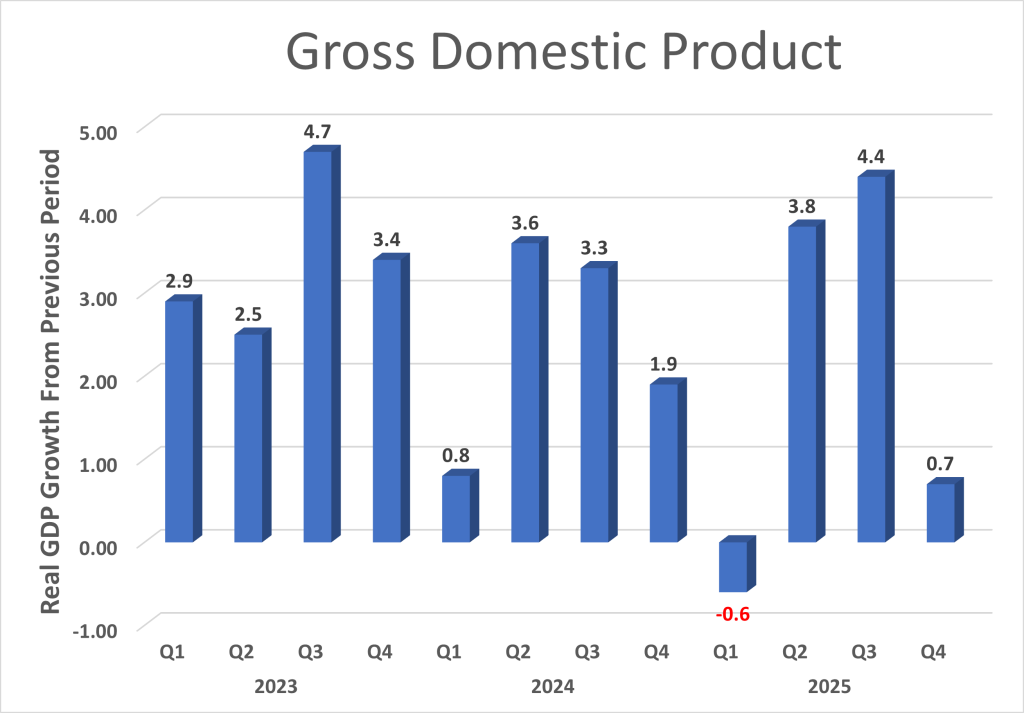

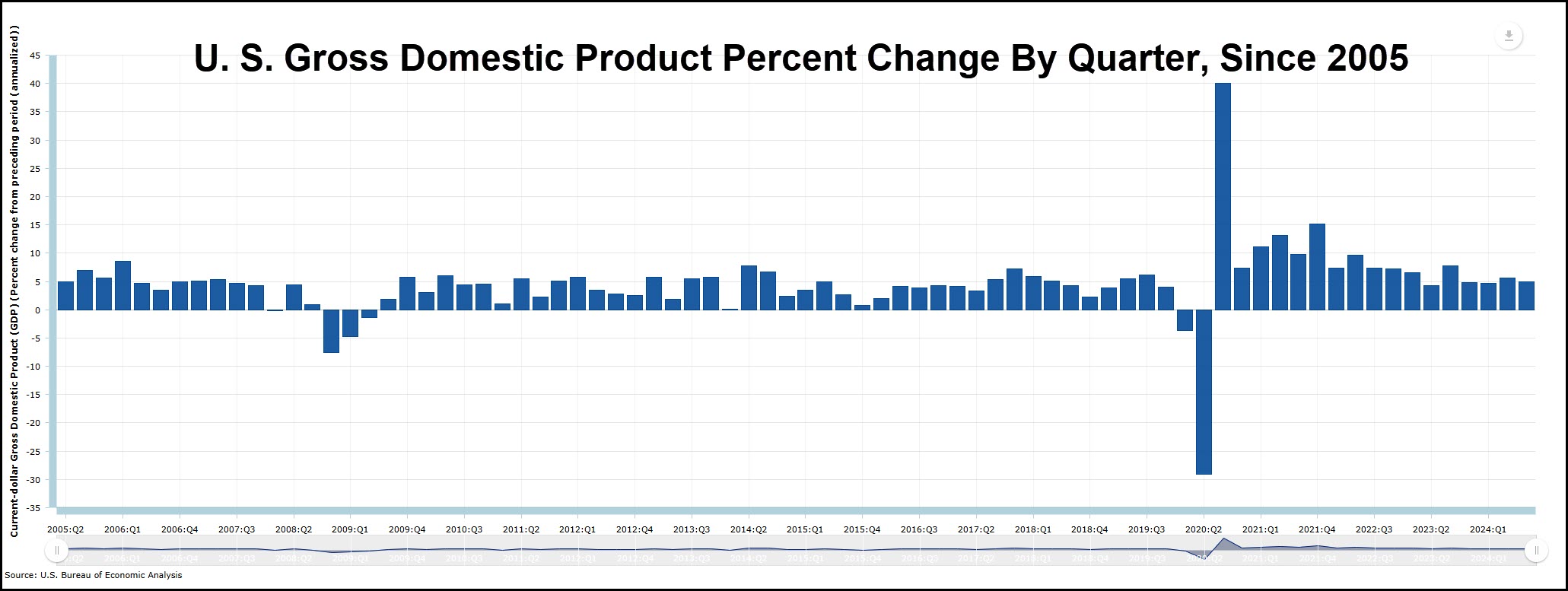

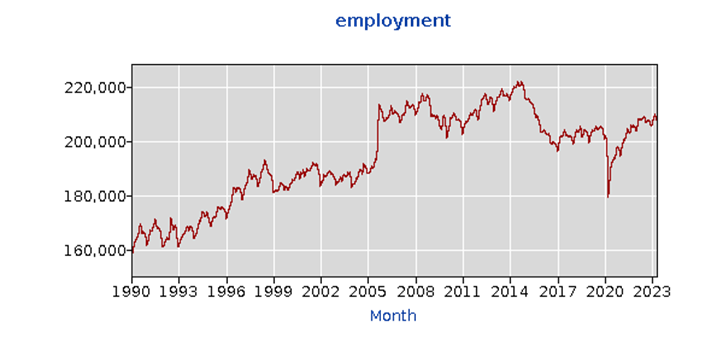

Just released: Growth of U.S. economy plummets. Yesterday’s release of .7% economic growth in the 4th quarter of 2025 was the 2nd worst quarterly growth in the last 3 years, as shown in the chart. This 4th quarter growth rate combined with the 1st quarter growth rate makes 2025 the only year in the last 13 years (except for Covid) that the U.S. experienced two quarters of economic growth this low.

This article examines how poor economic growth affects the commercial real estate industry and details not only how the retail, office, industrial and hotel industries are affected but what they need to do today to protect themselves in periods of poor economic growth. Then we drill down into how the economy’s growth rate is calculated and the surprising answer to who is responsible for the decline in 4th quarter growth. Let’s get started.

Retrenchment Is A Strategy

Business owners are always pushing for growth and spending every waking minute creating new ideas to provide a better product that increases sales. The thirst for growth is at the heart of our free market system, but this latest showing of a slower growing economy reminds us that business owners need to be smart about their long term plans. This latest growth rate number means retail, office, industrial and hotel businesses should plan for a decline so first let's cover strategies to survive in a slow economy.

Retail Retrenchment Strategy

Retailers need to reduce inventory and plan how to keep inventory low during the next 6 months. Reduce operating costs by reducing hours, staff, payroll and renegotiate vendor contracts. Rather than spend on marketing to get new customers, reinforce value to existing customers. Many retail consumers first shop online then visit a store, so update your online presence and match offerings with actual inventory. Be stingy about dropping prices and focus on technology to make the most of your customer data to create a better shopping experience.

Office Retrenchment Strategy

Businesses heavy with office space still have to pay the same office rent whether employees work part time from home or full time at the office. While office rent leases can be long term, 5 to 10 years, everything is negotiable. Office tenants can renegotiate a lease for a smaller square foot space while giving the landlord a longer term. Landlords love long term leases. Underutilized office space can be subleased to provide income. If your business has multiple locations, offices can be combined and the lease with the nearest expiration period can be terminated.

Industrial Retrenchment

The warehouse sector is the hardest hit during a slowdown. With imports and exports declining, the demand for warehouse space plummets. Warehouse tenants can use a slowdown to prospect for new suppliers and use technology to track inventory and provide just in time delivery to provide a higher level of service. Warehouse tenants can review their floor plan for ways to reduce costs and increase profit margin. While warehouse tenants are pinched, landlords have big problems such as tenant defaults and deferred maintenance.

Hotel Retrenchment

Hotel owners have more tools than most that allow them to stay alive in a slowdown so they can prosper in better times. Of course hotel owners can cut back on staff, but even better, they can cross-train employees to work more efficiently. Instead of cutting rates, hotel owners can bundle services such as internet, dining, spa and parking. One industry standard is to charge a hefty amenity fee. Attracting loyal guests to book directly and utilizing email marketing tied to a creative website can drive sales.

What Is GDP?

GDP is the Gross Domestic Product, which is the value of all goods and services produced only in the United States. GDP data is collected and produced by the U.S. Bureau of Economic Analysis which is under the Department of Commerce that was established in 1913.

What Caused GDP To Decline: Government Spending Freefall

GDP is a formula that is calculated by combining 5 sectors, including: spending by U.S. residents, business spending on equipment and inventory, government spending (federal, state and local) plus exports. Imports are subtracted from GDP. Here is the formula:

GDP 5 Sectors Move Independently

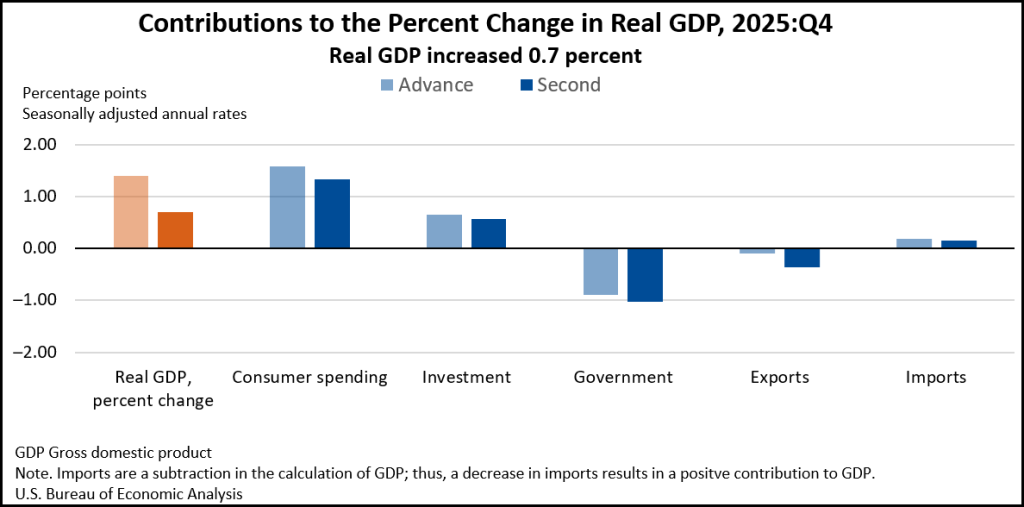

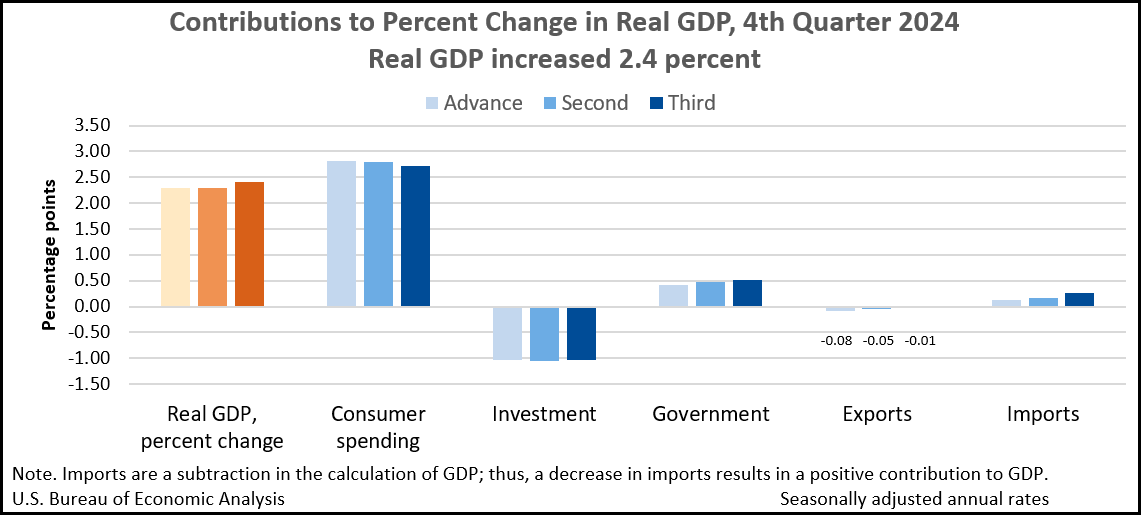

Not all of the 5 sectors of GDP rise or fall at the same time. In the 4th quarter of 2025, consumer spending increased 2% and investment increased 3.3%, but exports declined 3.3% and imports declined 2.5%.

The biggest drag on the economy was government spending which declined 5.8%, as shown in the chart. But the government sector includes federal, state and local spending and the entire decline in the government sector was due to a 16.7% decline in federal spending which offset the 1.2% increase in state and local government spending. If only the future provided a good war to bring back federal defense spending to boost the economy.

GDP Is Measured Three Times

The GDP percent number you read about in the news this week is the rate of change from the previous quarter and is measured 3 times, as shown in the table. Make sure you know which estimate is the latest:

the advance estimate, coming about a month after the quarter's end, is an early look based on the best information available at that time,

the second estimate and

third estimate each incorporate additional data that weren't available the month before, improving accuracy.

Also, GDP can be reported two ways: one called Real GDP which is after inflation is factored out and, two, Current Dollar GDP which is the actual dollar amount.

Summary

The one concept I remember from MBA school was that retrenchment is not an acceptance of failure, but is a viable strategy in a slow growth economy. This latest growth rate number means retail, office, industrial and hotel businesses should plan for a decline and utilize these strategies to protect themselves in a slow economy so they can thrive when the economy grows again.

For more information on Commercial Real Estate, select from over 150 articles in the Louisiana Commercial Real Estate Blog. Louisiana Commercial Realty is managed by commercial broker Robert Hand in New Orleans, who has successfully represented tenants and landlords in hotel, retail, warehouse and office transactions. Robert is the only broker in the state to create and teach a workshop showing residential agents how to be successful in the commercial sector which was approved for continuing education credits by both the Louisiana and Mississippi Real Estate Commission. Robert also has authored more commercial real estate articles in national publications that any broker in the state. During the Covid years, Robert worked for the Small Business Administration teaching new businesses how to get started and grow successfully.

It was standing-room-only for another continuing education course on “How To Do More Commercial Business”, taught last week by Louisiana Commercial Realty broker Robert Hand to group of investors and residential agents at Realty One Immobilia in Metairie.

The class detailed vital information that real estate agents and investors need to know about commercial real estate, and was designed to help agents who work mostly in residential but dabble in commercial real estate to better serve the needs of their commercial property clients.

Commercial Class Presents Pricing, Zoning & Artificial Intelligence

The class drilled down into the nitty gritty of the six sectors of commercial property: office, warehouse, retail, shopping centers, hotels and apartments, and presented an analysis of pricing for each sector. Also covered was information on zoning, contract language to avoid, and how the latest artificial intelligence data can be utilized to help retailers find the perfect location. The class also taught agents how to value commercial property based on income, which is one method utilized in all commercial appraisals.

Nobody Teaches About Commercial Real Estate

The 2 hour class was presented by Louisiana Commercial Realty broker Robert Hand who explains, “When I started 20 years ago working as a commercial agent for Latter & Blum and then RE/MAX Commercial, I was surprised that neither firm trained agents in how to work in the commercial property sector, despite the fact that these were the two largest commercial real estate companies in the area. So I created a course teaching agents who mostly make a living in residential property but dabble in commercial property how to do business in the commercial arena. The course was approved last year by the Louisiana Real Estate Commission for 2 hours of continuing education credit for agents.”

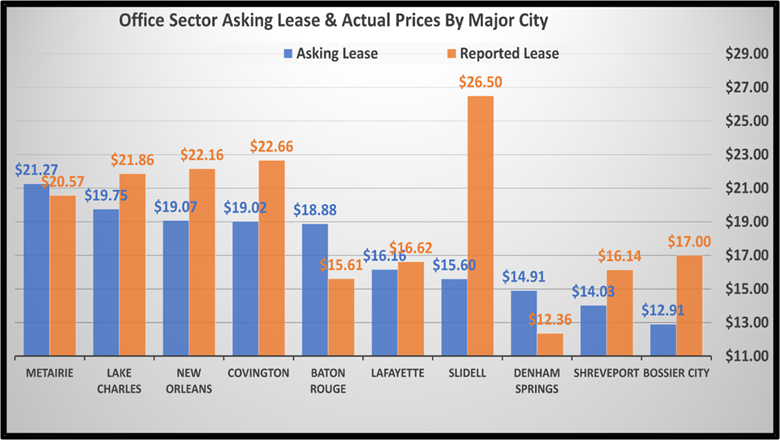

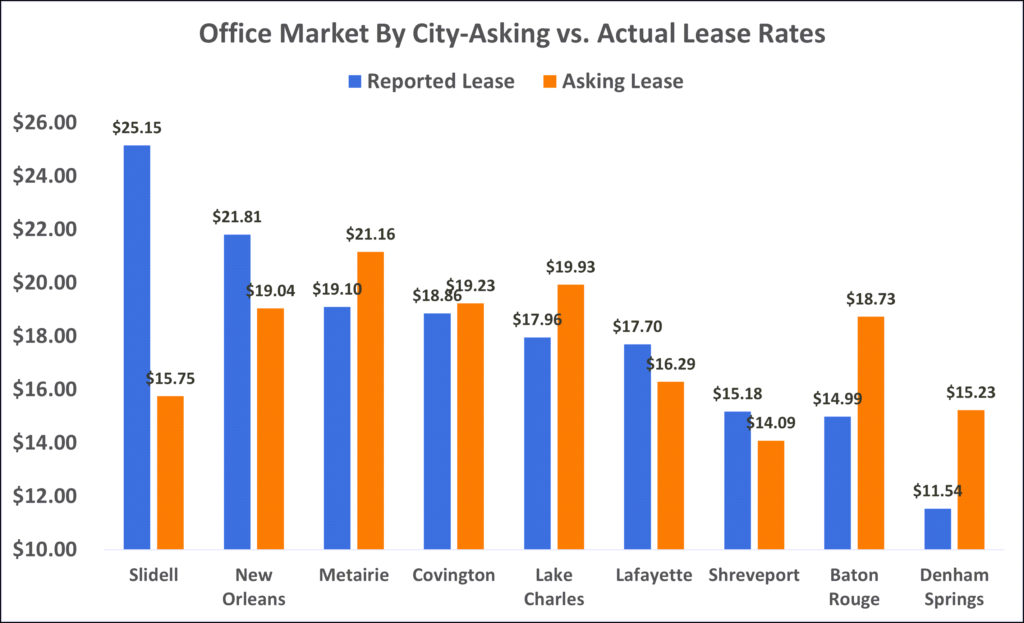

Office Sector Prices By Major City

The in-person class includes research on over 7,000 office space listings throughout Louisiana and concluded only 194 were closed on average each month, which is only 3%. Metairie closed 21 of the 194 leases which were the highest office prices at $21.27 per square foot. Among the major cities in Louisiana, some reported leases at much higher prices than average, such as Slidell, but that was because only one lease was transacted. Baton Rouge closed the highest number of office leases.

