The most popular method of appraising commercial real estate is not the most accurate. Usually we compare past sales of property and apply the price per square foot, but this is valid only if all the properties are homogeneous, which is never the situation. Let's examine three methods of valuing commercial real estate.

Sales Approach

The most common method of valuing commercial property is the least accurate, because it only works if all properties have the same characteristics. Called the Sales Approach, it requires gathering the sales price of nearby comparable property, then making adjustments for different traits. This leads to inaccuracy, since the unique quality of real estate is that location can contribute greatly to how a property is used which determines what its value might be, and no two properties can occupy the same location. Other characteristics such as floor plan, parking, zoning, ingress and egress can also contribute greatly to value.

Cost Approach

Sometimes, owners value real estate based on what they paid for it, or what someone last offered for the property, or the cost to build the property new. In reality, the cost of property has little to do with market value, and an offer made by one buyer does not mean a different buyer would value the property at the same price. The market value is the price a property would bring in an open and competitive market, with a willing buyer and seller knowledgeable about the facts. The cost approach works when you have the time, financing and a reliable contractor to build an alternative structure.

Income Approach

Whether you own stocks or bonds or real estate, the best method of valuing an asset is the present value of all future cash flows. The underlying principal is that a dollar one year from now is worth less than one dollar today, because you could invest that dollar today at some interest rate which will grow in one year to a value of more than one dollar. Here is the math:

DPV=FV / (1+i)n where

DPV is the discounted present value of the future cash flow (FV),

FV is the nominal value of a cash flow amount in a future period;

i is the interest rate, which reflects the cost of tying up capital

n is the time in years before the future cash flow occurs.

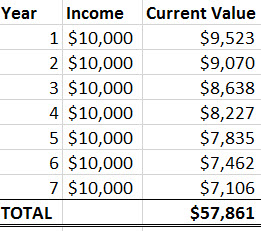

Let’s put this information to work and say a property delivers $10,000 annually in Cash Flow After Taxes. The current value is the sum of future cash flows. You calculate each year’s cash flow, discounted back at an interest rate you could earn on other investments. Let’s assume 7 years at a 5% interest rate and change the n value to match the number of years in the future.

In summary, $57,861 today is the same as $10,000 for 7 years, assuming 5% interest rates. Therefore, if a property had a 7 year lease that produced income of $10,000 annually, the current value of that lease income alone would have a value of $57,861. If an investor required a 10% rate of return, he or she would be willing to pay $578,610 for the property, just to get the lease income.

Not all income is the same however. Let's examine how to determine cash flow income.

Determining Cash Flow

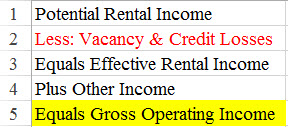

With commercial real estate, the best measure of income is called Cash Flow After Tax, and here is how it is derived.

Potential Rental Income

- Vacancy and Credit Losses

- Operating Expenses

- Annual Debt Service

- Tax Liability

= Cash Flow After Taxes

Determining Operating Expenses

Operating Expenses do not include:

Interest

Depreciation

Capital Expenses

Personal Income Taxes

Reserves for Repairs and Maintenance

Tenant Improvements

Real Estate Commissions

Operating Expenses do include:

Property Taxes

Insurance

Management Expenses

Repairs

Utilities

Source: CCIM Financial Analysis, "The Appraisal of Real Estate", 14th edition, Mark Rattermann, MAI, SRA.

Determining accurate prices for commercial real estate can be elusive. It's not what economist call a highly competitive market such as buying a stock or a bond where the bid (highest price for buyer) and ask (lowest price for seller) is actively visible for all to see. Market prices for commercial real estate can be vastly different from appraisal valuations and can vary widely by property type, location and tenant. The unpredictability of determining a price means that the person with the most knowledge makes the best decision and capitalizes on the opportunity that others may not recognize. This article researches the commercial property markets in Louisiana and Mississippi to provide the knowledge with which you can make better commercial real estate decisions.

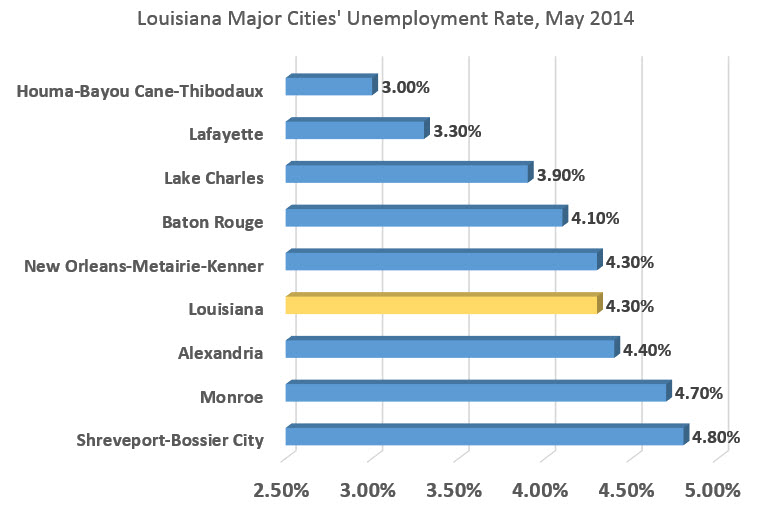

The Louisiana Commercial Real Estate Market

For $4.2 billion, you can buy all the listed commercial property in Louisiana. There are 26.9 million square feet for sale and 24.2 million for lease.

Average Time To Sell Or Lease Property

There are 8 sectors of commercial property, shown below. The time it takes to sell or lease most of these 8 types of property is longer than the gestation period of most animals, ranging from 144 to 596 days. Only Apartments and Retail property can be leased or sold faster than it takes to give birth to a human.

Days It Takes To Sell Or Lease Commercial Property, By Type

Industrial-460 days

Office-293 days

Retail-266 days

Shopping Centers-596 days

Vacant land-439 days

Farm & Ranch-not enough data points

Hospitality-Hotels-not enough data points

Multi-Family-Apartments-144 days

Average prices for space for lease and for sale are listed in the table below. The tightest sector is recognized by how close to the list price the transaction takes place. With 700 transactions, Shopping Centers rank the highest demand, having an average transaction at only 6.9% below their list price, followed by 2,493 transactions in the Office sector averaging only 10% below list, land at 15%, Industrial at 16% and in last place is the Retail market that averages a transaction 20% below list.

How Does Louisiana Compare To Mississippi

Louisiana is 4 times the Mississippi market size in property for sale, and 9 times the size in property for lease.

Lease and Sale Prices in Louisiana Compared To Mississippi

The average lease rate in Louisiana is only 10 to 20 percent higher than in Mississippi, but the average sale price in every significant sector is 30 to 100 percent higher. This is due to the more vibrant economy and demographics which drive commercial property to produce more income and therefore hold more value. For example, Industrial sale prices average $34 per square foot in Louisiana compared to $15 PSF in Mississippi, and Office property averages $80 PSF compared to $63 PSF, Retail averages $94 PSF compared to only $48 PSF, and Shopping Centers average $88 PSF compared to $43 PSF.