Industrial/Warehouse Prices By Major City

The class also presented information on lease prices of warehouse space in Louisiana’s major cities. Of the 101 warehouse leases listed, Lafayette closed 7 leases at an average price of $8.10 per square foot which was a 20% discount to the $10.03 per square foot list price. New Orleans and Lake Charles only closed 3 warehouse leases, but the lease price for each was above average.

Training In Commercial Real Estate Offered In Mississippi

The continuing education course was adapted to include commercial real estate in Mississippi, and recently was approved by the Mississippi Real Estate Commission for continuing education credit. Broker Hand says, “All the other continuing education courses offered are written either by title companies or vendors who never actually worked in commercial estate. The course I created is the only class in Louisiana or Mississippi that was written by a commercial agent who is actually in the field with 'hands on' experience in how commercial real estate gets done.”

Louisiana Commercial Realty announces the sale of their 12,000 warehouse listing near downtown New Orleans for $777,000, after marketing the property for 2 years and bringing the seller 5 offers. The property offers a loading dock, rear rollup door, front rollup door and loading dock with crane, plus a billboard that is leased for $18,000 annually, and was home to Cajun Spirits Distillery, the only New Orleans distillery producing vodka.

Listing broker Robert Hand explains, “The warehouse has a terrific location near downtown New Orleans, and is one of only 4 warehouses in the area. Like many warehouses, the property was constructed almost 75 years ago but was appraised for $1,100,000. We heavily marketed the property, with advertising in the top commercial databases: LoopNet, LACDB and CREXI, along with targeting businesses directly that serviced the hotels and restaurants in downtown New Orleans and would need warehouse space. The feedback we received was that warehouses in Elmwood were not as attractive because the area had become congested and it was time-consuming to get trucks in and out quickly; therefore, we marketed the property to those prospects who were looking for a better location."

Hand says they received more interest in this property than any other listing and their marketing efforts secured 5 offers from $750,000 to over $1,000,000, with some cash offers and one with 15 days to close and another requiring no interest owner financing.

Hand explained, "Every transaction has problems so the most valuable service we offer clients is our expertise at negotiating to overcome obstacles. We have been trained in negotiating by the NASD. We negotiated one offer that included a $50,000 non-refundable deposit but the buyer showed up at closing saying he expected a wire any minute now with the money. It never came. The $50,000 deposit was kept by the seller but that was little consolation. The highest offer was $800,000 from a nearby business who needed that location and we negotiated the sale by excluding the billboard, which produced $18,000 annual income so we estimated that billboard value at $160,000. During inspections, some issues came up and we negotiated a reduction in price to $777,000 if the deposit would be immediately non-refundable. Another issue came up because the distillery still had large tanks in the property that needed to be removed by closing. We negotiated another agreement with which both buyer and seller were happy. Those results confirm that our sophisticated marketing strategy works and our expertise in negotiating for our client gets the job done."

While the property was on the market for 2 years but the average New Orleans industrial property takes 12 months to sell, Hand says the sale price was the highest price for a New Orleans warehouse sale so far in 2025 according to the Moody's LACDB database.

For more information on commercial real estate, read our recent articles:

This week Louisiana Commercial Realty broker Robert Hand, presented his 'Commercial Real Estate Strategies' workshop to a sold out audience of real estate agents. The workshop is a two hour deep dive into the major aspects of commercial real estate that buyers, sellers and real estate agents need to know.

The workshop was created by commercial broker Robert Hand, who explains:

"As a 20 year veteran in the commercial real estate industry and completing hundreds of transactions, I felt there was a real need for someone to teach others what they really need to know about commercial real estate, because it is so different from anything else. You not only need to know about demographic trends, zoning issues and construction, but, to be successful, you also need to know about pricing which does require a little math and you need a ton of negotiation skills. Nobody teaches this stuff. Until now.

My knowledge comes from working with the largest commercial real estate companies in the state, including Latter and Blum (now Compass), and also RE/MAX, but nobody there taught anyone about the skills or knowledge required to complete enough transactions so you could make a living. So I created a course which does just that. The Louisiana Real Estate Commission approved it for continuing education hours, and recently I taught the course to a sold-out audience of real estate agents, representing all the major companies, including Compass, Reve, Snap Realty, EXP Realty, HomeSmart and Berkshire Hathaway."

The workshop explains the major issues involved in commercial real estate, including:

How to stay out of trouble in contracts

Knowing your zoning requirements

How to price office, retail and warehouse properties using financial statements

How to use consumer spending patterns to pick the perfect retail location

How to negotiate using active listening to get what you want

Gross, Modified and NNN leases

Who pays tenant improvements

Common Area Maintenance

How to use Cap Rates to accurately value property

For more information on the next workshop, email Louisiana Commercial Realty at robert@louisianacommercialrealty.com, and get more details at: Commercial Real Estate Strategies

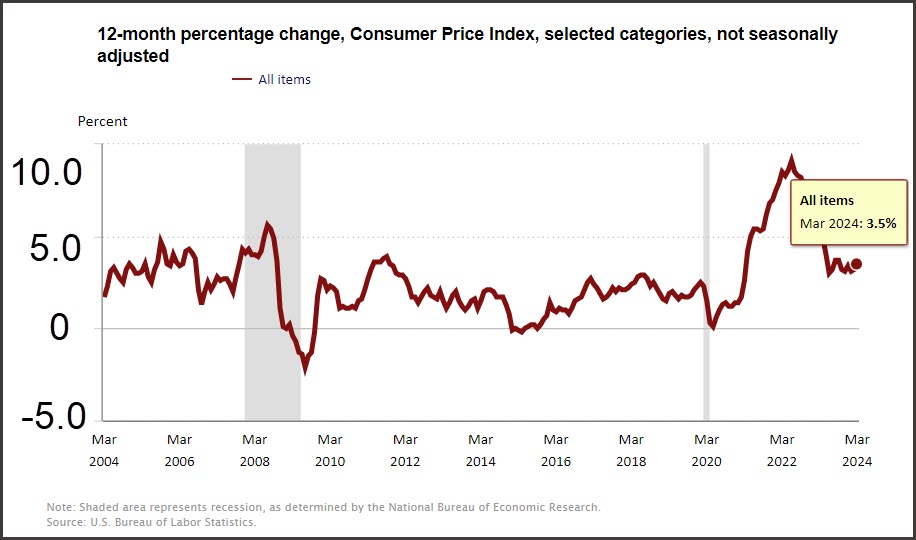

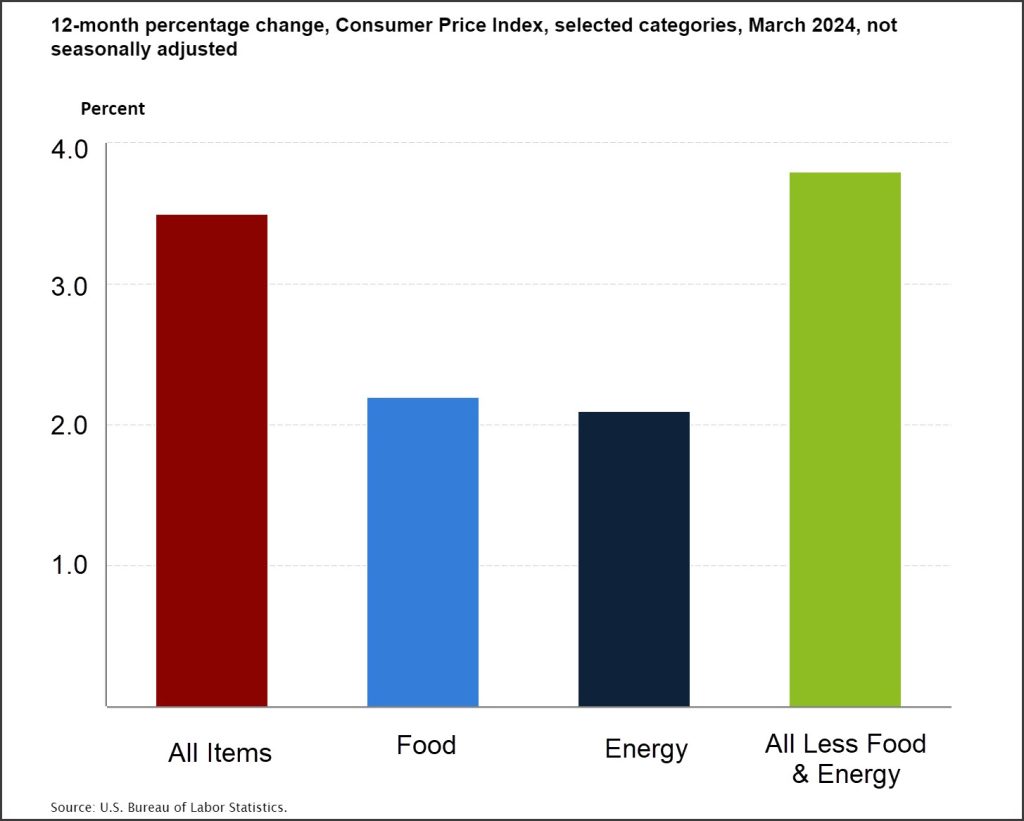

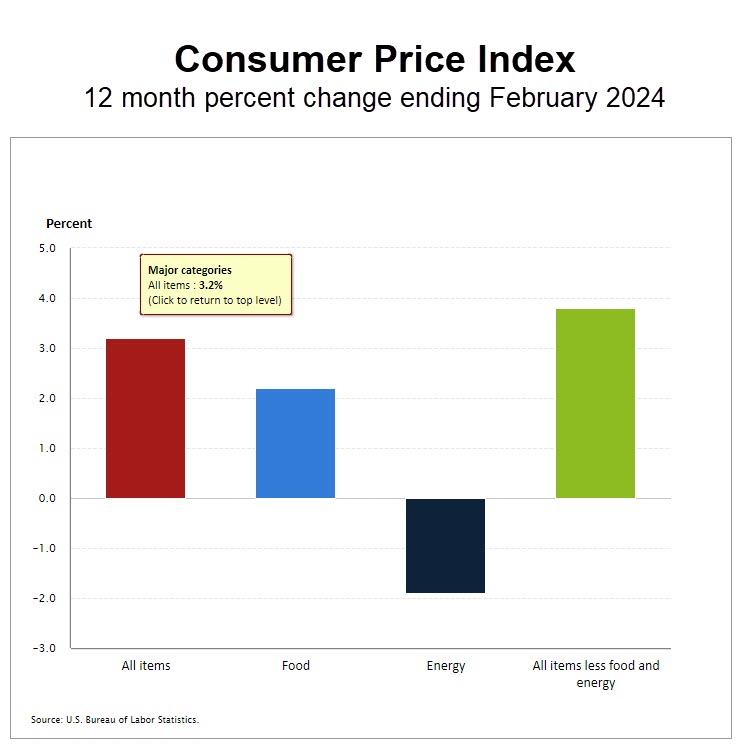

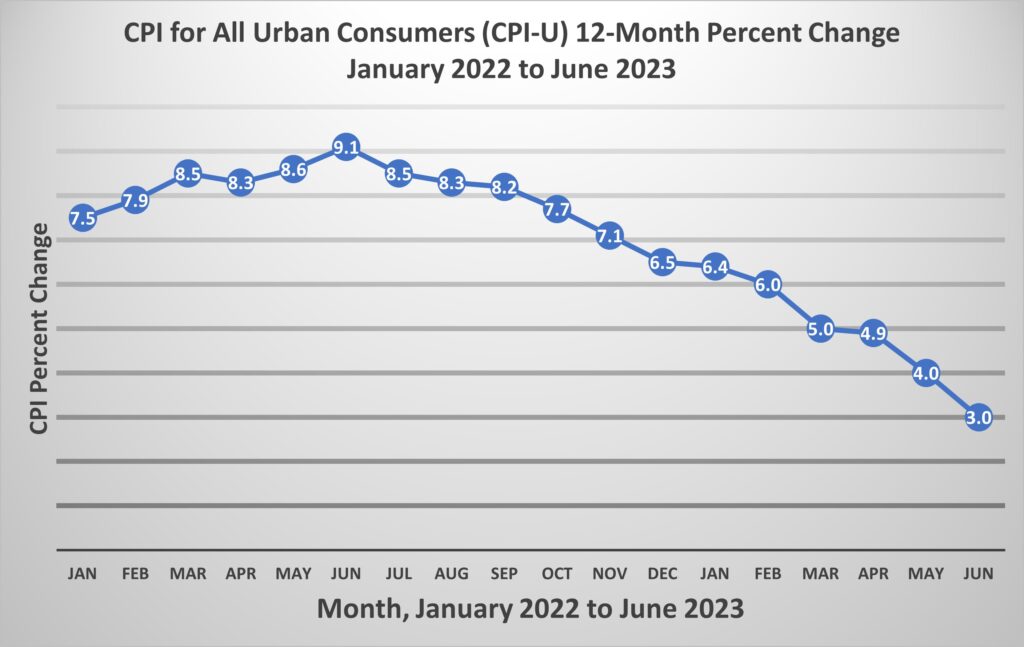

Inflation is dead, long live inflation. The latest release of inflation numbers shows that inflation for the year ending March 2025 for the basic items actually declined 0.1%, a sharp contrast to only 2 months ago when inflation was the top story and everyone was worried about skyrocketing egg prices. This article explores the changes in inflation, which are an important part of any commercial lease, and how that affects landlords and tenants who lease commercial space. Let's get started.

Where Is Inflation Today and What Is The Trend?

The start of 2025 saw inflation for January skyrocket up 0.5%, but then drop in February 0.2% and go negative in March with prices actually declining 0.1%. There is no defined trend yet, so let's examine what history tells us.

What Can We Expect Normal Inflation To Be?

Since 1914, when we first started keeping records, inflation has averaged 3.3%, and since 2010 averaged 2.6%, but since 2020 averaged 4.2%, due to one 8% year during COVID. The conclusion from the data is that inflation should be expected to be around 3% per year, and we should recognize that the last 5 years has not been normal.

Lease Language No Longer Protects Landlords

Inflation is measured by the Consumer Price Index and, if you are a landlord or a tenant, your lease defines how much more rent is paid every year based on that number. Just 3 years ago, inflation was 8% and landlords reaped the benefit of much higher rents in 2023. But 2022 was the year we experienced extraordinary economic imbalance due to Covid, suffering supply chain shortages exacerbated by consumers spending wildly, resulting in the classic free market supply/demand curve with prices increasing. But in 2025, things have changed.

Inflation and Your Lease

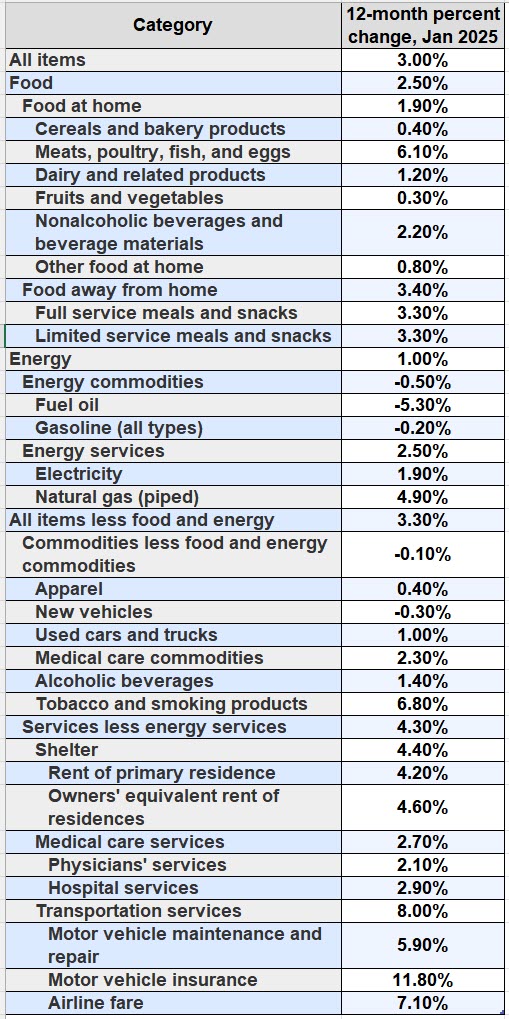

If you are a landlord or a tenant, your lease should include language that states rent will increase with inflation. If you have a really good lease, it will be clear about how inflation is calculated and what inflation index is used. The problem is that inflation is measured 8 different ways and includes prices of thousands of items. While the inflation number for the 12 months ending March 2025 was only 2.4%, many of the costs that landlords pay have increased much more than that, such as electricity, property taxes and hazard insurance.

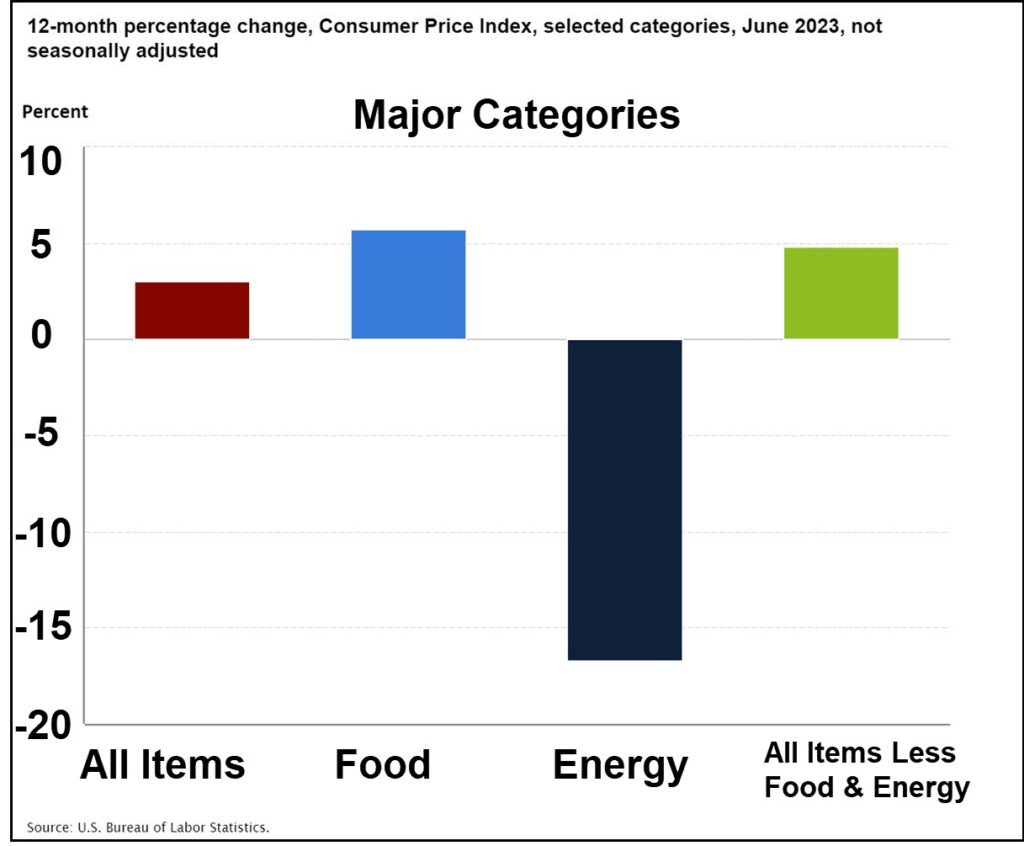

For example, if you are a landlord in New Orleans, congratulations because the 14% increase in property taxes was the largest increase of any city in the United States, and that is on top of a 37% increase last year in New Orleans/Metairie insurance costs for office properties. The table below shows all the major components of the Consumer Price Index, Food, Energy, and the third category: All items, less Food and Energy, but the data show about many categories increased prices much more than the average. The result is that a lease doesn't always protect a landlord or tenant from rising costs just because rents are adjusted for the sum of all these categories.

How Landlords Protect Themselves From Inflation

Most landlords require language in their leases which allow for rents to increase based on inflation, but also allow rent to increase at a minimum rate. A good lease will have specific language that explains how the inflation number is derived, such as:

" At the end of the initial term, there shall be an annual reevaluation and increase of the basic rent based on the Cost of Living Index as published by the U.S. Department of Labor, Consumer, Price Index for Urban Wage Earners and Clerical Workers, U.S. City Average. However, under no circumstance is the base monthly rent to increase not less than three percent annually."

Another way landlords protect themself is to reduce the base rent but pass along the property taxes and insurance to the tenant in a triple net lease. This means the tenant would need to agree to incur the risk of the higher than normal increases. Many times, however, this would make the property unattractive to a tenant and price the space out of the market.

How Tenants Protect Themselves From Inflation

Tenants protect themselves by negotiating language in their lease which puts a cap on operating expenses that can be passed along from the landlord. Sometime the language states that there is a cap on controllable expenses, such as landscaping, but the lease may state there is no cap on uncontrollable expenses, such as property taxes and insurance. So that doesn't really help a tenant.

In summary, all lease language can be negotiated and a tenant has the most power to force changes in the lease language during the dating period, not after the marriage. The bottom line for tenants is to make sure you have a trained negotiator on your team.

For more information on how inflation is measured, read our blogs:

African Americans in the New Orleans/Metairie area in 2023 were denied as much as 55% more home loans when compared to White applicants in the same income bracket, according to research by commercial broker Louisiana Commercial Realty. Data from the Consumer Financial Protection Bureau show that 22,701 loans for New Orleans home mortgages were made in 2023 totaling $3 billion, but African Americans were denied loans totaling $319 million, or approximately 32% of applications, compared to a denial rate of 18% for White applicants.

Reasons For Loan Denial

There are many reasons for loan denial. For home purchase applications, lenders cite low collateral as the most common denial reason. For refinance applications, lenders cite the debt-to-income ratio, insufficient cash, unverifiable information, and incomplete applications as the most common denial reasons.

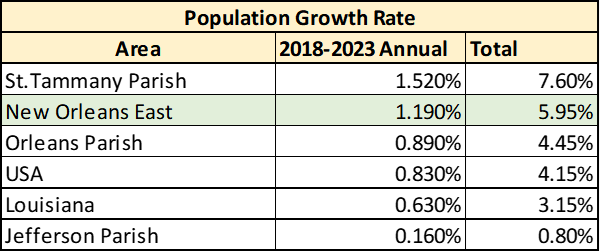

However, these common reasons would not fully explain why the denial rate was higher across the board for any income bracket, even those with family income above the median average. Louisiana Commercial Realty researched the data as part of their efforts to revitalize New Orleans East, and commercial broker Robert Hand explains:

"My firm has focused on bringing business to New Orleans East for the last 15 years, so we were curious as to why people were constantly unable to obtain financing to start new businesses even though entrepreneurs had great ideas and the businesses were feasible. When we examined the mortgage numbers, we found that at every level of income, African Americans were denied a much higher percent of loans than Whites in New Orleans and Metairie, and also denied loans at a much higher rate than the national average. We started this analysis in 2018 and found the same discrimination then: rates of denial for African Americans were twice the denial rate for Whites, in all income brackets."

The analysis examined 5 income brackets relative to the median income in the New Orleans and Metairie area:

Income under 50% of the average.

Income 50% to 79% of the average.

Income 80% to 99% of the average.

Income 100% to 119% of the average.

Income over 120% of the average.

Results from 2023 show, even in the income bracket exceeding 100% of the New Orleans MSA average, that denial rates were 25% for African Americans, but only 15% for Whites. That excess denial totals totals $75 million and since the average loan application was $201,000, that would have denied an additional 375 home purchases.

Discrimination Is Nationwide

The data show that nationwide, loans for conventional mortgages were denied at twice the rate for African Americans as were for Whites. The analysis also revealed that the denial rate in New Orleans/Metairie for African Americans is almost twice the national rate.

Where Mortgage Information Comes From

The mortgage data is available from the Consumer Finance Protection Bureau, which was established in 2010 under the Dodd-Frank Act and is an independent bureau within the Federal Reserve System, with a $500 million budget financed by up to 12% of Federal Reserve revenues.

The Bureau collects the data with the power enabled by the Home Mortgage Disclosure Act, enacted by Congress in 1975 and implemented by Regulation C which requires financial institutions to maintain, report, and publicly disclose loan-level information about mortgages. These data help show whether lenders are serving the housing needs of their communities and designed to shed light on lending patterns that could be discriminatory.

For more information on the New Orleans commercial real estate market, read our other articles:

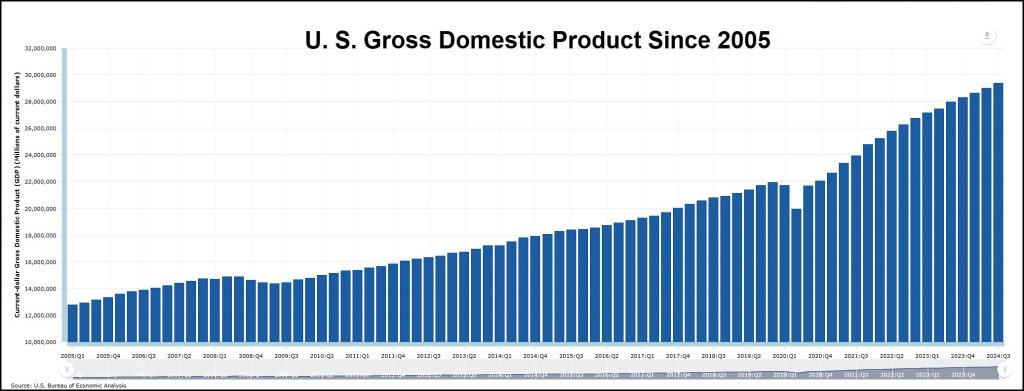

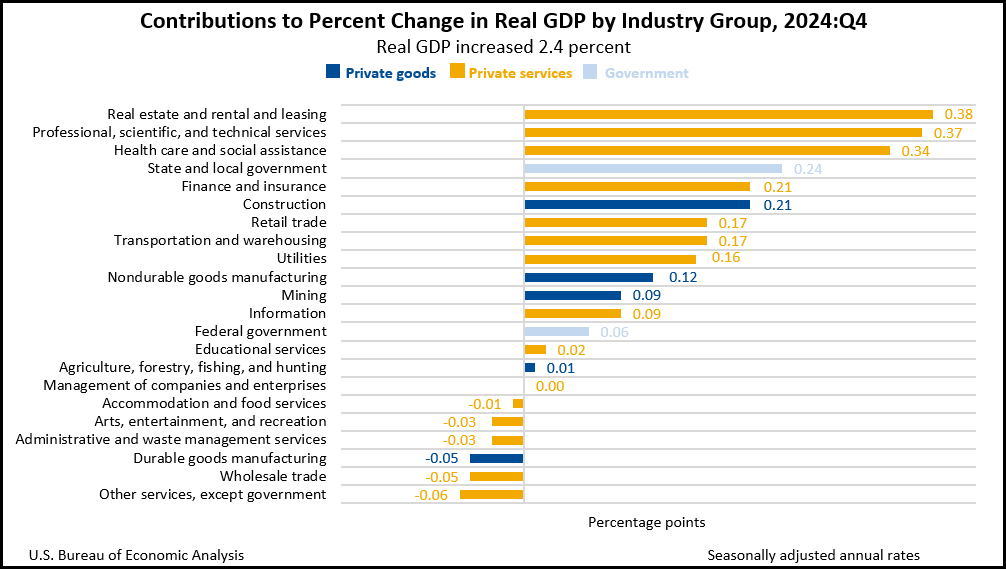

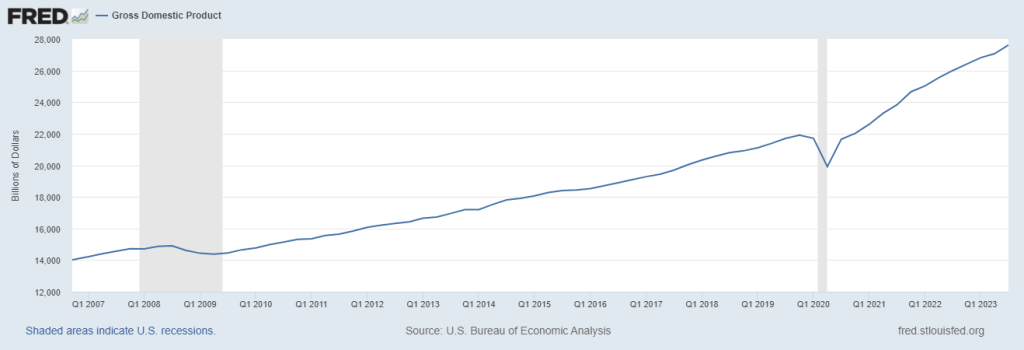

Today, real growth in the U.S. economy was announced to be 2.4%, after inflation. This was a drop from the previous quarter growth of 3.1%. The economy still has momentum, just not as much. If you own a business, this growth rate of 2.4% doesn't seem like much, so how can you grow your business more than the economy? Let's drill down into GDP and expose where faster growth comes from.

Gross Domestic Product Components

The Gross Domestic Product is calculated by the Bureau of Economic Analysis, and is the total dollar amount of goods and services produced, but the final GDP number is the sum of 5 components: consumer spending, investment, government and exports. Imports are subtracted from GDP because they are included in the consumer spending component.

What Businesses Are Boosting The Economy Now?

The economy is recovering from the 2020 Covid drop, as shown in the chart of GDP from 2005, but not all industries are contributing. If you own a business and are looking to grow your business more than the 2.4% economy, all you need to do is steer your business to benefit from industries that are leading in growth:

Real Estate Leasing

STEM

Health Care

and, as shown in the chart, stay away from businesses that are declining:

Wholesale

Durable Goods Manufacturing

Hotel & Restaurants

Recreation

Waste Management

Summary

In summary, the GDP is announced but revised 3 times. It is also calculated two ways, one, as real GDP, which subtracts the inflation rate, and, two, as nominal GDP which is the total number. GDP is calculated every quarter, but the number is an annual rate so be aware of what calculation method you are looking at.

The bottom line is that your business should at least be growing by the GDP number, but grow your business faster by finding a way to do business with those industries leading the charge.

Want more information on the economy, commercial real estate prices or interest rates? Read our articles:

Start-ups and businesses in their infancy always prefer leases for just a few years in case their business fails; however, established businesses always prefer longer lease terms which gives them control of their space, especially businesses that have spent money building out their space, such as breweries. Most leases have a section called "In Solido" which means the tenant is personally responsible for the entire lease payments even though the lease is in the name of an LLC. That means the term of your obligation is a financial burden.

Recently Louisiana Commercial Realty helped Urban South Brewery renew their $1,000,000 lease for another 5 years in one of the more complicated real estate negotiations in their 20 year history. Broker Robert Hand explains, “We have a long history with this warehouse, having been hired by the warehouse owner in 2015. The property is zoned MU-2, so we originally marketed the warehouse to those businesses requiring that zoning, which included breweries. Within 30 days, we secured a 10 year lease with Urban South Brewery for our landlord client”.

Complicated Lease Terms

But that is only half the story. The original lease was only for the 20,000 square foot front half of the building and when the rear half of the building became available the following year, Hand negotiated a 10 year lease for that space also. Therein lies the challenge. Each space, front and rear, had a separate lease that included an annual adjustment for the Consumer Price Index, causing the owner to calculate the inflation adjustment based on different periods, effective dates and square footages.

Like many properties in New Orleans that are inherited, owners self-manage their commercial property and forgo the expense of paying 3% to 6% of rent income to a property management company who does all the everyday little things that come up in renting commercial space. The result is that owners rarely have the expertise to negotiate commercial leases smoothly and without expensive conflict in later years.

Correcting The Attorney's Lease Language

Just before the initial lease term expired, the tenant expressed interest in exercising an option to renew the lease, and Hand had an idea, "Why not combine both spaces and have one lease start date and one annual inflation adjustment date? Easy, right? Except that one of the spaces had a renewal provision triggering an 8% rate increase upon renewal and the other did not.” Complicating the negotiations was that one of the parties wanted an attorney to draft a complicated agreement to renew the lease. “We spent lots of time explaining the lease language to both sides, to make sure each party understood the language and that the lease renewal language was what they intended”, Hand explained, “and we corrected much of the attorney’s wording so it made sense and was easier for landlord and tenant to understand-with the attorney’s final approval, of course.”

Successful Negotiation Skills

Commercial real estate involves knowledge of property values, zoning, population demographics and marketing but also negotiations. Hand says, “This is a clear example of why owners need help with commercial property. I have been trained in negotiation by the NASD, and have the CCIM and SIOR designations, an MBA, and spent years writing appraisals. We are well qualified to handle any aspect of commercial property. This is another example of where we helped the landlord simplify their property management and also helped the tenant get a lease renewal with favorable terms. This deal would never have been successful had we not been involved-there were simply too many moving parts. We just took one issue at a time and zeroed in on a solution. In life, there are those that make excuses and those that get things done. We get it done.”

For more insights into what your lease should include, read our blog:

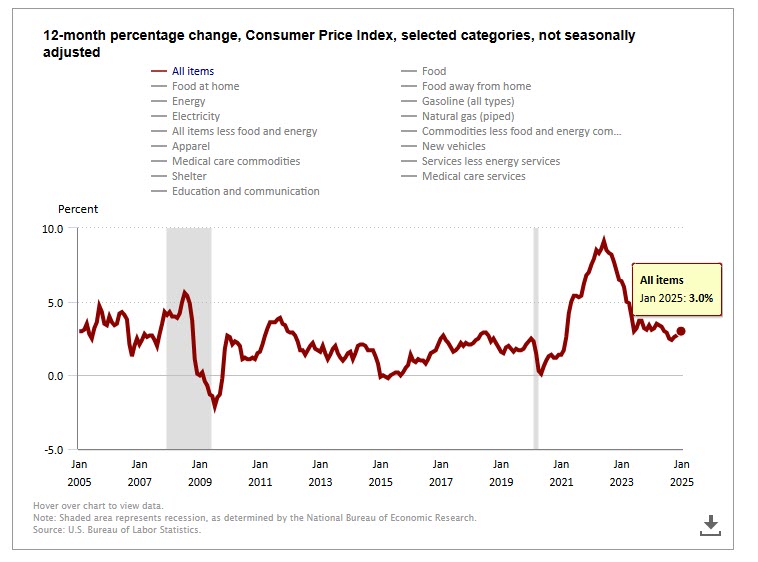

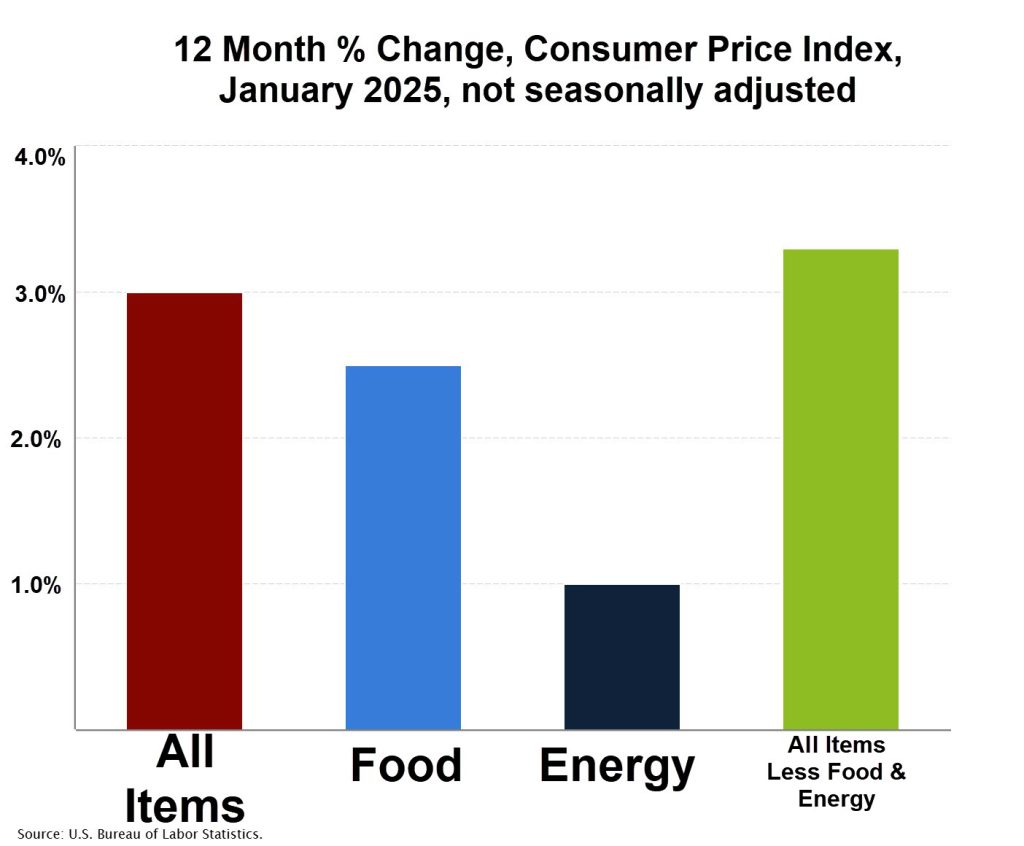

Last week, inflation was calculated at 3% for the last 12 months and while the high cost of eggs was the main concern, those expensive eggs are only the ones that roosters lay, right? This article lays out the facts about inflation and explains what you need to know. Let's get started.