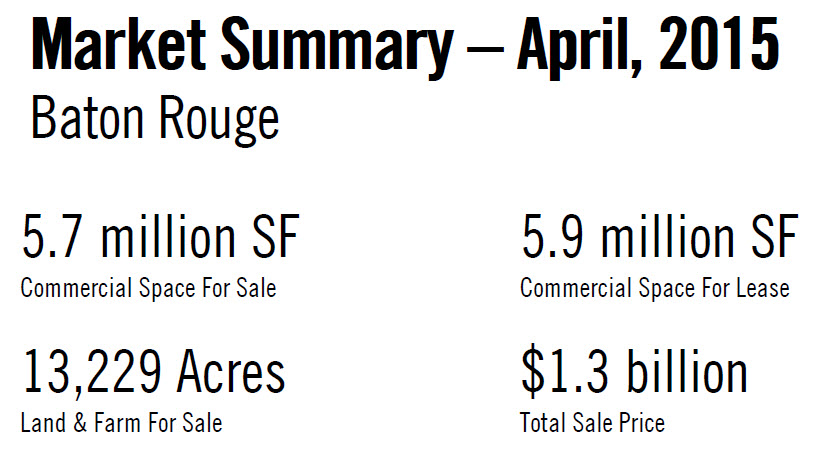

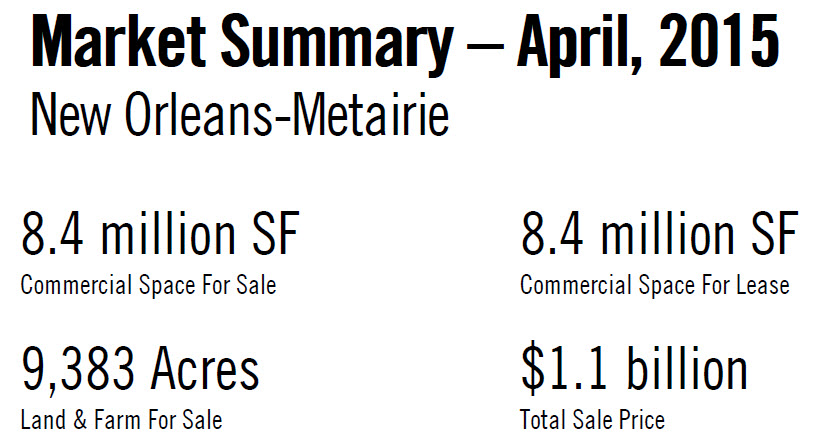

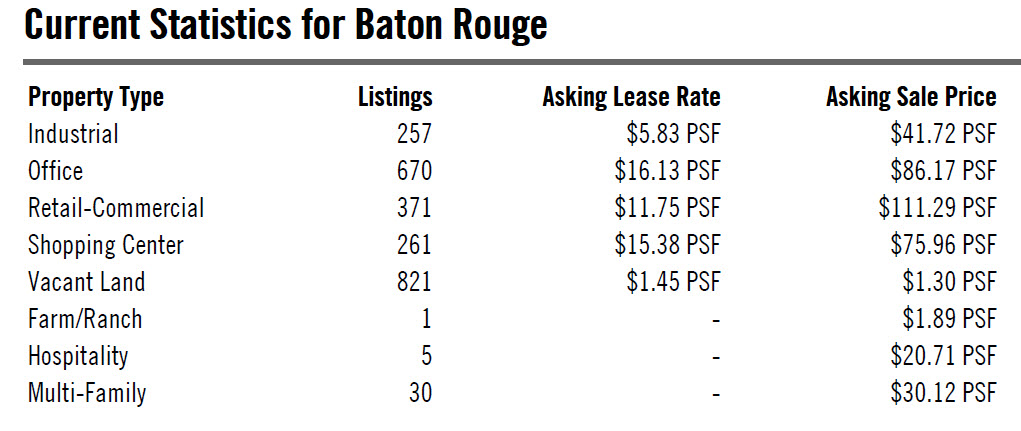

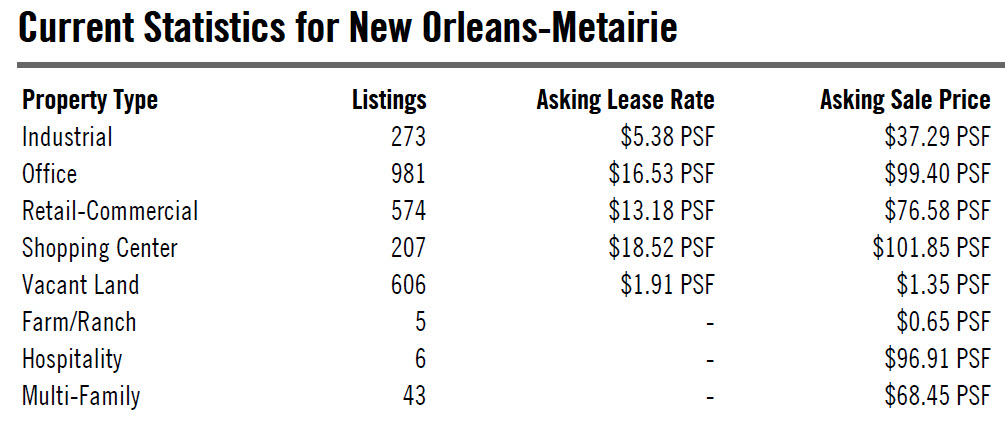

New Orleans Compared To Baton Rouge

We examine a city's MSA, which is the Metropolitan Statistical Area, designated by the Census Bureau and defined by the Office of Management and Budget as an area with a high degree of social and economic integration . New Orleans MSA is the larger market measured by square feet for sale, with 8.4 million vs. 5.7 million in Baton Rouge, but Baton Rouge is the larger market by total sale price with $1.3 billion vs. $1.1 billion.

New Orleans and Baton Rouge Have Similar Prices In Some Sectors

New Orleans has more properties on the market than Baton Rouge in every significant sector. Office and Industrial sector lease and sale prices are very close in both cities, but 371 transactions in Retail averaged a 46 percent higher price in Baton Rouge while 261 Shopping Center transactions occurred at an average 25 percent lower. Since there were hundreds of transactions, the price data cannot be skewed by outliers.

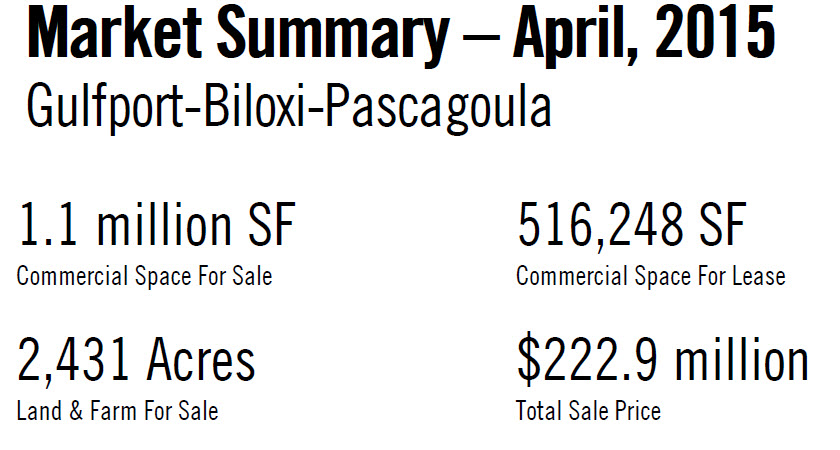

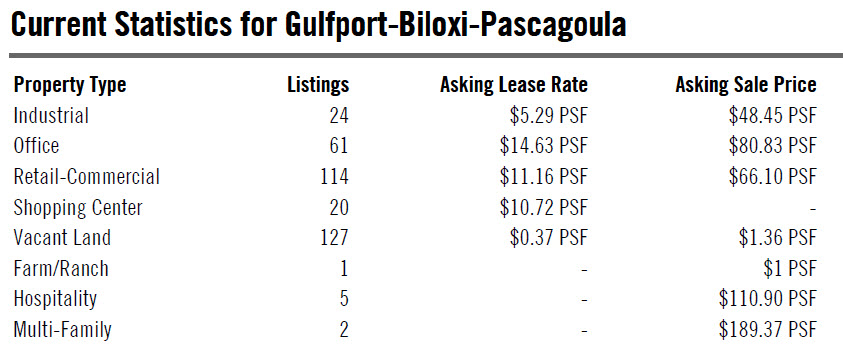

What About Gulfport-Biloxi-Pascagoula

Who would have thought Gulfport even had an MSA. The market is about 13 percent of the size of New Orleans, as measured by square footage for sale and 6 percent of the market size as measured by lease space. Prices per square foot are within 10 percent of the New Orleans market for the Industrial, Office and Retail sectors, but average 57 percent of the Shopping Center lease price. Sale prices are 20 percent higher for Industrial due to a shortage in supply, but Retail and Office sale prices average 10 to 20 percent lower.

Summary

Now that we have the average sale and lease prices of the various sectors in major markets in both Louisiana and Mississippi, where is the opportunity? If you own properties in several cities, it is called arbitrage, but the average person must look for areas and sectors where prices are simply out of sync.

You might think Shopping Centers in Baton Rouge are a steal at a sale price 26 percent less than in New Orleans, but lease rates are 26 percent less also. That's no coincidence. Office property in Baton Rouge is a bargain compared to New Orleans; even though lease rates are 3 percent less, sale prices are 14 percent less. The real bargain is Retail in New Orleans which has 12 percent higher lease rates than Baton Rouge but sale prices averaging 32 percent less.

For more information on prices on commercial real estate, click on these articles:

Office Space Prices In New Orleans

How To Value Commercial Real Estate

Sources: Census Bureau, Department of Labor & Statistics, LACDB, LoopNet

In this article we examine current market prices for every type commercial real estate in Louisiana.

Louisiana Largest Sector On The Market For An Astounding 460 Days

In Louisiana, there is 26.9 million square feet of commercial space for sale and 24.2 million square feet for lease, which can be broken down into these major categories:

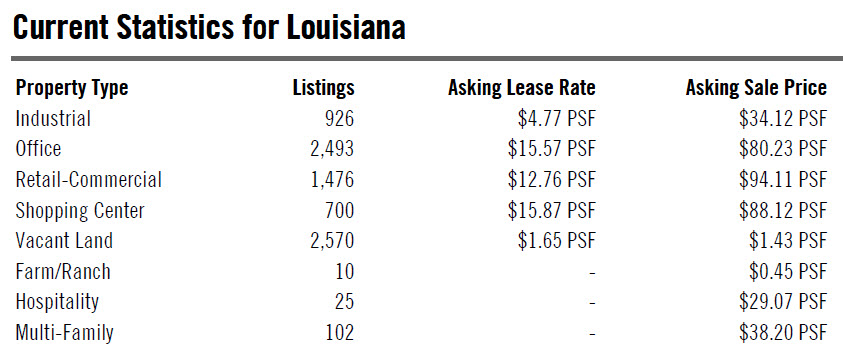

INDUSTRIAL: The Industrial sector has 926 properties totaling 21.1 million square feet and an average asking sale price of $34 per square foot and average lease rate of $4.77 per square foot. The average property is on the market an astounding 460 days.