Bird's Eye View Explanation

Inflation is called the Consumer Price Index and is measured by the Bureau of Labor who collects over 8,000 data points from 75 cities, including 6,000 homes and 22,000 retailers, for prices people pay for goods and services purchased for everyday living. Inflation is not just one number that applies to everything, some items increase in price while others decrease because each item has its own supply and demand curve.

There are two major populations measured for the Consumer Price Index:

the All Urban Consumer Group which represent 90% of the total population.

the Urban Wage Earners which includes clerical workers but only covers 30% of the population.

Not included in the CPI are people in rural areas, farms, military, prisons and mental hospitals.

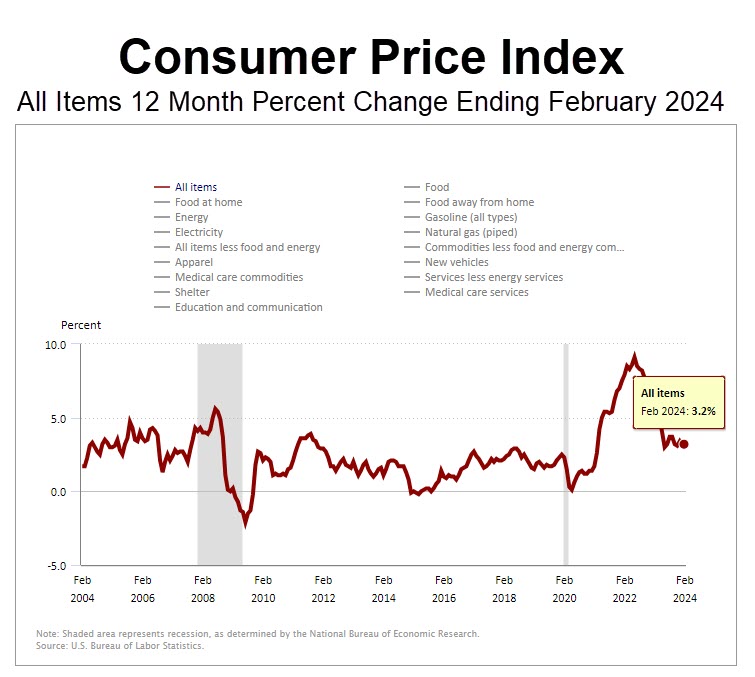

Inflation Trend The Last 20 Years

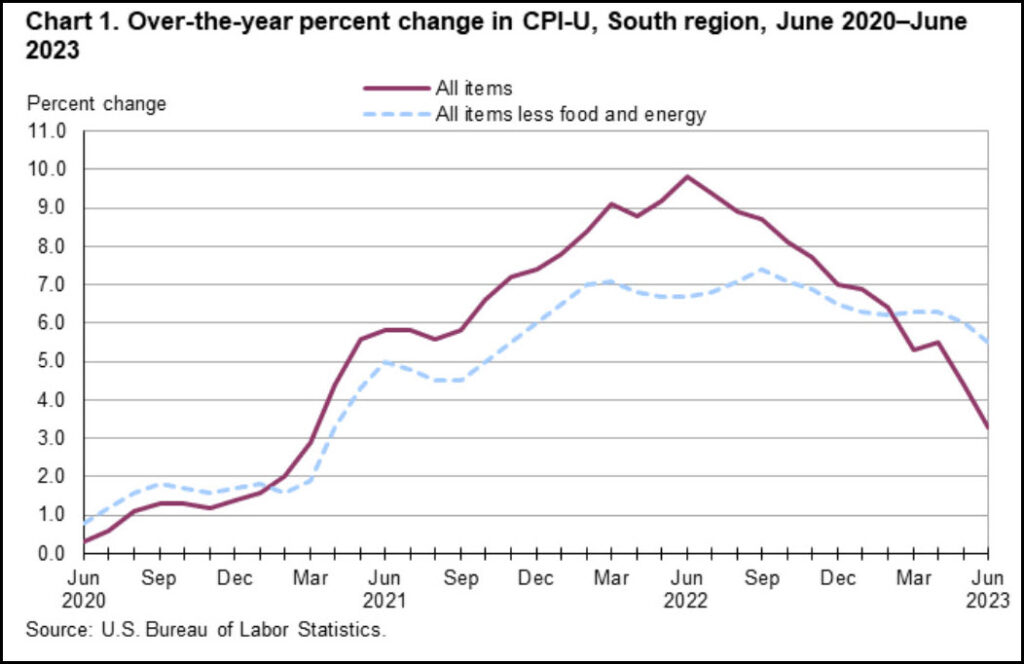

The last 20 years witnessed 2 recessions where inflation declined, as shown in the shaded areas in the chart. The mortgage crisis in 2008 caused a sharp drop in the economy and therefore inflation, and 2020 saw the onset of COVID rapidly shut down the economy, causing unemployment to rise to 14%; however, by 2022, supply chain shortages caused prices to skyrocket, only to fall back to normal in 2023.

What Happened The Last 12 Months?

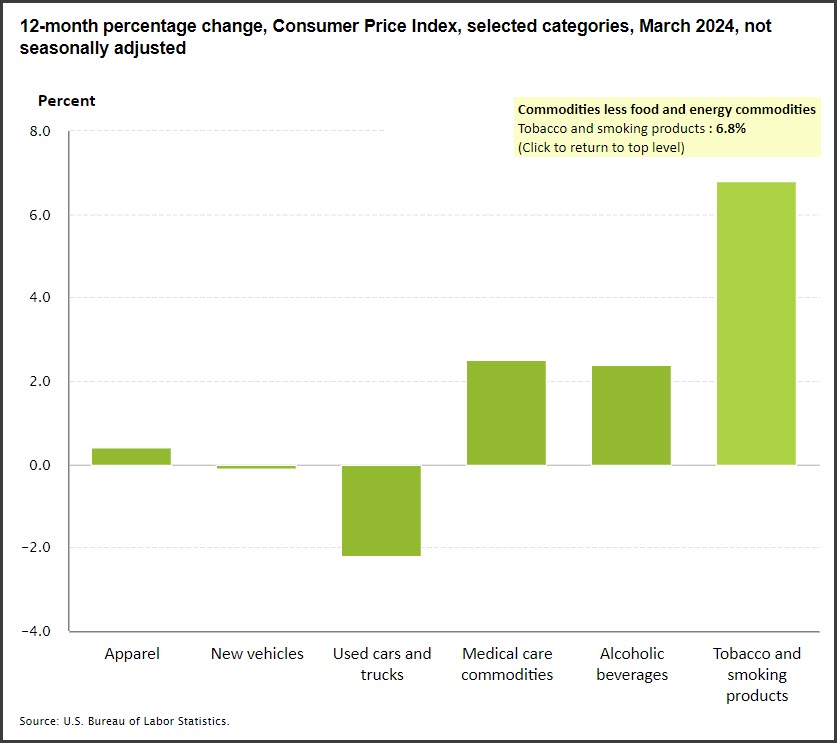

The Consumer Price Index is comprised of major categories including "Food" and "Energy", but like any government agency there is a 3rd category called "All Items Less Food & Energy" which includes clothing, vehicles, booze, medical care, rent, cars, airlines and smoking.

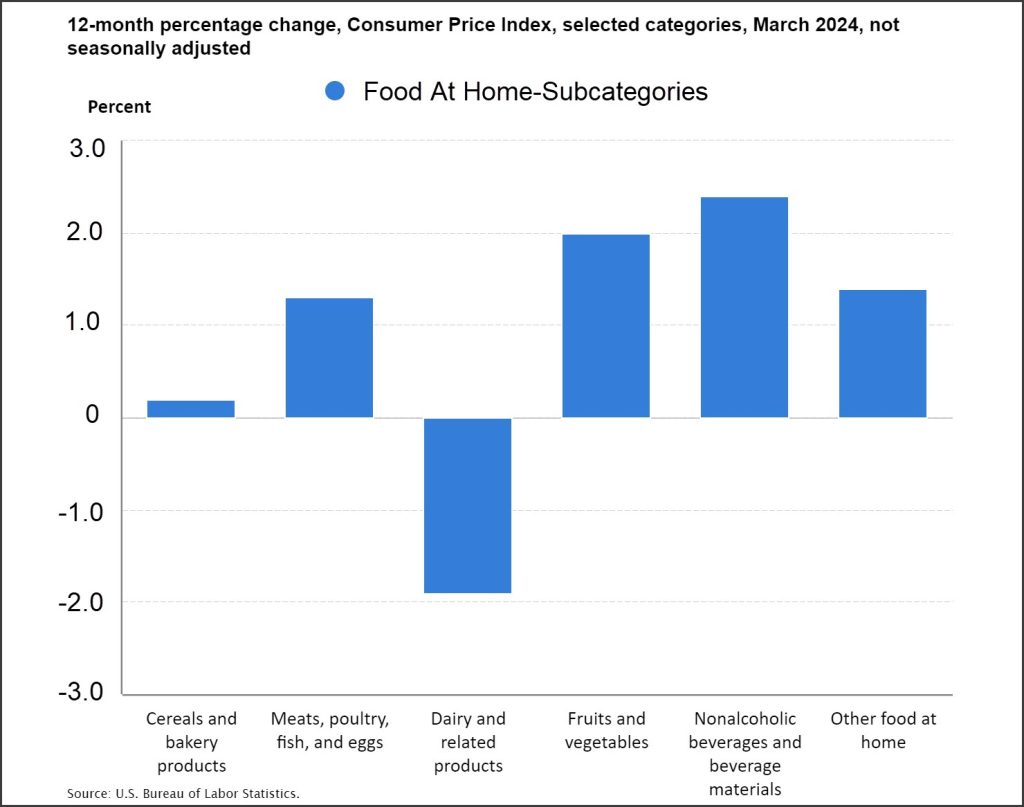

The last 12 months saw inflation increase 3%, but the food component only increased 2.5%, and that number is an average of two categories. Food can be further divided into "Food At Home" which increased 1.9%, including a 15% price increase for eggs, and "Food Away From Home" which increased 3.4%.

Energy Prices Drop

Energy prices increased 1% over the last year, but that category is comprised of gasoline which dropped .2% and fuel oil which dropped 5.3% over the last year. Electricity prices increased 1.9% and natural gas prices increased 4.9%.

Everything Else Category

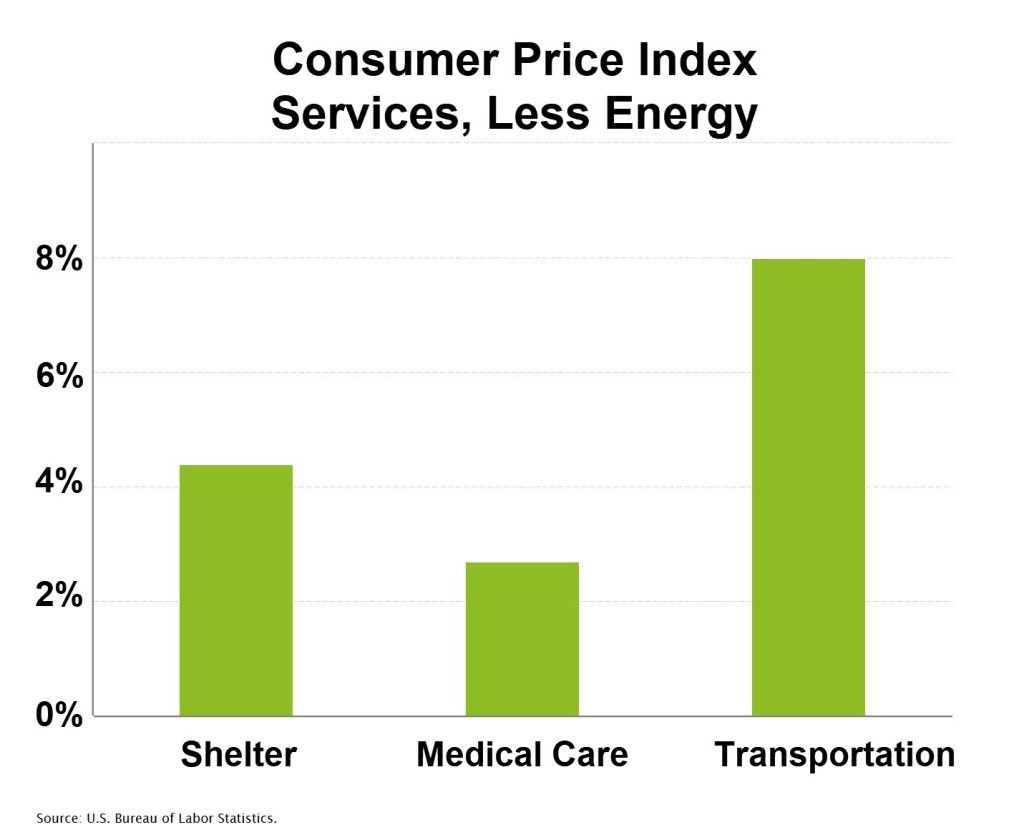

The remaining major category for the Consumer Price Index is called "All Items-Less Food & Energy" and increased 3.3% over the last 12 months. That category includes "Shelter" which increased 4.4%, which was the smallest increase in 3 years, and "Medical Care" which increased 1.6%, but the dagger in the heart was an 8% increase in "Transportation" including an 11.8% increase in auto insurance and 7.1% increase in airline prices.

Summary

The Consumer Price Index has 8 different calculation methods, including chained, unchained, seasonally adjusted and not seasonally adjusted, plus monthly calculations that some would incorrectly annualize. But the main idea to take home from this article is that inflation is not just one number, but is a bird's eye view of prices and when you drill down into the sectors, you can see lots of hens running around laying lots of eggs, each one doing something special.

Want more information on inflation and how the Consumer Price Index affects your lease? Catch our articles:

It is no surprise that the Chiefs will win the Superbowl by 7 points tomorrow, but the latest data on the New Orleans office market will shock you. We analyzed all the current listed office space for lease in New Orleans, looking for insight to future trends by examining 2,878,471 square feet for lease in 493 listings in 95 different properties. We discovered that only 9% of the listings account for 36% of the square footage for lease. We also examined what type of operating expenses are commonly passed through to tenants, and are able to conclude some surprising trends on the New Orleans office market for lease. Let's get started.

New Orleans Office Market History

International Trade Mart Office Building-Now a Four Seasons

We have been researching and writing about the commercial office market in New Orleans and Louisiana for 10 years now, and there is an interesting history to it. The New Orleans office market is different from the Metairie market and most other large population cities in the South. Most of the downtown office space is located in high rise office towers, with the oldest built during the oil boom of the 1970's by now banker/developer Joe Canizaro, but the last office tower was built in the 1980's.

The office tower movement began as the Canal Street retail sector started a decline and the parallel Poydras Street became the place to be, but no new office towers have been constructed in the last 35 years in New Orleans.

Current Office Market For Lease

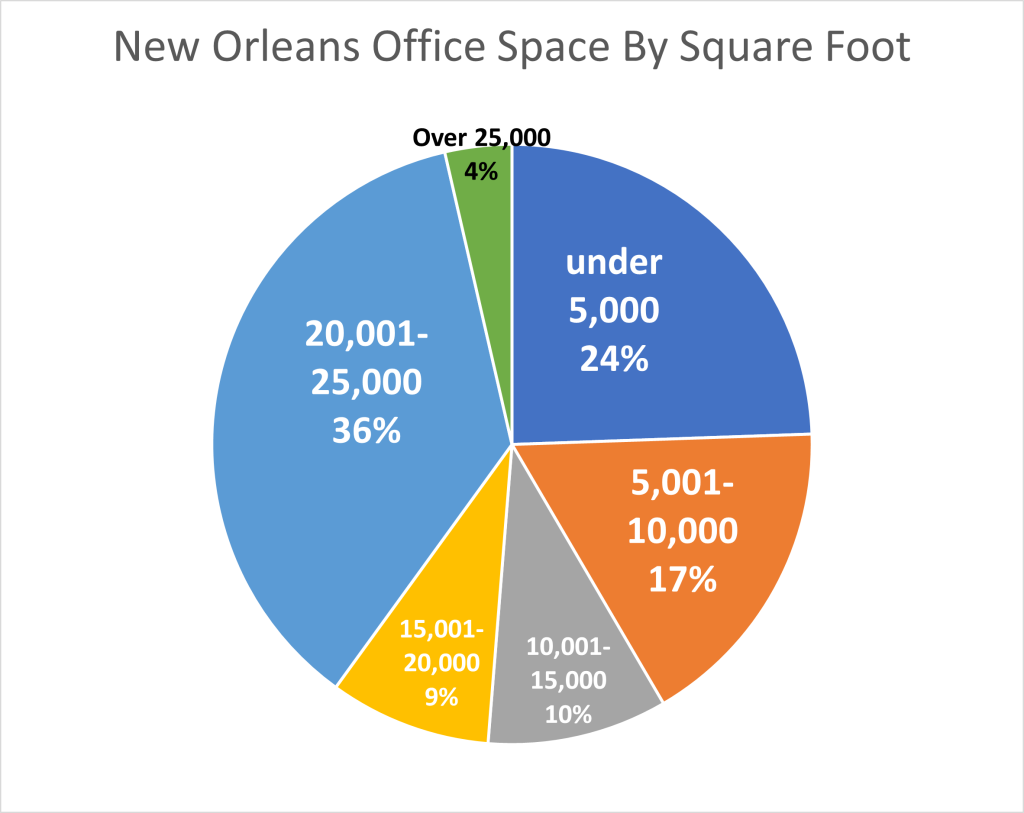

New Orleans Office Space For Lease By Size

Currently there are 95 office properties with space for lease in New Orleans, with a total of 493 listed individual spaces. Of the 493 spaces for lease, the largest number of square feet for lease is between 20,001 and 25,000 square feet in size, with 36%, or 1,048,003 SF for lease total.

This has major implications, since these are usually full floor spaces that the landlord does not want to subdivide; so for the space to be leased, you would need a large company coming into the area with 50-100 employees, looking for office space, or you would need a law firm, accounting, engineering or architectural firm to relocate out of an existing space. New Orleans has none of those.

The conclusion is that the majority of these large office spaces will never be leased, especially because landlords refuse to reduce the rents to attract tenants, since the value of the building, and thus the loan to a lender, is connected to the current asking rent rate, as well as net operating income. As values fall, lenders will require owners to add funds to maintain equity/loan ratios, causing highly leveraged properties to default.

The Good News About Office Lease Rates

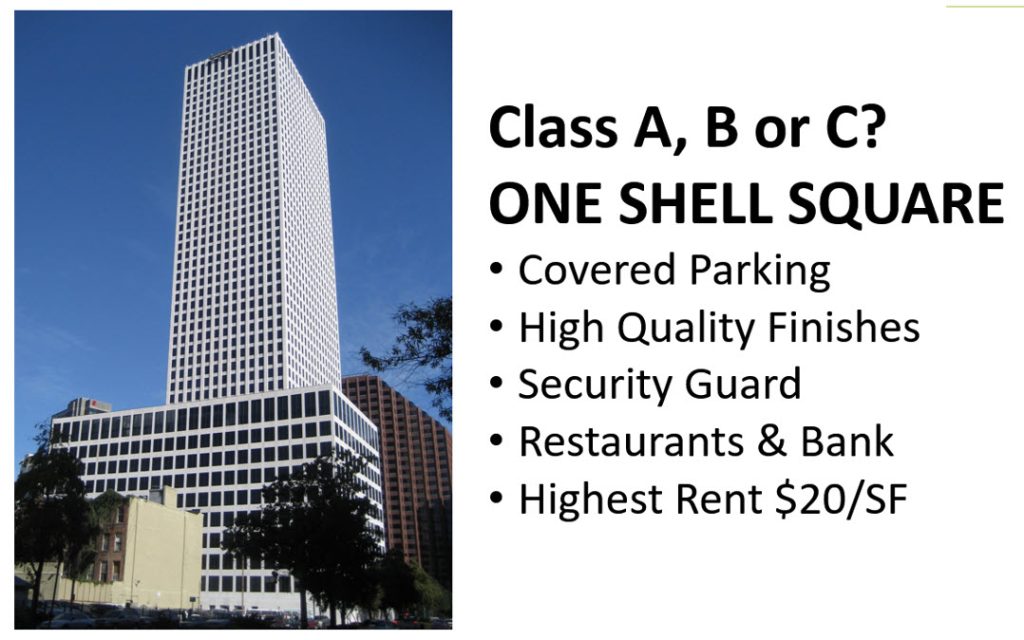

One Shell Square-Once The Best, Now Ailing

The good news is that the next highest bracket of listed office space for lease is a size less than 5,000 square feet, which accounts for 24% of the market and 68% of the number of listings. This size office space can attract newer businesses such as start-ups, which we find in New Orleans because people visit, then love the culture, and then decide to stay and open or relocate a business.

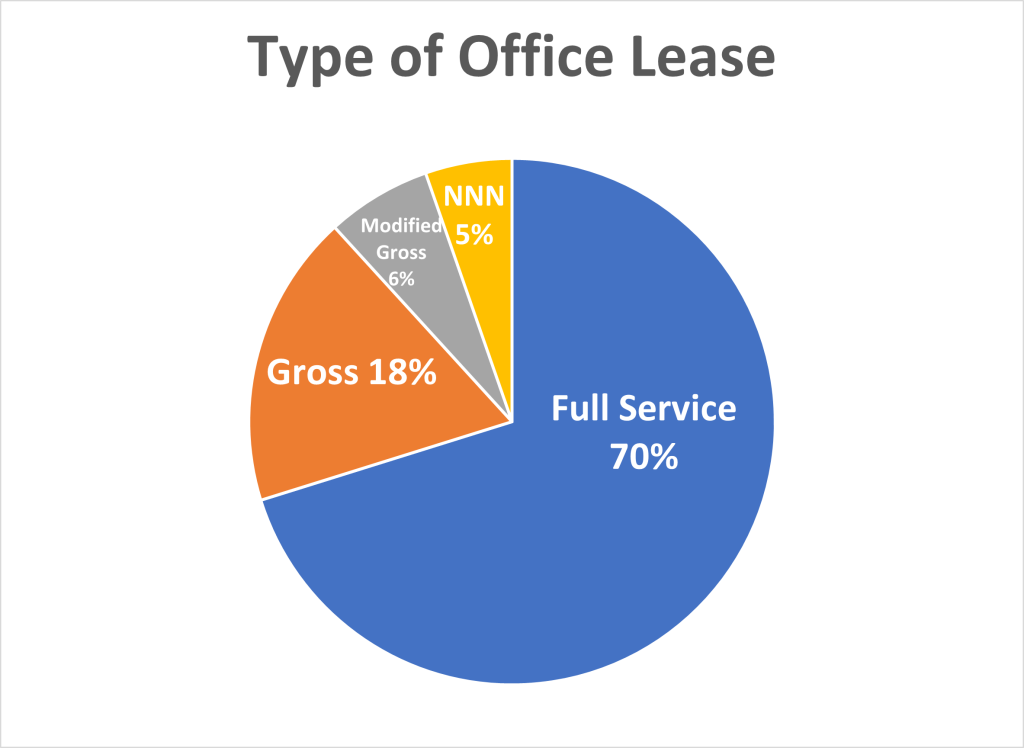

That Lease Is Gross

Type of Office Lease Prices

About 70% of the square footage for lease, 1,926,363 SF, is priced as full service, which means all utilities are included in the rent rate. Only 5% were triple net, which means all operating expenses are passed on to the tenants, including, property taxes, fire insurance and unusual but expensive issues like restriping the parking lot. Here are Moody's definitions of the various types of lease pricing:

Gross: The landlord covers base year expenses except for janitorial, utilities, and outside trash removal.

Full Service: The landlord pays all or most of the operating expenses, taxes, and janitorial.

NNN: Tenant pays all operating expenses, taxes, and insurance.

Summary

New Orleans Skyline

The New Orleans office market reflects the national trend in declining occupancy, and not necessarily due to Covid. The population in New Orleans has been declining over the last 10 years, and recently was named as the number one city in the nation for population decline rate. The long term office market trend follows population growth, and a movement by employers to force employees back into the office won't fix it.

One solution offered is to convert office towers to needed residential space. We negotiated one of the largest office leases in New Orleans, 75,000 square feet, representing building owner ENI who leased several floors to the adjacent Hyatt Hotel to be used as hotel space, and we concluded that business model will not work for the other office towers in New Orleans, It is just not economically feasible.

Compounding the issue is that office tower owners are unwilling to lower prices to increase demand. The result will be that highly leveraged office towers will fall back into the hands of lenders, continuing the decline in the Class A office market, and decimating the Class B office market who will be forced to lower prices much further.

Stay tuned for our next report on prices of the New Orleans office market and also trends in the Metairie office market. For more information on prices and office space leased, catch our blog: A Drill Down Into 2023 vs. 2024 Office Market

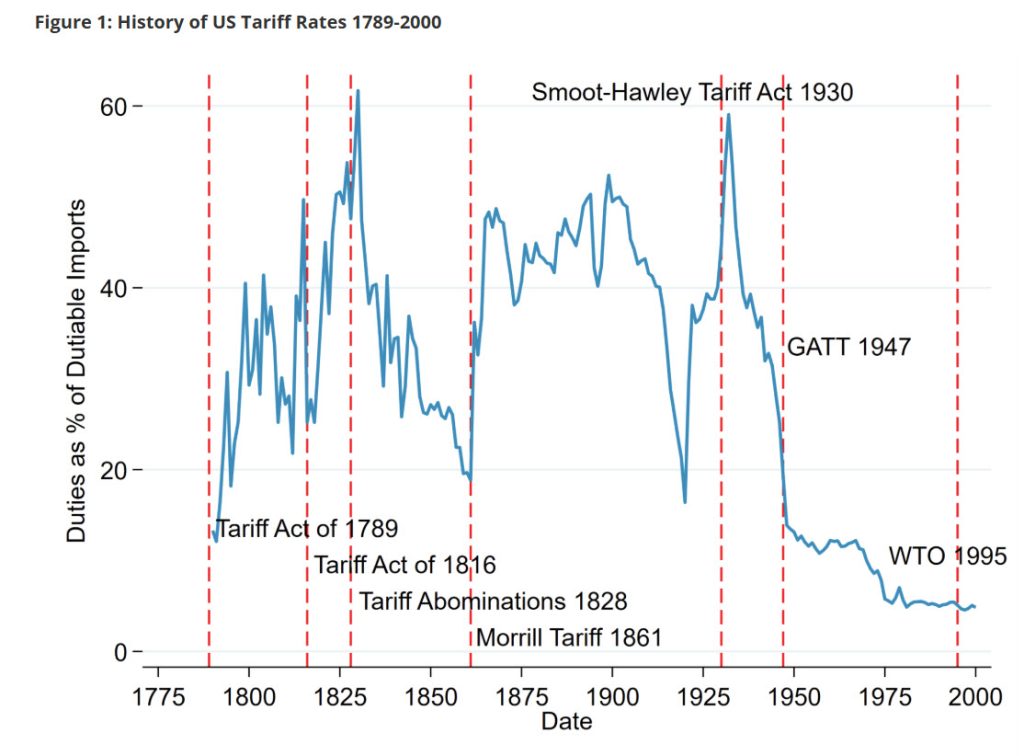

At first glance, imposing tariffs or quotas appear to be the perfect solution to get American industries back on track to prosperity, but the reality is that tariffs steal money out of consumers’ pockets by causing prices to increase, stifling creativity, rewarding inefficiencies and destroying the competitive drive that allows a free market economy to deliver cheaper, smarter and innovative products to you.

If you skipped college or avoided a business degree, you missed the basic economics course that explains why tariffs and quotas work in communist countries but never work in a free market economy. This article refreshes you on Econ 101 and explains why tariffs in America cost you over $70 billion every year.

The price of a good is the intersection, or equilibrium, of the demand and the supply. The chart illustrates the interaction between increased quantity and increased prices for buyers (demand curve) and suppliers (supply curve). The supply curve always rises since, as prices increase, providers of goods want to sell more and the demand curve always declines, since consumers always want to buy less. The intersection of supply and demand tells us the long term equilibrium of price and quantity.

Tariffs and Quotas

A tariff is a tax on imports, paid to the government. Domestic producers are exempt from the tariff. A quota is a limit on the quantity allowed to be imported. The result of both is an increase in the price of the good, from the market price to the new tariff price. American manufacturers get to charge the new price, and manufacturers overseas receive the market price but pay the tariff to the US government. The government gains area “D”, the revenue from the tariff; however, American consumers pay the higher price measured by areas A+B+C+D. Even if the government passes along to consumers the revenue from the tariff, the loss to consumers is still area B+D.

What Can We Learn From Steel Industry Tariffs

America has many precedents that teach us tariffs are bad policy, and the most obvious is the steel industry. Going back 70 years, the steel industry was an oligopoly, with just a few manufacturers and little competition, allowing the industry to raise prices 9% annually in the late 1940’s, twice the rate of wholesale prices.

In the early 1950’s, steel prices increased 4.8% annually at a time when the wholesale price index was falling. In the late 1950’s, steel prices increased 7.1% annually, three times wholesale prices. In 1969, quotas were imposed and steel prices increased 14 times greater than they had in the previous 9 years, during a time of recession and 25% of industry capacity was in an idle state. The result was a lag in technology. American steel companies failed to introduce the oxygen process and continuous casting which put them at a disadvantage. Their oligopolistic pricing policy kept American companies from competing in the world market and eventually allowed Chinese imports to erode their market by producing a better product at a lower price.

Summary

Tariffs and quotas are not sound public policy. They undermine competitive discipline which forces industries to always reduce cost and increase efficiency, driving creativity and invention. Protectionism has a narcotic effect, allowing sick industries to avoid facing up to their problems. Tariffs are bad for consumers, and the math proves it so.

Louisiana Commercial recently negotiated the 10 year lease for medical tenant Velocity Clinical Research who secured 8,000 square feet of space on the 6th floor at 3308 Tulane Avenue in New Orleans. Velocity moved from their Metairie location which no longer met their needs because it did not offer an efficient floor plan.

Louisiana Commercial Realty broker Robert Hand explains, “Velocity came to us for help finding a more efficient office space. While many businesses are moving from downtown New Orleans to Metairie, Velocity is doing the opposite in moving from Metairie to New Orleans. The move made sense for them because the building is in the perfect location and the landlord renovated the space to exactly meet their needs. We negotiated all the minute details of the lease for Velocity and also the landlord so that both got what they wanted.”

Here is a list of features the 8,000 square foot space at 3308 Tulane offered:

Private exam rooms

Reception area

Free parking

Nurses station

High speed internet access

Secure record storage

Certified research laboratory

Refrigerated centrifuge

Temperature controlled pharmaceutical storage

Freezers for specimens at minus 70 degrees Celsius

Backup generator

Velocity is the world’s top clinical research organization, with 63 locations in the US and 34 locations in Europe, conducting clinical trials in infectious diseases to bring successful vaccines to market. For example, Velocity helped conduct studies for approval of a new flu vaccine as well as treatment for asthma.

This is the 8th tenant lease that Louisiana Commercial Realty has negotiated at 3308 Tulane. Velocity’s 8,000 square foot lease ranks as the largest lease for office space in the mid-city area and ranks in the top 5 New Orleans office leases for 2024.

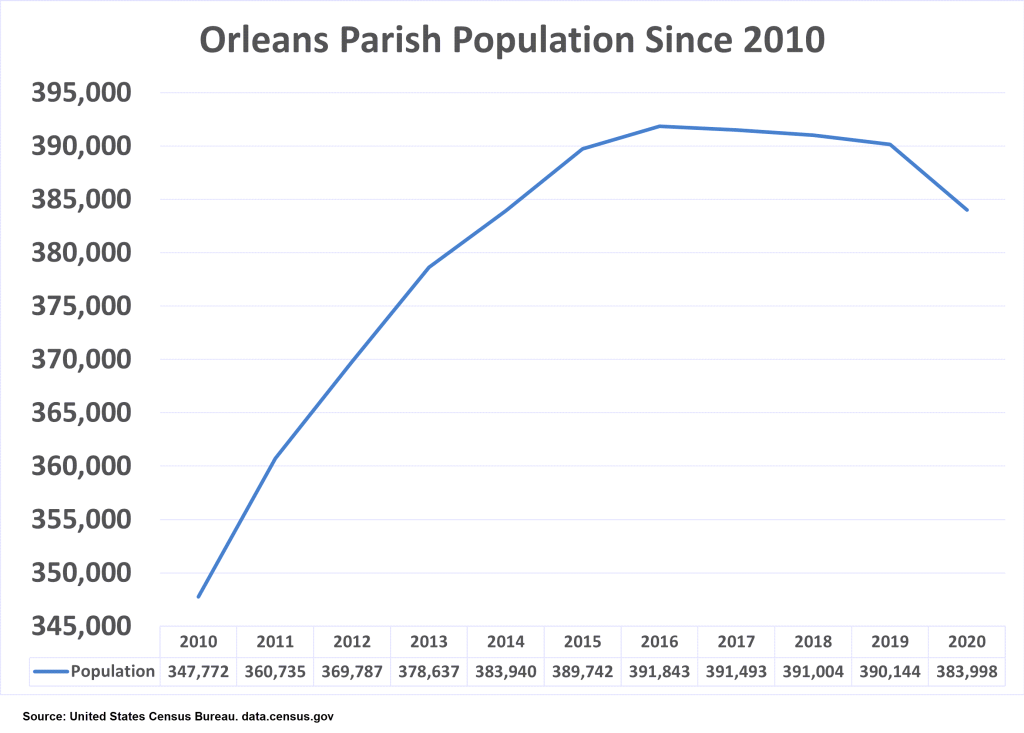

The population in New Orleans and Metairie is declining. Residents are moving out of both cities in droves. Data show that in the last 3 years, New Orleans and Metairie both have the 2nd largest percent decline in population among all the U.S. cities. Tracked by the Census Bureau, the population declined 17,024 last year alone and 45,121 for the last 3 years, which amounts to 4.69% of the total New Orleans/Metairie population. That percent decline is higher than San Francisco, Los Angeles, Pittsburg and Detroit. Only Honolulu has a higher percent decline in population.

Why Population Growth Is Important

The commercial real estate market only grows in areas where population is growing, and the more growth in population, the higher the growth in businesses and commercial real estate. Of the 5 main sectors of commercial real estate: office, retail, multi-family, industrial and hospitality, 3 are dependent on a growing population. Let's look at how each sector is affected by a declining population.

Office Sector

Offices are dependent on new businesses coming into the area or current businesses expanding their employee count. Even with the increase in employees working remotely, the amount of office space leased is usually negotiated for 5 to 10 year periods so companies are committed to office space regardless of whether the employees show up there or not. In order for the office market to grow, landlords need more businesses moving into the area who provide services for a growing population. For example, if the population is growing, residents would buy a home in the area which would cause an increase in other businesses such as real estate agents, landscapers, contractors, appliance and furniture retailers who depend on new home owners. Each new business would have a need for administration which would lease new office space.

1100 Poydras is 4th largest office tower in New Orleans

The decline in New Orleans population has decimated the office market, causing two of the largest office tower owners to be able to collect enough rent to make the loan payments.

1100 Poydras is the 4th largest office building in New Orleans and the owner defaulted on a $56,000,000 loan causing the bank to foreclose on the property.

1615 Poydras is a 475,000 square foot office tower default due to declining rent income and named in the top 5 loan losses in the U.S. office sector with debt of $30,000,000 and liquidated recently for $18,000,000.

1615 Poydras is in top 5 loan losses in U.S.

Retail

The Retail sector depends on consumer spending patterns, which are heavily tracked by data analysis companies. For a retailer to come into a market, they first research how much money is spent by residents within a 5, 10 & 15 minute drive time specifically on goods a business sells, and then the retailer compares that spending to how much is sold by existing retailers. The difference is called a Spending Gap, and the higher the population, the greater the consumer spending and the more likely a business would be successful in that area. Since starting a business is an expensive endeavor, retailers want to make sure the area they target will make the business feasible, otherwise they will just go somewhere else.

Multi-Family

Apartment demand depends on new people moving into a city when they get new jobs or are transferred. All but one of the new apartment developments in New Orleans occurred during periods of growing population after Hurricane Katrina. We brokered 90% of the land acquisitions to make building the apartments feasible, so we should know.

Developers were very specific about the areas they wanted to build apartments in, and target areas where people were moving to. Apartment developments like this usually cost $10,000,000 to $30,000,000 to build, not to mention the time it takes to get them leased up, so the investments requires a high degree of confidence that the population will support he investment.

Summary

It is just common sense that commercial real estate depends on a growing population, but what will surprise you is the correlation and multiplier effect that declining population has on 3 of the 5 sectors of commercial property. New Orleans' trophy for the 2nd highest rate of declining population in the United States is the reality and businesses have to be hopeful but play the cards they are dealt.

The optimistic part of this declining population reality is that we can fix it, but it will take city, state and federal government to change their thinking. Currently New Orleans has a 4.45% tax plus a state tax of 5% on purchases. There is a 20% tax on hotels that tourists stay in. There is a 25% increase in property taxes by the city on commercial property. If government can reduce taxes a little we can gain several times more than that from the increase in business in the office, retail and multi-family commercial sectors.