OFFICE: The Office sector has a population of 2,493 properties with and average sale price of $80 per square foot and average lease price of $15 per square foot and on the market an average of 293 days.

RETAIL: Comprises 1,476 properties averaging $94 PSF in sale price and $12.76 PSF for lease with 266 days on the market.

SHOPPING CENTER: Classified by most as part of the Retail sector, but separated out here as 700 properties averaging a sale price of $88 PSF and lease price of $15.87 PSF with 596 days on the market.

LAND: The largest sector with 1.7 billion square feet and 2,570 properties averaging a sale price of $1.43 PSF and lease price of $1.65 PSF. Seems like its a no-brainer to buy the land at $1.43 PSF and lease it out at $1.65 PSF but it takes so long to transact a deal that the Average Days On The Market does not even show in records. It can take decades to lease or sell land.

MULTI-FAMILY: 102 properties averaging a sale price of $38 PSF , although most are sold based on Net Operating Income or Price Per Unit. Multi-Family is the category in the highest demand, as witnessed by the lowest days on the market at 144. Since the recession in 2008 and the housing market collapse, it has required a higher deposit to purchase a home, causing an increase in renting, resulting in a higher demand for apartments, which leads to higher occupancy rates, which results in large institutions changing their asset allocation away from shopping center investment to apartments, which causes a shift in demand leading to higher prices for apartments and lower Capitalization Rates. Whoo! Yes, it is a Domino Effect, and the trend will continue.

TABLE OF PRICES AND DATA FOR COMMERCIAL PROPERTY SECTORS IN LOUISIANA

Industrial Market In Detail

Let's carve out one of the sectors comprising all Louisiana commercial real estate and break it down. The Industrial market is comprised of 926 properties with 570 for lease and 356 for sale. There is 10 million square feet for lease and about the same for sale. On average the last two years, 29 properties have been leased at an average of $3.68 per square foot and 10 properties have sold at an average of $46 per square foot. This is an average of all the industrial properties in Louisiana, and certain areas may be stronger or weaker.

INDUSTRIAL SECTOR DATA

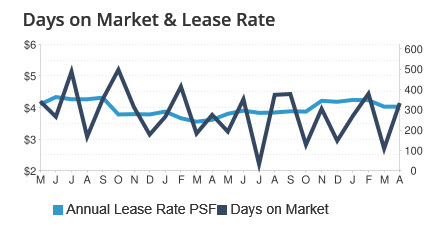

Industrial Market Price Volatility

Just like the analyst on Bloomberg and CNN who prognosticate with 100% accuracy that the markets will be volatile and fluctuate, providing no more insight than a zoo animal throwing a dart, the chart below shows that over the last 2 years the price of leasing Industrial space on average in Louisiana has gone up and down but not gone anywhere at about $4 per square foot. The average days on the market ended up where they began at around 300.

CHART OF DAYS ON THE MARKET AND LEASE RATE FOR INDUSTRIAL PROPERTY IN LOUISIANA

Tune in next week for a detailed look at prices of other sectors of commercial real estate in Louisiana.

For more information on prices on commercial real estate, click on these articles:

Office Space Prices In New Orleans

5 Things You Need To Know About Pricing Multi-Family

A vacant hotel property that is among the largest pieces of available real estate along Tulane Avenue recently changed hands after more than three years on the market.

The Americas Best Value Inn, 2820 Tulane Ave., sold on March 25 for $1.06 million, according to Orleans Parish conveyance records. The 16,000-square-foot hotel, which is spread across three separate buildings, sits on a more than 30,000-square-foot tract of land near the Orleans Parish Criminal District Courthouse.

Conveyance documents show the property, which had also gone by the name Patio Motel, sold to an entity known as 2820 Tulane LLC. Records from the Secretary of State list New Orleans residents Bahram Khoobehi and Hossain and Mahmood Mogharehabed as members. The new owners could not be reached for comment.

Commercial broker Robert Hand, president of Louisiana Commercial Realty, said the property has been vacant since 2011 when a fire in one of the rooms caused severe damage to the roof and most of the second and third floors. The property was put on the market in “as-is” condition and listed at land value.

According to Hand, buyers came forward twice in 2011, but neither could arrange financing. The property sold in 2012 for $650,000 to a local hotel owner who intended to restore it as a hotel, but the project became too expensive. Prior to this most recent deal, Hand said a verbal offer came in 2014 from a local construction company, but a deal couldn’t be reached.

“It was rather surprising that it took this long to close a promising deal,” Hand said. “Tulane Avenue is among the most anticipated areas in New Orleans for new developments and we had a number of written offers, but none materialized.”

“Negotiations with this most recent buyer began in February,” Hand said. “The plan is to include retail on the ground floor, which is required by zoning, and office space on the upper levels.”

The hotel’s seller is listed as WHCTC II, LLC, which lists New Orleans resident Wen Chuan Chen as a member.

According to assessor’s records, Khoobehi owns several residential properties along Broadway Street uptown.