The Louisiana Real Estate Commission approved Louisiana Commercial Realty's commercial property workshop to train real estate agents on the complexities of commercial property. The workshop is approved for continuing education credits which are required by the commission each year in order for a Louisiana agent to maintain their license. Chapters of our workshop teach commercial real estate agents and investors what they need to know about each of the 6 major types of commercial property.

We Spent Years Creating A Powerful Workshop

The workshop dives deep into the motivations of buyers, sellers, landlords and tenants. Each of these 4 stakeholders has a different objective so a commercial real estate agent must quarterback all the various entities and tactfully guide the decision-makers, government authorities, bankers, appraisers and property owners, who often conflict when interacting with each other.

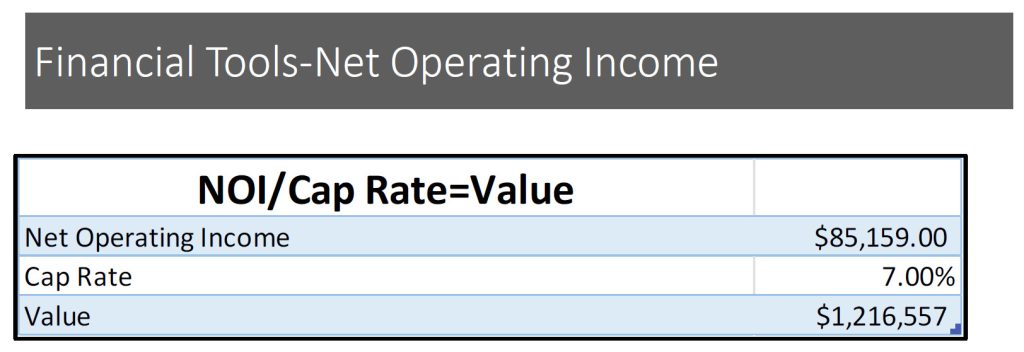

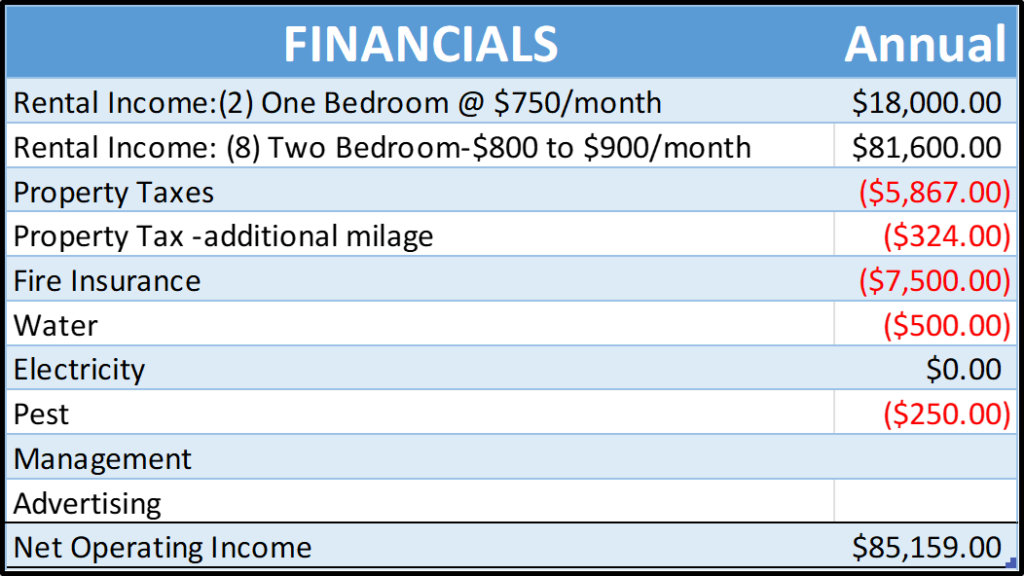

The Workshop Teaches How To Value Commercial Property

The workshop also covers one of the most misunderstood features of commercial real estate: how to value property. We spent years writing appraisals for two of the top firms in New Orleans, so we understand appraisals are only meant for a bank committee to justify loaning money and have little to do with a price at which a property can be sold. The most accurate method of determining a market price for commercial properties that produce rent income is to apply a Capitalization Rate to the Net Operating Income. For example, if a property produces $85,159 in income (revenues less expenses) you would divide that by a 7% Capitalization Rate. This means a buyer should, at most, be willing to pay $1.2 million for that commercial property.

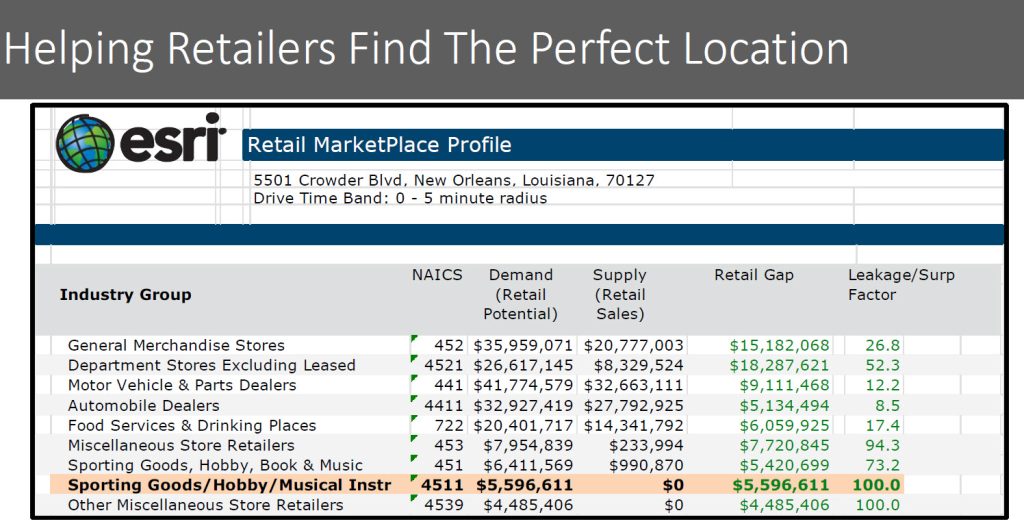

The Workshop Shares Technology To Make Great Decisions

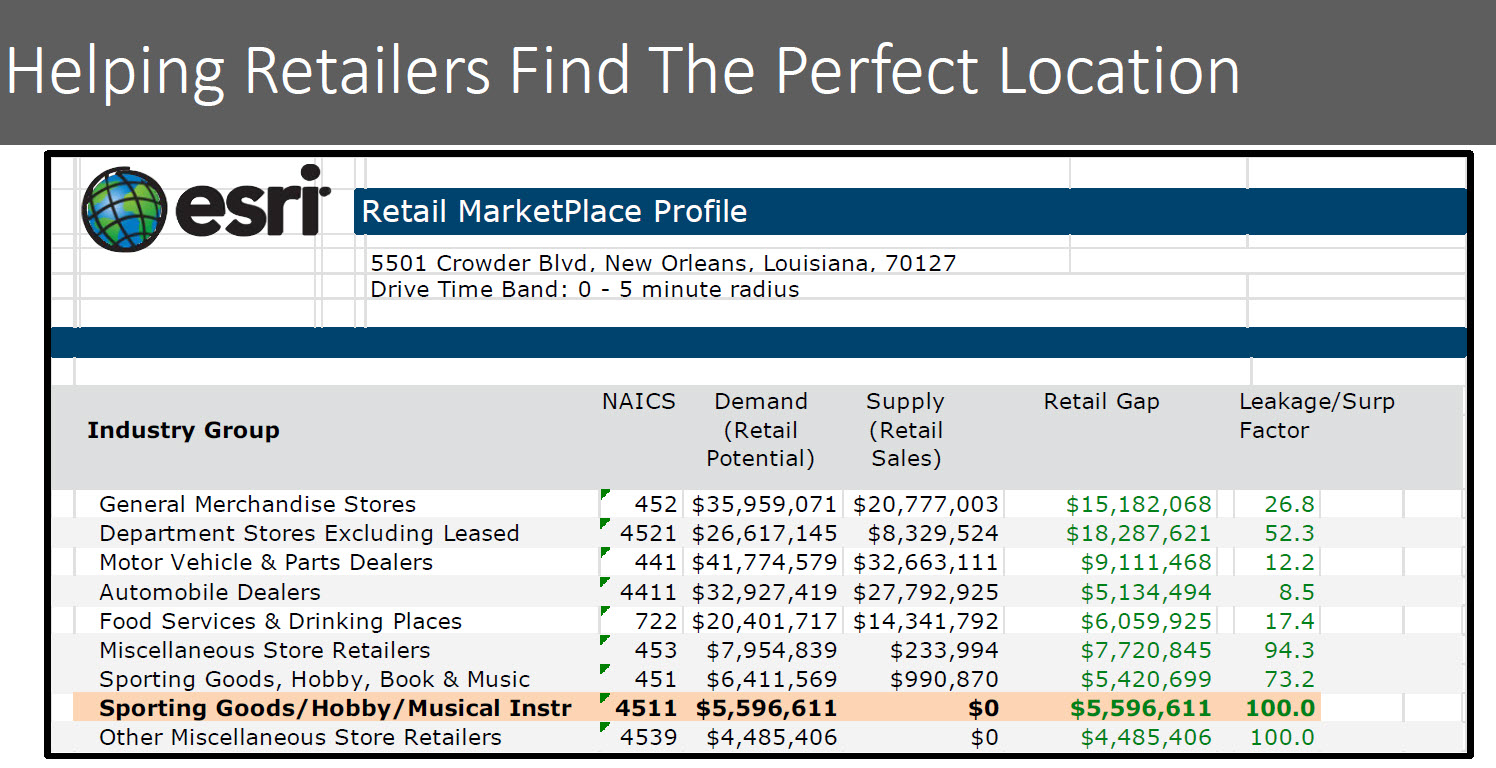

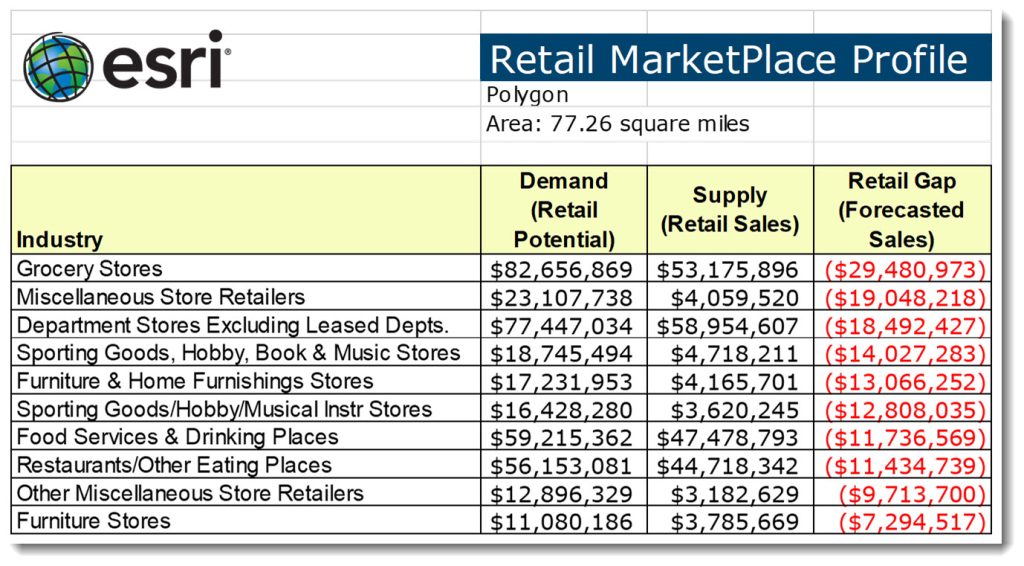

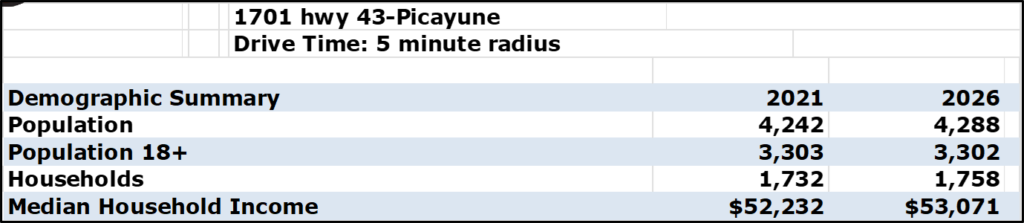

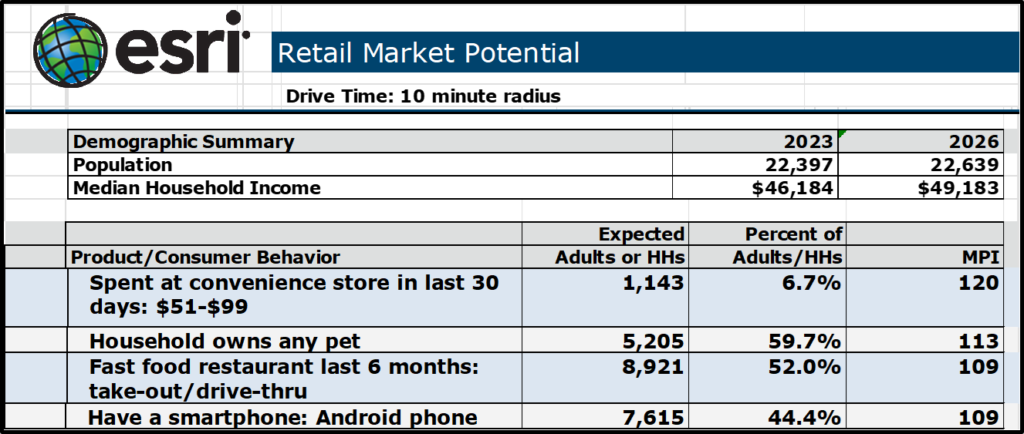

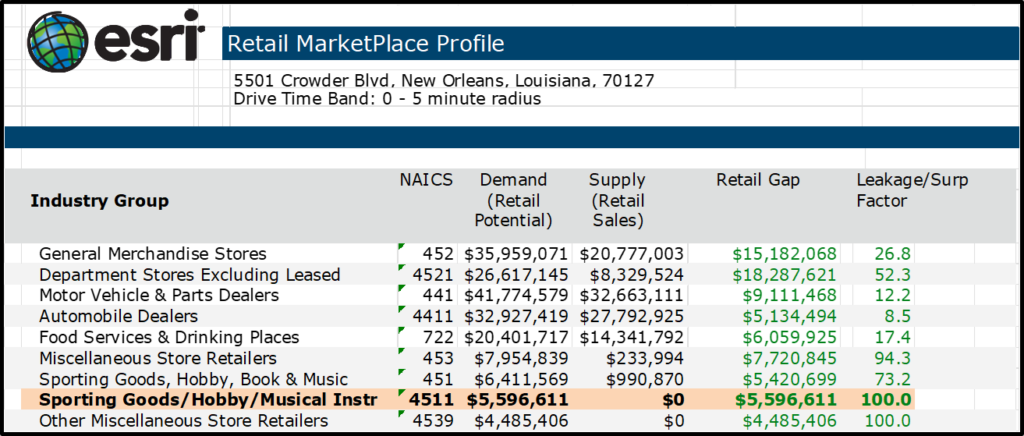

Commercial real estate agents and investors need to be proficient in using technology to determine the best location for their business. Normally agents or investors only know about demographics, including population, income and age; however, finding successful locations requires knowledge about how nearby residents spend their money. This research depicted in the table helps businesses know how residents within a 5 mile radius spend their money. In this example, residents spend $5,591,611 on sporing goods but there is no sporting goods store in the area. The workshop details how to get valuable information to find the perfect location for a business.

Attend The In-Person Workshop

We have 20 chapters in the commercial real estate workshop for agents and investors who want to be proficient in commercial property, so contact us for locations and times.

Want to read more now about commercial real estate? Catch our blog:

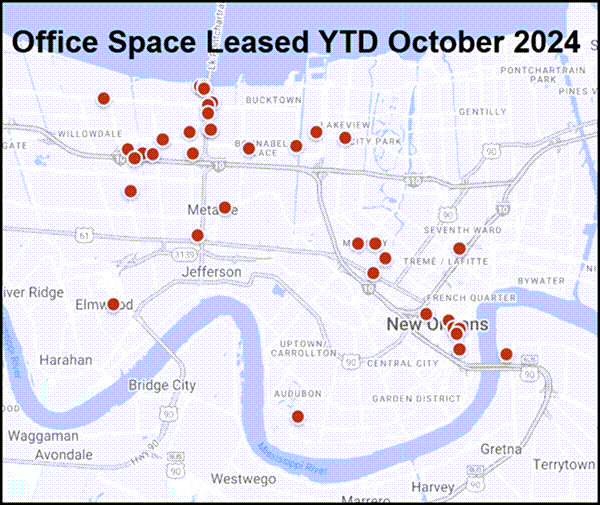

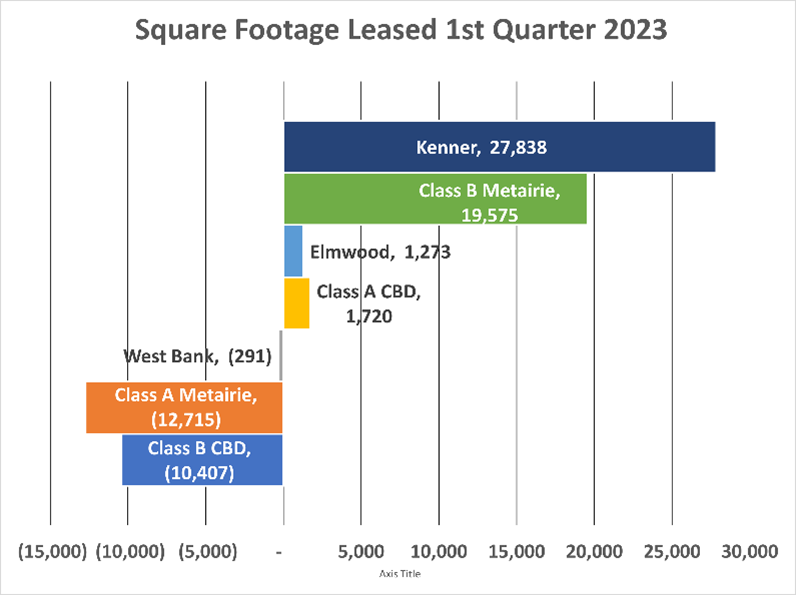

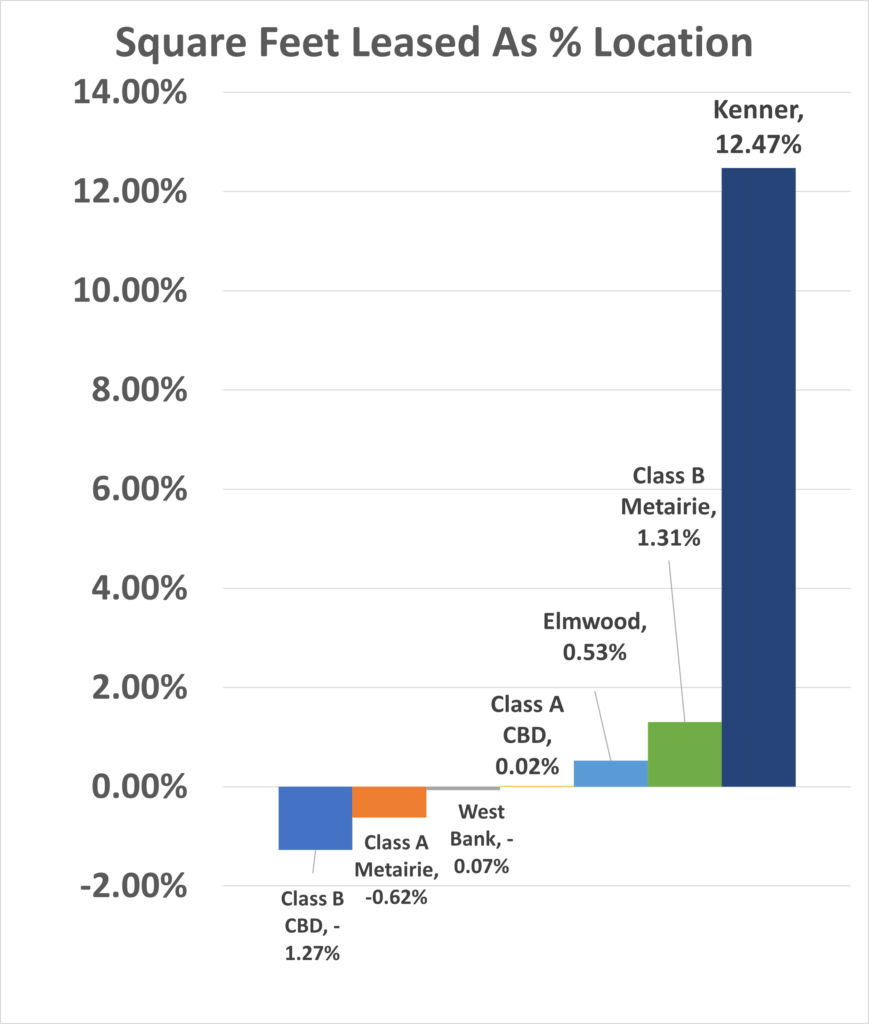

This article drills down into the office market in New Orleans and Metairie, examining 350,000 square feet leased in 143 reported transactions, comparing office space lease terms from 2024 to 2023 and providing insight into office market trends.

2023 Office Square Foot Leased

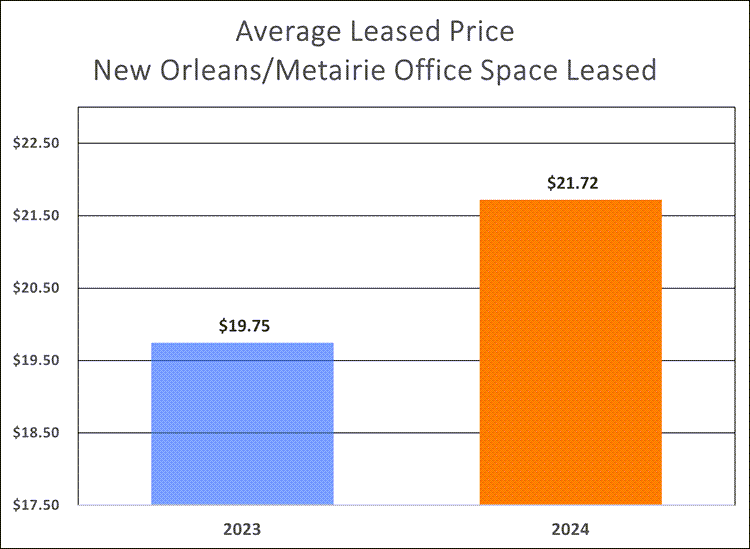

In 2023, 184,885 square feet of office space was leased in 78 listings in 41 properties. The average space was 2,400 SF and leased at $19.75 per square foot, but the operating expense terms varied.

For example, triple net leases comprised only 9% of all office space leased but 59% was leased as full service. The average triple net rate was $16.77/SF and the average full service rate was $21.00/SF. Triple net leases are common in industrial spaces leased but full service is prevalent in the office sector.

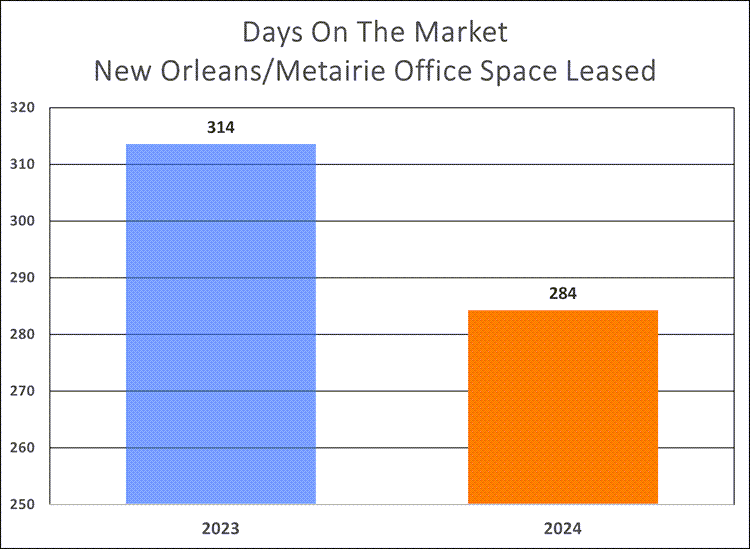

The average space leased is 2,070 SF at $21.72/SF. As of October 31, 2024, there have been 66 office spaces leased totaling 136,000 square feet. At this pace, the year end total is forecasted to be 163,964 square feet.

Comparison of 2024 to 2023

Last year, 78 office spaces were leased in 41 properties, ranging from 300 SF to 12,864 SF, averaging 2,400 SF per space leased. Only 10% of the spaces leased exceeded 5,000 square feet. In 2024, spaces range from 167 SF to 18,000 SF, but of the 66 spaces leased, 60 were under 3,500 square feet.

Summary & Insight

SF Leased: 2024 is forecasted at 163,964, which is a 12% decline from 2023 when 184,885 SF was leased.

Days On The Market: 2024 is showing 284 days to lease office space, down 10% from 314 days last year.

Price: 2024 is averaging $21.72/SF vs. $19.75 last year.

To summarize, lease prices are up 10%, supply is down 12% and office spaces are leasing 10% faster; but the office market overall is soft for the typical agent. Assuming the average lease was for a period of 5 years and each property had one agent, the average 3% commission only produced an income to the agent of $13,000 per property.

For more information on the office market, including detail descriptions of operating expense terms, check out our two most popular articles:

FEMA is on the ground days before hurricanes hit. I should know because I worked for them. Today they have hundreds of staffers organizing relief, distributing 500,000 meals and 800,000 liters of water, with more infrastructure to come.

For flooded homeowners, you can feel like a deer caught in headlights because you just don't know what to do. Mold sets in within 24 hours so you need to take action. This article outlines what victims of flooded property need to do right now, and what it will cost, as told by a Hurricane Katrina survivor.

Flooded? What To Do Right Now

When your home gets flooded, it can be overwhelming. There is so much devastation that you don't know where to begin. The first thing to do is to call all your friends and ask for help, since this is no time go it alone.

You will be amazed at how word can get around and friends will come to the rescue. Here is a list of what you need immediately and how much things cost that you need to ask people to bring you:

Wet/Dry 3 gal, 5 HP Shop Vac-Lowes with extra filters

$ 49.95

$ 49.95

1

portable fans-Lowes

$ 69.99

$ 279.96

4

Total

$ 2,170.46

Once you have your supplies, start with the highest priority tasks. Have your insurance adjuster examine your property, take lots of photographs, and file a claim with FEMA as soon as possible.

You might have a 4 bedroom home but if only 2 people live there, you will only receive FEMA aid for a 2 person house. Save financial records, photographs, appliances. Everything wet that is salvageable must go outside to dry, all else thrown away.

First Things First

Pull up all wet wood flooring or carpet and discard. Mold can set in within 24-48 hours.

Cover salvageable furniture with sheets.

All wet trim and sheetrock has to be pulled out and discarded into 3 mil black trash bags in Brute cans on wheeled dollies. One person should have the job of taking bags of wet sheetrock outside and refilling trash cans with bags. Break up the sheetrock into small enough pieces so they fit into the trash bags.

Get a ruler and mark a line on every wall at least 24 inches from the floor, or high enough to mark where the wet sheetrock stops. Snap a chalk line or use a level to draw a line. Use a box cutter knife or drywall jab to cut out the wet sheetrock. Pull out trim nails with pliers and remove drywall screws.

Broom out large chunks of debris and insulation.

Wet/Vac out water and remaining debris from studs.

Once exposed, studs are clean and free of debris and insulation, spray with bleach 25% mixture, then place institutional carpet blowers near exposed walls to dry out studs. Let fans and blowers run 24/7. Studs should be dry in 2-3 days.

Pull out all wet kitchen and bath base cabinets and store outside to dry, if possible, remove cabinet doors for ventilation.

Soak up standing water with with cotton head mop and clean floors often with sponge mop, so as not to track sheetrock dust to other rooms. Dust does not mop up by itself, so use ZEP Floor Cleaner.

Got office space in New Orleans? We researched all the office space leased last year in New Orleans and discovered some real surprises. Let's get started.

In 2023 only 90 office spaces were leased in New Orleans

Office space for lease in New Orleans totals 2.8 million square feet in 482 listings, with prices ranging from $12/SF NNN to $19.50 Full Service. But are office spaces actually leased at the listed price? This article drills into the New Orleans office market to determine actual lease prices, and we discovered not that much office space has been leased.

30 Years To Lease The Current Office Space

In the first seven months of 2024, only 16 office spaces in New Orleans have been leased, totaling 53,866 square feet at an average rate of $18.59 per square foot on 3,367 square feet leased. At this rate, it will take 30 years to lease all the office space. Full Service leases account for 62% of the total and 87% were less than 5,000 square feet in size.

Full Service accounted for 62% of the office space leased in the first 7 months of 2024.

What Happened In 2023?

Only 90 office spaces were leased in all of 2023 in New Orleans at an average price of $19.13 per square foot, but that doesn’t tell the whole story. The surprise was that 28% of spaces were under 1,000 square feet and 68% were under 2,500 square feet.

68% Is Under 2,500 SF

68% of office space leased was less than 2,500 SF

The smaller spaces are usually leased by upstart companies, or those sole proprietors tired of working from home where they suffer leaf blowers, garbage trucks and barking dogs during their conference calls. New companies are a good sign, but are not the economic driver that New Orleans needs to recover from losing corporate headquarters with hundreds of employees.

70% Is Full Service

Full Service leases accounted for 70% of the total, and prices ranged from $16.99 to $22.61, with the smaller spaces leasing over $20/SF but then the spaces from 2,500 to 10,000 square feet were negotiated down in price to a range between $16.99/SF to $17.80/SF. This reduction in rent is because landlords aways want the larger tenant which leads landlords to have less negotiating power and since there are lots of spaces this size to pick from, tenants were able to secure reduced rents.

Only 4 Spaces Exceeded 10,000 SF

Smaller SF spaces pay a premium rent

The surprise is what happens to prices in the office sector over 10,000 square feet: prices increase. There were only 4 spaces leased in all of 2023 over 10,000 SF in size, and prices averaged $17.88/SF.

All 10 Spaces Over 5,000 SF Located Downtown

All 10 office spaces leased over 5,000 SF were located in downtown

The larger spaces are always in high rise office towers, such as 1100 Poydras Street, and landlords all quote the same price which gives them negotiating power. All 10 of the office spaces over 5,000 SF leased last year were located in or near downtown New Orleans.

Summary, Insight & Forecast

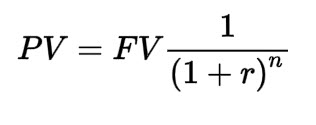

The office market in New Orleans is dead. For such a large city, having only 90 office spaces leased totaling 233,000 square feet in all of last year depicts a picture of doom and gloom. And 2024 is not much better with only 16 office spaces leased totaling 53,866 square feet in the first 7 months. Look for prices to fall as soon as landlords understand rented space at a lower price means a higher present value than a higher price after 2 years of vacancy. After prices reach equilibrium, tenants will come back to New Orleans office spaces and the momentum will shift. Meanwhile, the opportunity will be to buy depressed office property during this down cycle at prices you will never see again, get it leased, then sell at the next peak.

The days are long gone when you can just put up a sign and wait for phone calls to sell or find tenants for commercial property. This article dives into the top commercial databases in Louisiana and Mississippi to expose strengths and weaknesses in using technology to get commercial sold or leased. The top commercial databases are LACDB, MSCREX, Loopnet and CREXI which are utilized by commercial agents to find tenants, sellers and buyers, but we've discovered that the database with the most listings is not the one that works best. Let's get started.

Finding Tenants For Your Commercial Property

The pie chart above shows the 6 common ways, called marketing channels, that agents can sell or lease commercial property, and the highest estimate is that 55% of prospects are found using commercial databases. In Louisiana there are 3 commercial databases, each having its own reach and costs ranging from $1,000 to $30,000 annually. Here is a deep dive into each database and its strengths.

LACDB

The Louisiana Commercial Database (LACDB.com) reaches 1,500 commercial agent members in Louisiana who post 8,539 listings, with 4,007 properties for sale and 4,532 for lease. The database also has 314 commercial listings in Mississippi, with 187 for sale and 127 for lease. There are free email blasts to promote properties to agents, limited to one daily but unlimited blasts to clients. LACDB uses Catylist as their software provider plus you have access to a national database called Commercial Exchange which gives you wider distribution. Costs for subscribing to the database are $720 annually and agents can add SiteLink to have their listings automatically populate their website for an additional $800 annually. Agents do not have to be a member of the National Association of Realtors before they can subscribe to the database which reaches mostly Louisiana and Mississippi agents and brokers because subscriptions are the least expensive. LACDB offers market statistics showing the average sale or lease price and days on the market in each of the major categories: office, industrial, retail, shopping centers, hospitality and multi-family.

MSCREX

Mississippi Commercial Real Estate Exchange has 106 members who are commercial real estate agents and brokers, with 1,284 listings divided into 680 for sale and 604 for lease. The cost is $720 annually, up from $600, to subscribe to the database which allows you to post listings but it is owned by the Mississippi Association of Realtors, so membership in the National Association of Realtors and Mississippi Association of Realtors is required, increasing the cost an additional $454 annually. MSCREX uses the Commercial Exchange platform which is owned by Moody's, so listings here get regional exposure for tenants and buyers seeking property, but listings only get in front of 106 members in Mississippi.

LOOPNET

Loopnet.com has 1,100,000 properties listed by 300,000 commercial agents nationwide. The marketplace gets 11,000,000 unique visitors monthly. For its massive size, Loopnet.com only has 656 listings for sale and 368 for lease in Louisiana, and in Mississippi has 788 for lease and 726 for lease.

This database brings in tenants and investors both locally and nationwide because Loopnet was purchased by CoStar recently, giving it national exposure; however, not everyone can see a listing on Loopnet. Agents can post listings without paying to be a Loopnet subscriber, but those listings are marked as Basic which are not shown to anyone except paid CoStar subscribers and very few agents subscribe to CoStar because they require everyone licensed under a Broker name to pay. It gets very expensive and just not feasible for most listings.

Loopnet offers 4 platforms: Basic (free), Silver ($5,000 annually for 4 listings and 10 listings for $8,400 annually), Gold ($8,400 annually for 4 listings), Platinum ($14,000 annually for 4 listings) and Diamond ($30,000 annually for 7 listings). The Diamond level offers:

Higher exposure and a dedicated marketing specialist.

Targeted digital marketing strategy that keeps your property front and center across the web through retargeting.

Professional architectural imagery, videography and 3D tours.

CREXI

CREXI Database Has Almost 10,000 Listings In Louisiana & Mississippi

CREXI.com has 1 million commercial real estate agent subscribers but an average 2 million buyers, brokers, and tenants each month exploring over $2 trillion of property value nationwide. Crexi has 2,367 properties in Mississippi for sale and 1,212 for lease, and 2,771 for sale in Louisiana and 3,587 for sale. Crexi Pro cost $4,800 annually for unlimited listings.

Summary

The Highest Number Of Listings Are Posted By The Database With The Fewest Agents

In utilizing a database to reach tenants and commercial agents directly, not all databases are the same. Most local agents who can bring tenants and buyers to a listing subscribe to LACDB.com since it is the most affordable. LACDB only reaches 1,500 agents so, in the chart above, their agent count column is barely visible when compared to the other databases; however, those are the local agents who often have qualified tenants and buyers as their clients and are seriously looking for property in Louisiana and Mississippi.

CREXI is a fairly new database but already has almost as many Louisiana and Mississippi listings as LACDB plus provides a national reach with 1,000,000 agents and investors as subscribers. Loopnet recently merged with CoStar and anything other than a Basic listing gets Louisiana and Mississippi property in front of prospective tenants and buyers nationally. If your property is above average in size, you may not find tenants or buyers easily because the Louisiana/Mississippi economy no longer drives large companies to the area. If you need to reach larger markets such as Houston, Dallas, Nashville or Miami, the Crexi database is for you.

Currently a Louisiana licensed real estate agent can transact business in both residential and commercial real estate, even though agents are not required to be trained in even the basics of commercial property. All agent licenses must be issued by the Real Estate Commission. Agents are independent contractors, not employees, and the license is always held by a broker not the agent themself. The broker can void the license at any time for any reason, leaving the agent unable to practice any real estate business.

No Training for Residential Agents By Their Broker In Commercial Real Estate

Despite the power and responsibility a real estate broker has for their agents, no broker currently trains their agents in even the basics of commercial real estate. Brokers have lots of regulations dictated by the Real Estate Commission, but training in commercial real estate is not required. Since commercial real estate is vastly different from residential real estate, the result is a disaster. When the residential agent who is inexperienced in commercial real estate tries to transact business in the commercial arena, they usually end up harming their client by allowing a faulty contract or paying too much or suffering a difficult transaction which most likely fails to happen. It doesn't have to be that way and Louisiana Commercial Realty is working to change that.

What Other States Require Training In Commercial Real Estate?