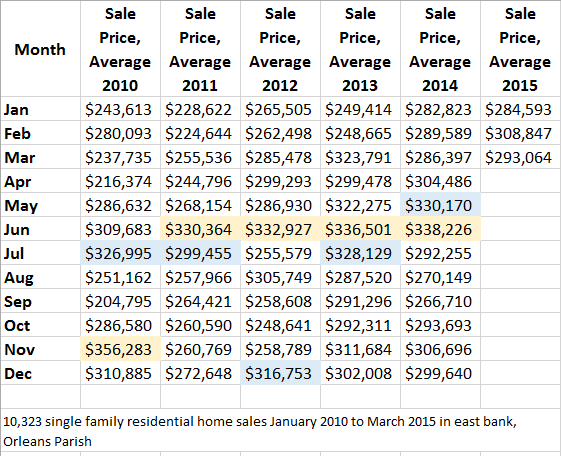

The common belief that homes prices rise during the summer months because everyone wants to be settled in before school starts is true. The facts show us that the highest prices concentrate around the month of June.

Examining The Trend of 10,323 Homes Sold Over The Last 5 Years

Using the Multi List Service from the Realtor database, home sale prices can be sorted by month, as shown in the table below in a sample of 10,326 single family detached home sales. The highest price month is highlighted yellow, and the second highest price month is highlighted blue. The results show in all but one month since 2010, the highest average price for homes sold occurred in June, and in the second highest price in 3 of the last 5 years occurred in the month of July.

Average Sale Price By Month For Single Family Homes The Last 6 Months

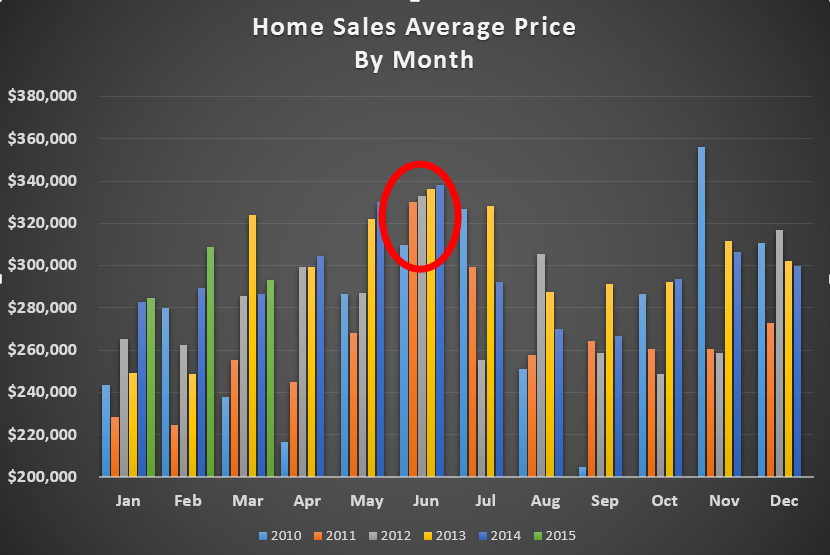

Chart Home Sales By Month

The concentration of homes sold in June can easily be seen in the chart below because almost every year it is the month where prices reach their highest level.

Source: GSREIN MLS database, Stats customized by average sale price and exported.

Note: Average sale prices were used. Results differ if median sale prices are used.

For prices on commercial real estate, click here for charts of current list and lease prices on Industrial, Retail, Office & Retail sectors.

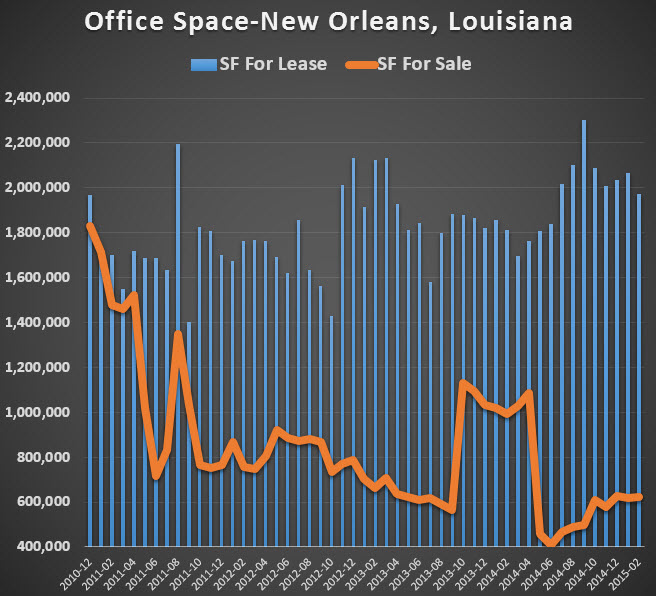

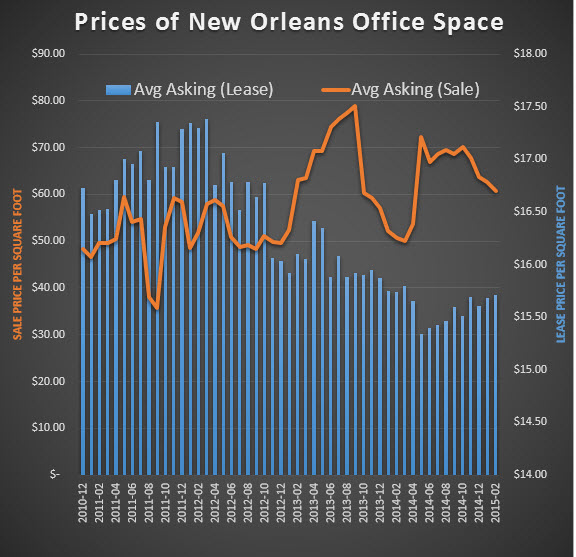

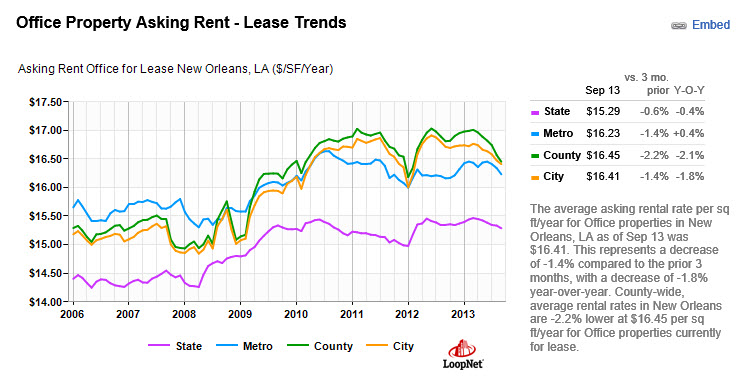

Over the last 4 years, available office space for sale in the New Orleans area has plummeted to one third of its previous supply, due to a lack of new office space construction. The result is a strengthening of sale prices in the office market. This article examines the supply and demand of office space and the trend for the future.

Just 4 years ago, there was just as much office space for sale as there was for lease: around 1.9 million square feet. Each month, on average, there have been approximately 322 properties for lease at an average of $16.30 per square foot and 34 for sale at an average of $58 per square foot. Sale prices averaged 8 percent below the list price and the average property was on the market 354 days.

Today; however, tells a different story. Even though the supply of office space for lease has increased slightly from 1.9 million square feet, the amount of office space for sale has dropped by two-thirds to only 622,000 square feet.

Chart of New Orleans Office Space For Sale and For Lease Since 2010

Economics 101: Supply and Demand

Basic economic theory says, given all other variables unchanged, a decrease in supply leads to an increase in price. That theory can be seen in practice in the chart below which compares the prices over the last 4 years of office property for lease and for sale. The result is that with the strength in supply in office space for lease, prices declined approximately 8%, while prices of office property for sale have increased 20%.

Chart of New Orleans Office Space Prices Since 2010

Summary

Equilibrium in prices is not reached until the supply approximates demand, so the future for office space is that lease prices will continue to fall since the amount of office space for lease appears to increase slightly. Sale prices will continue to rise, causing a new wave of sellers of office properties to enter the market and take advantage of higher prices. This will eventually stabilize the prices of office space for sale.

Sources: Louisiana Commercial Database, LoopNet

For help leasing, buying or selling office space, contact Louisiana Commercial Realty at 504-289-8172 or by email at roberthand@cox.net.

For additional articles on office space supply and demand, click:

Fire Damaged America's Best Hotel Going Back Into Commerce As Office/Retail Center

NEW ORLEANS, Louisiana. March 26, 2015 – Tulane Avenue is the most anticipated area in New Orleans for new developments, and the largest tract of land in the area will finally be put back into commerce after 4 years of work by a local commercial real estate broker. Louisiana Commercial Realty president Robert Hand says, "Our firm has been involved with almost every major development in the Tulane Avenue area, and we are proud to announce another vacant property will be put back into commerce. The fire-damaged America's Best Hotel at 2820 Tulane Avenue has been sold to a local businessman who hopes to transform the property into a new office and retail development."

The 4 year struggle to get the 32,579 square foot of land developed started in April 2011, after the property was severely damaged by fire caused by one of the hotel's residents who was cooking on a hot plate in a room on the third floor. The fire destroyed the roof and most of the third and second floor. The property went on the market to be sold in AS-IS condition, and many hopeful developers thought it could be revived as a moderately priced hotel. In June 2011, a developer agreed to purchase the property, but it turned out they did not have the proper financing and the property went back on the market. In October 2011, there were negotiations from a nearby property owner to purchase the property, but things fell apart when the buyer again could not get financing. Finally in January 2012, the property was purchased for $650,000 by a local hotel owner who believed Tulane Avenue was a good location and envisioned putting the property back into commerce as a hotel. The new owner incurred over $100,000 in fees from architects and attorneys just so he could present the development to the City Planning Department for approval, but after nearly three years he was still unsuccessful. The owner decided a hotel would require more effort and expense than he expected, and decided to entertain offers to purchase the property. A verbal offer from a local construction company in December 2014, for $1,000,000 could never be finalized in writing, but in February 2015, negotiations started with a local businessman who owned nearby retail property and wanted to do more in the area. Finally in March 2015, the businessman purchased the property for $1,060,000 under the name 2820 Tulane, LLC.

Hand says, "We are reminded when properties like this are put back into commerce, that real estate is often the vehicle by which the average person can achieve their lifelong dream. The seller of this property moved to the area 25 years ago, arriving in the middle of a recession with a dream to operate his own hotel. He purchased a small hotel in Houma and built the business up successfully, then sold it and used his family's life savings to buy this property. The buyer of this property is a trained physicist from Europe, whose most likely job was work in the military but sought a better life in the US. He now does work with the National Institute of Health and saves his money so he can buy real estate. It is the grit and determination of an average person, looking to make a better life for their family who in the end helps revitalize New Orleans and transform its landscape. We are proud to have been a part of helping people realize their dream."

About Louisiana Commercial Realty LLC

Louisiana Commercial Realty LLC, based in New Orleans, Louisiana, is known for marketing high value, complicated commercial properties. President Robert Hand is the only commercial real estate broker in Louisiana with an MBA and the CCIM and SIOR designations.

Valuing New Orleans commercial real estate accurately can be difficult at times, but using basic financial principles can help you calculate the market price with a higher level of confidence. Just remember that the price of any object is the equilibrium of supply and demand, but commercial real estate supply and demand can depend on emotional as well as logical factors. The challenge is to avoid these emotional traps and use rational analysis to price your property. Here are the three most common pricing traps that sellers fall into that are imperative to avoid.

1. I'm Just Going To Hold It Until I Get My Price

While the price the seller paid has nothing to do with the value of the property nor what the seller thinks it might be worth, many sellers use their purchase price as the bottom line they will take when negotiating a price with a buyer. It is called "benchmarking" and it is an easy mistake because nobody likes to lose money on an investment. In more cases than not however, a seller is better off taking the highest price they can get and then reinvesting their money elsewhere to recoup their losses since trying to get an above market price might happen, but it might take you ten years to do so. You can prove it with math using the formula for present value: where i is the interest rate you can earn elsewhere and n is the time. Therefore if you wait 10 years to finally get a buyer at the $1,000,000 price you paid for property, you would have the same amount of money as if you sold the property today for $613,913 and put that money to work at 5% annually. This is a real disaster when holding land that does not appreciate in value since you still have to pay taxes and keep the grass cut.