None. In promoting residential agent training in commercial real estate, the question always comes up: why doesn't the Louisiana Real Estate Commission require a commercial license? This leads to another question: what other states require a separate real estate license for commercial transactions? So we contacted all 50 states and the answer is: none. No other state requires a separate commercial real estate license. Louisiana would have to be the first.

98% of Residential Agents Want Training In Commercial Real Estate

We polled all 20,000 Louisiana licensed real estate agents to determine if demand exists for basic training in helping clients with their commercial property needs. This includes buying, selling or leasing office, warehouse, apartments, retail, restaurants or hotels. Of the residential agents who responded to the survey, 98% said they would be interested in commercial training, and 50% had already completed at least one commercial transaction within the last 2 years.

Training In Basic Commercial Real Estate Did Not Exist, So We Created It

Louisiana Commercial Realty utilized their 20 years of experience in both commercial property management and also leasing to create a 2 hour workshop specifically for residential agents. We already made progress and presented the workshop to the Real Estate Commission and the Louisiana Association of Realtors, and also to Berkshire Hathaway agents who mostly transacted residential business.

How It's Done

Our workshop details all aspects of a commercial real estate transaction and teaches residential agents how to successfully navigate the nuances of commercial real estate.

Chapters of our workshop teach real estate agents what they need to know about the 6 major types of commercial property to help their clients. The core focus dives deep into the driving factors for buyers, sellers, landlords and tenants. Each of these 4 stakeholders has a different objective so a commercial real estate agent must quarterback all the various entities and tactfully guide the decision-makers, government authorities, bankers, appraisers and property owners, who often conflict when interacting with each other.

Technologically Proficient

Commercial real estate agents need to be proficient in using technology to solve their client's problems. One example is how residential agents can help a retail client determine the best location for their business. Normally, residential agents only know how to provide demographics that include population, income and age, but finding successful locations requires knowledge about how residents spend their money in nearby businesses.

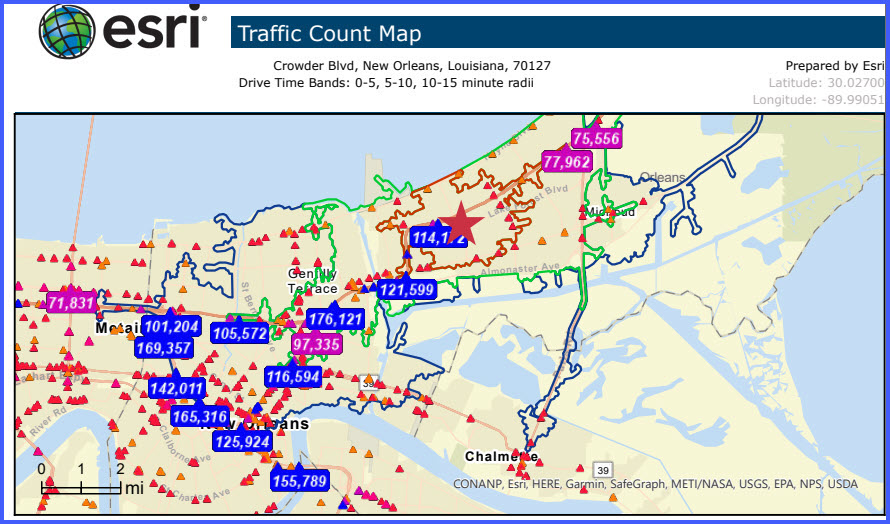

For example, our research for a listing at 5501 Crowder in New Orleans showed within a 5 minute drive time that residents spent $5,591,611 on sporting goods-but there is no sporting goods store in the area. That means residents are traveling outside the area to spend their money; therefore, a sporting goods store in that location would do very well.

This research helps residential agents discuss with sellers and landlords how they will go about finding buyers and tenants. It also helps residential agents show prospective tenants that their business, such as a sporting goods store, can capture $5,591,611 of revenues from day one. This information is easily available but few residential agents know how to access and utilize it. We show them how.

Determining Value

One of the most elusive chapters in the "how to" workshop is valuing commercial real estate. We spent years writing appraisals for two of the top firms in New Orleans: Truax & Robles Appraisers and also Argote & Derbes, so we understand appraisals are meant for a bank committee to justify loaning money but should not be used as a realistic price at which a commercial property can be sold.

If commercial properties produce rent income, the best method of determining market price is to apply a Capitalization Rate to the Net Operating Income. For example, if a property produces $85,000 in income (revenues less expenses) you would divide that by a 7% Capitalization Rate. This means a buyer should, at most, be willing to pay $1.2 million for that commercial property.

Summary

The current absence of training harms the general public and fails the licensed real estate agent. We hope to play a small part in changing that by providing training for agents who dabble in commercial transactions but mostly make their living from residential transactions. If this idea is of interest to you, just contact us today to schedule a free commercial real estate training session.

If you would like more information on the technology available for commercial real estate, we have hundreds of articles on the commercial real estate industry, including popular topics such as prices, zoning, reading flood maps and inflation. Check out two of our popular blogs:

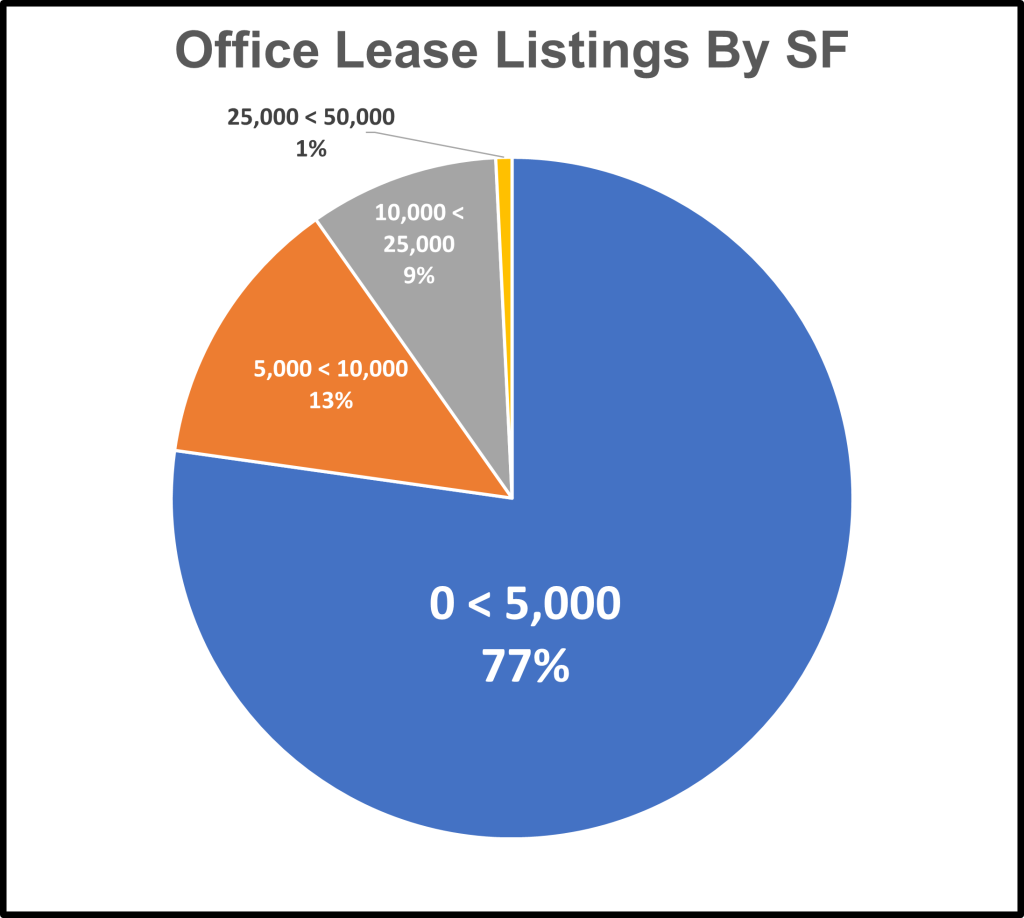

We examined the 2,723 office spaces for lease in Louisiana totaling 8,700,000 square feet, and calculated the average listing to be 4,150 square feet priced at $18.76 per square foot. But that doesn’t tell the whole story. Office space can be priced nine different ways, ranging from Triple Net, which adds on operating expenses, to Full Service which is priced to include electricity, water, taxes, insurance, janitorial and even landscaping. This article takes a deep dive into today's prices of office space across the entire state, including how prices are quoted and who the agents are that lease the most office space.

Only 1% of Office Space For Lease Exceeds 25,000 SF In Size

77% of the Louisiana office space is under 5,000 SF in size

Of the 2,723 office spaces for lease in Louisiana, approximately 1,600 spaces with 77% of the square footage are under 5,000 square feet in size. Only 10% of the spaces exceed 10,000 square feet and only 1% exceed 25,000 square feet. This small size office market is a reflection of the types of businesses in Louisiana which has a lack of corporate headquarters and major corporations which need large office spaces.

Prices Depend On Pricing Type

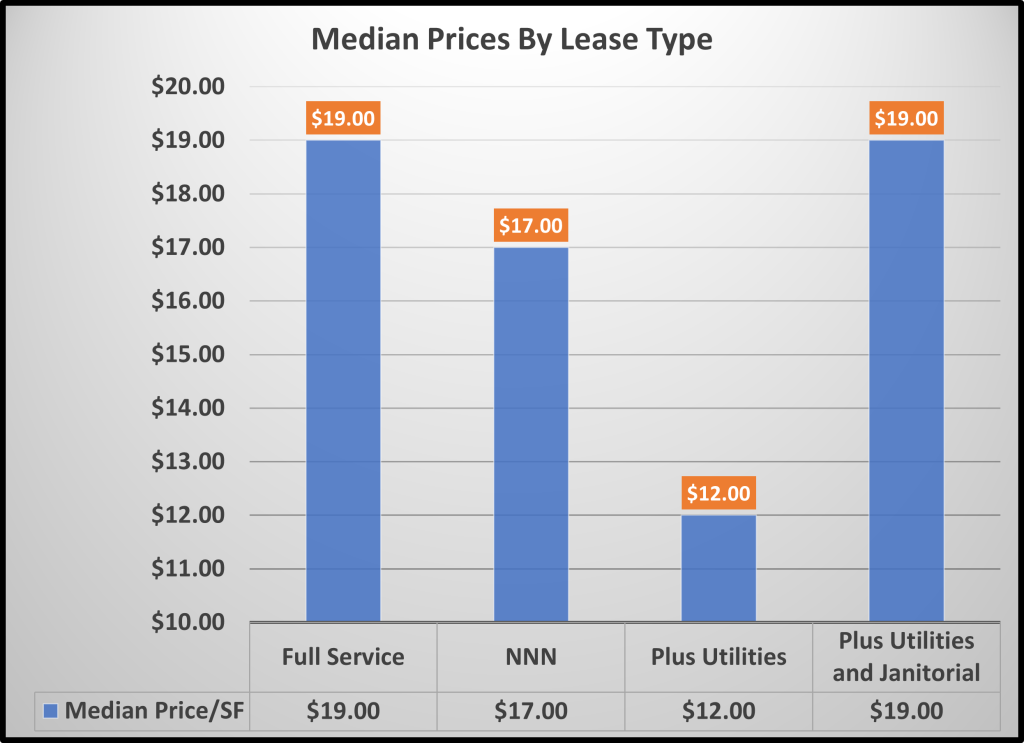

The average Full Service office space is priced at $19/SF

Pricing office space for lease comes in a variety of terms, and the fine points of these terms usually get negotiated during the lease review stage. Here are the major types of office lease pricing we discovered:

Full Service (also known as Gross)-the price quoted includes the base rent plus all other common operating expenses. The landlord pays all costs of electricity, water, property taxes, property management fees, landscaping and hazard insurance.

Modified Gross-includes a base rate and only a few operating expenses are passed along to the tenant. This pricing type usually adds on electricity and water, which are charged to the tenant since most office buildings do not have separate water or electrical meters for each space. The total cost is allocated to each tenant based on the square footage, and is called “additional rent” in a lease. The pro-rata costs are estimated and billed monthly, but reconciled at the end of the year when the true operating costs are known.

Triple Net-Quoted as a base rate but adds on all operating expenses, called common area maintenance, which are passed along separately to the tenant. There may be language in a lease that allows a stop on separate controllable operating expenses versus uncontrollable operating expenses such as property taxes and hazard insurance. The stop would place a cap on the percent increase of expenses that is paid.

We examined 2,723 office spaces for lease in Louisiana and found a range of rates from Full Service to Triple Net (NNN), but also a variety of both. Notice in the table that the quoted Full Service rate of $19 per square foot equals the same as the quoted NNN rate plus utilities and janitorial. This means there may be some additional expenses added that are called utilities but are not. The lowest rate of $12 per square foot plus utilities can be deceiving, since electricity cost can easily average $3 per square foot, water $1 per square foot and janitorial averages $2 per square foot.

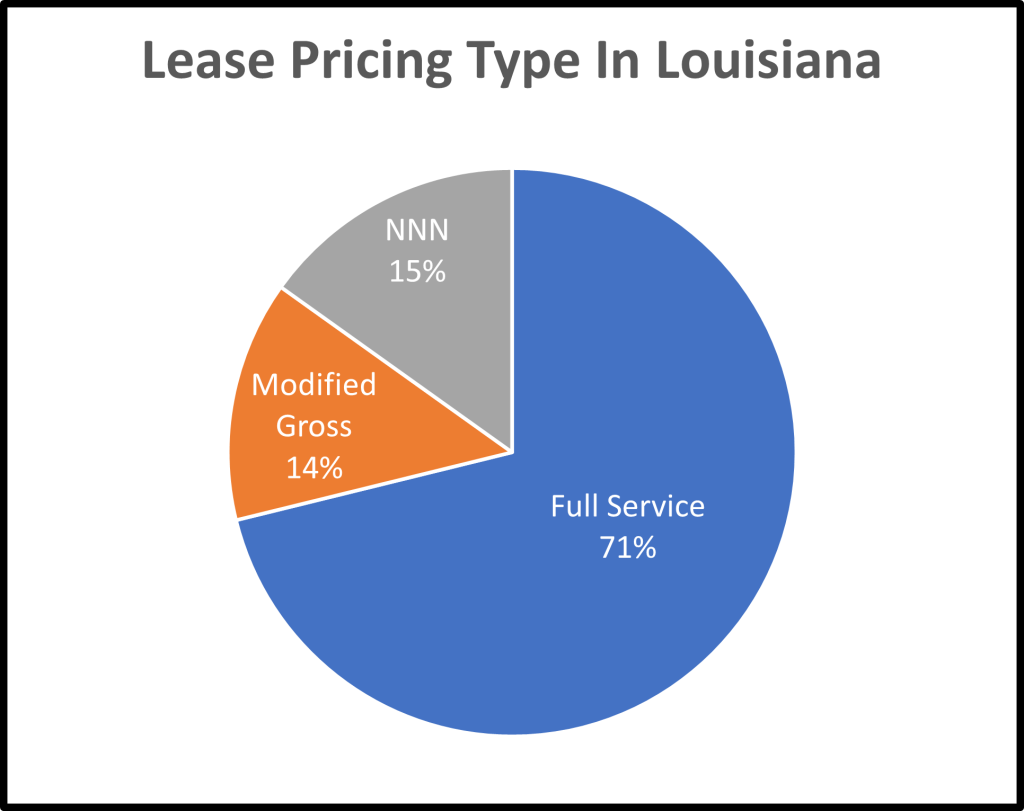

Majority of Listings Are Priced As Full Service

71% of all Louisiana office square footage is quoted as Full Service

Most office space for lease in Louisiana (71% as measured by sector square footage) is priced as Full Service, which includes all expenses except parking. Modified Gross and Triple Net pricing totals 29% of all listed square footage. One reason may be that the majority of office space for lease is in high rise office towers which are always priced as Full Service. The Triple Net pricing is usually associated with suburban locations and older, less attractive, properties, so they quote lower rates but attempt to pass along operating expenses to tenants.

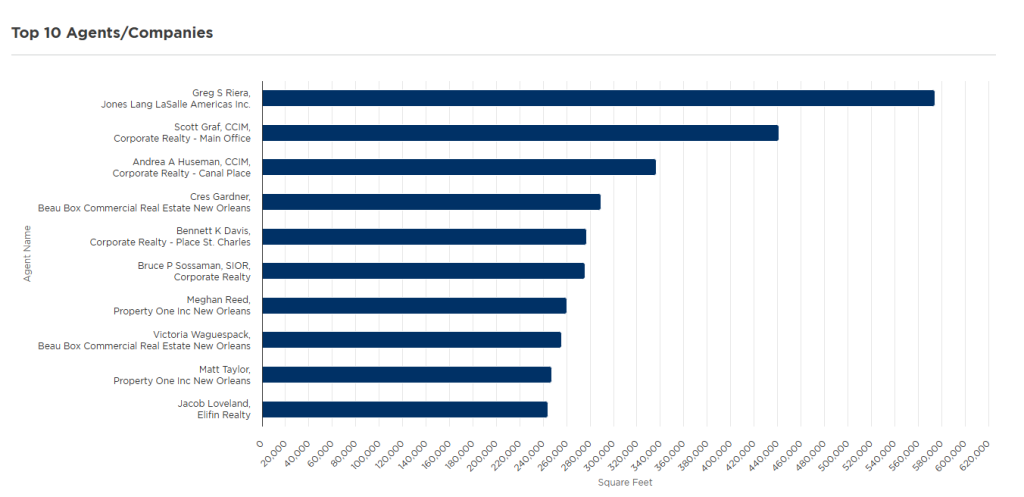

Who Are The Agents Representing The Most Office Space For Lease?

Source: LACDB/Moody's

While Cres Gardner with Beau Box has the most listings at 65, Greg Riera with national Jones Lang LaSalle is the top agent with 574,521 square feet listed, all in downtown office towers that were hit hard by COVID so they have lots of vacant space.

Summary

In summary, the office market in Louisiana is unique. Despite having millions of vacant square feet in downtown office towers, prices quoted have so far remained high as if strong demand for office space still existed. Often the actual lease price is negotiated down and includes some hidden buildout allowances. Full Service office space is about 71% of the 8,700,000 square foot market with an average list price of $19 per square foot, and 77% of the office space for lease is small at 4,150 square feet.

For more information on commercial property prices, read our articles:

Got commercial property to sell? It will not only take much longer than you think but will bring you insurmountable obstacles along the way. Here is how we get it done.

Beauty Connection tenant at 5495 Crowder Boulevard

Louisiana’s economy is not booming like Texas or Florida. Even Alabama is thriving. Louisiana is a great place to live with a fascinating culture but a difficult environment to get business done. That means selling commercial property in Louisiana takes longer than most owners can imagine and will involve overcoming lots of obstacles. The average time to lease or sell commercial property anywhere is the state is 212 days. That is why when selling commercial property, you have to be careful with whom you do business. This article explains how commercial property gets sold and what to look out for.

5495 Crowder is a 24,000 SF building on 2.2 paved acres