2. The Appraisal Was Much Higher

Appraisals are restricted to using three pricing methods:

a. Income Approach-value based on the net operating income the property generates.

b. Cost Approach-based on what the cost would be today to build your property.

c. Market Approach-based on what other properties in the area have already sold for, adjusted for inequalities.

The appraisal is always based on assumptions which, using today's methods, don't allow an accurate price. For example, the income approach assumes the tenant does not default on the income, that taxes and expenses do not increase and that current expenses stated by the seller are accurate. Rarely does an appraisal calculate net operating income including maintenance sinking funds, even though air conditioners and roofs have a finite life and need to be replaced. And these are very large expenditures which can easily eliminate a years' rental income. The cost approach assumes you can build a new structure for a certain price, usually a per square foot estimate, when any accurate pricing would require a firm bid from a contractor based on specific drawings for the new project. The market approach assumes properties already sold would still have those buyers interested in your property and would have the same demand. Just because one person paid one million for the property down the road to build an apartment doesn't mean a different person who wants to build a po-boy shop would pay the same amount, or that the apartment buyer would have any money left to purchase your property.

3. It's What I Paid For It

Buyers don't care what you paid for it, just like the television show Pawn Stars, when someone walks in to sell an old item they bought long ago. The Pawn Store is only interested in what they can sell it for. Your cost is called a "sunk cost" in that you spent that money regardless of whether you hold or sell the property.

The Best Method For Valuing Commercial Real Estate

Pricing commercial property accurately can depend on the use a buyer might have, so it pays to ask a lot of questions. Here is a real world example. The subject property is a 10,464 square foot vacant building with three separate spaces: a 4,930sf restaurant, a 3,600sf retail space and a 1,934sf retail space.

This property could be sold to an investor who might rent the space for $16/sf, for a gross income of $167,424, if taxes and insurance costs are passed along to the tenants in a triple net lease.

Pricing Commercial Real Estate Using Net Operating Income

The price of any investment property, stock or bond, is the present value of future cash flows, adjusted for risk and opportunity costs. The income on commercial real estate is measured by Net Operating Income, which is the income stream generated by the operation of the property, independent of external factors such as financing and income taxes. Gross income includes both rental income and other income such as parking fees, laundry and vending receipts, and any other income. Operating expenses are costs incurred during the operation and maintenance of a property, including repairs and maintenance, as well as insurance, management fees, utilities, supplies, property taxes and others, but excluding principal and interest, capital expenditures, depreciation, and income taxes. For a 10,000 square foot property 100% leased at $10 per square foot producing income of $100,000 annually with expenses of $25,000 annually, the Net Operating Income would be $75,000. If a buyer needs a 9% Cap Rate, the price of the property would be $833,000. If the buyer felt there was more risk than normal and required a 12% cap, the price would be $625,000. If the property were a high quality AAA rated large company such as CVS or Walgreens, the same property with the same income would trade at a 5.5% to 6% Cap Rate since 30 year Treasury Bonds trade at 2.97%, resulting in a price of $1,363,000.

If the investor had to lease the space, the risk of leasing the space would be factored in and there would be an expectation at least a 15% cap rate to assume that risk which would value the property at $500,000, using the formula below.

The seller could be able to command a higher price simply by finding a user of one of the spaces who would buy the property and lease the two remaining spaces. Simply by putting yourself in the buyer's position, you can determine the maximum price a buyer would pay. Here is how it works. A user, for example, of the restaurant is comparing the cash flows of buying versus leasing space. Using the "Law of Substitution", the restaurant owner would compare the alternative of leasing versus buying this property, and the market lease rate is $16.sf, plus $3/sf triple net costs, for an annual lease cost on 4,930sf of $93,670. The buyer could justify purchasing the building if the costs were less than the lease cost. Here is the cost to the potential buyer at various purchase prices. If the potential buyer can lease elsewhere for $93,670 annually, he/she would not be willing to pay a price for the property which would result in a cost of more than that, after taking into account the rental income. The above spreadsheet can be graphed to produce a maximum price which is the intersection of the line of rental cost and the line of net purchase cost.

The maximum price for this property a buyer could justify would be $1,320,000 which would result in a cost of $93,670 annually which is the same as the alternative property lease cost. There are some considerations, such a tax savings from depreciation but that is offset by the tax when the property is sold since the recapture rate is close to the ordinary income rate. There is also the benefit of principal paydown on the mortgage note which is offset by the owner's space cost of taxes and insurance and the maintenance and roof expenses. In summary, the best method to value a property is to put yourself in the most qualified buyer's position and determine what the alternative costs are for the buyer, then price your property using basic financial principals..

Definitions:

"benchmarking"- valuing a property not on the current market value or analysis but on some price you have in your mind that it is worth, based on what you paid for the property or a price someone, somewhere, long ago offered you that you turned down.

"net operating income" - gross income less operating expenses (maintenance, insurance, property taxes, management expenses, utilities) but before income taxes, interest and depreciation.

"sunk cost" - past costs that have already occurred and cannot be recaptured.

"cap rate" - capitalization rate. The rate of return used to value an income stream which can be composed of current and future income or expected capital gain.

copyright 2012 www.louisianacommercialrealty.com.

Last Wednesday, President Obama was the lead story on many television stations, proposing a new plan to eliminate "conflicts of interest" that investment advisors have with their clients.

This begs the question: Can government regulate ethical behavior? This article explores how ethical behavior is incentivized, either on purpose or by neglect, even down to how the real estate industry regulates emails and signs posted that property is for sale.

Shades of Gray: AARP, Secretary of Labor & Vanguard Mutual Funds

In speaking to AARP last week, President Obama said, "Financial advisors...shouldn't be able to take advantage of their clients." What you didn't hear on the news was Secretary of Labor, Tom Perez, discussing "the corrosive power of fine print, hidden fees and conflicted advice" and that the president also promoted Massachusetts Senator Elizabeth Warren, who has been popular since her 2012 election with a platform stating that the financial industry takes advantage of people.

Obama's plan to regulate ethics is to be presented by Labor Secretary Perez, who on a conference call with reporters, was joined by John Bogle, founder of the largest mutual fund family, Vanguard. What you also did not hear is that Vanguard's business model doesn't offer financial advice and Vanguard directly competes with firms that do offer one-on-one education on financial issues. For the average person who wants personal financial education, the best source is often a highly trained, licensed financial advisor. There is always a fascinating story behind the story, and the backstory here is that the new claim for additional government regulation will not work.

The Untold Story: Morris Bart Could Never Be A Financial Advisor

The untold story is that the financial industry is already one of the most heavily regulated industries. Financial advisors only get into the industry after an intensive hiring process where only the most qualified are accepted. Advisors must pass a test to become licensed by FINRA (Financial Industry Regulatory Authority), the not-for-profit organization authorized by Congress to supervise the 637,000 brokers in the US. In addition, each office where the financial advisors are employed has an operations staff that reviews account paperwork and transactions, and most offices have replaced their sales manager with a compliance officer. The accounts of each financial advisor are reviewed regularly to insure compliance with a client's investment objectives, and accounts that are too active receive letters and phone calls from the office's compliance office. Financial advisors cannot send emails or letters to clients without approval and can not use excessive language in any communications.

Morris Bart could never be a financial advisor because he could not imply that all you needed to do was call him to get your money. The reality is that financial advisors are trained to provide a high level of service to clients which encourages referrals which helps them grow their business. Like buying a car or a house, consumers have the responsibility to become educated about their purchases to make the right decision, and in the investment arena the best education on investments can come from your local financial advisor.

The free market is more efficient than government at weeding out the poor performers, if we just let it work. Educated consumers seek out the best service providers, and poor service providers go out of business. That's why businesses are always evolving, trying to provide the highest level of service.

Government Regulates Realtors But Most Of The Training Is Done By NOMAR

The real estate industry is also highly regulated, but not like you thought. Licenses are issued by each state's Real Estate Commission. There is HUD and FHA and FNMA and GNMA but there is no federal government real estate agency regulating real estate agents. Louisiana created its Real Estate Commission in 1920 but it wasn't until 1972 that agents had to pass a test to obtain their license. While the Louisiana Real Estate Commission's main function is to issue the licenses, they are also charged with protecting the public's interest.

The LREC is the only resort for consumer/agent disputes and while every purchase and sale agreement references the parties will abide by the LREC rules regarding deposits, the fact is that the LREC tells parties in deposit disputes to take their claim to court. The only other real estate body is a trade organization, NOMAR (New Orleans Metropolitan Association of Realtors) which was chartered in 1915 by the National Association of Realtors that applies ethical standards only to its paid members.

Rules Lay The Groundwork For Ethical behavior And Tell Us How To Send Emails

The Louisiana Real Estate Commission has adopted Rules and Regulations pursuant to the authority granted in the Louisiana Revised Statutes, Title 37, Section 1435. The Rules and Regulations serve as an extension of the Real Estate License Law and assist the Commission in enforcement. The rules regarding the conduct of agents cover a wide range of topics, including advertising, mold, franchise operations, presentation of offers, and broker cooperation, but nothing about procuring cause, which is widely misunderstood.

The rules lay the groundwork for ethical behavior and agents are required to complete continuing education. The rules are sometimes very detailed, even going as far as explaining how to send emails. In 2012, 14 years after Google was founded but only 12 months after Snapchat, a special section of rules was finally adopted on how to properly use the Internet:

Internet advertising must include the broker's name, city & state, and license jurisdiction.

Emails must include must include the broker's name, city & state, and license jurisdiction.

Advertising by signs must include the following:

Broker name

Phone number

Finally Some Information We Can Use

Nominate a friend's best or worst email signature and get $10 donated in your name to your favorite charity. Send your nomination to roberthand@cox.net.

Interested in graduate school? For a free lesson on configuring email signatures to add pictures and hyperlinks to websites, or icons that link to facebook, twitter or linkedin, send us an email.

Every year, on average, the Corps of Engineers allows 20,000 acres of wetlands to be impacted by developments but at the same time they require 56,000 acres of wetlands to be restored. This article explores how developers protect our wetlands under a program administered by the US Army Corps of Engineers by purchasing mitigation bank credits which offset the impact a development might have on wetlands.

Since New Orleans is technically under sea level, you would expect many real estate developers to be eventually confronted with wetlands on their property, which the Environmental Protection Agency defines as “an area that is regularly saturated by surface water or groundwater and is characterized by a prevalence of vegetation that is adapted for life in saturated soil conditions”. Although these areas make up a very small percentage of the total land found in the United States, Southern Louisiana contains 40 - 45% of the wetlands found in the lower 48 states. This is because Louisiana is the drainage gateway to the Gulf of Mexico for the Lower Mississippi Regional Watershed which drains more than 24 million acres in seven states from southern Illinois to the Gulf of Mexico.

Mitigation Banking

Compensatory mitigation for unavoidable wetland impacts may be accomplished through three distinct mechanisms:

• Permittee-Responsible Mitigation: Restoration, establishment, enhancement or preservation of wetlands undertaken by a permittee in order to compensate for wetland impacts resulting from a specific project. The permittee performs the mitigation after the permit is issued and is ultimately responsible for implementation and success of the mitigation. Permittee-responsible mitigation may occur at the site of the permitted impacts or at an off-site location within the same watershed.

• Mitigation Banking: A wetlands mitigation bank is a wetland area that has been restored, established, enhanced or preserved, which is then set aside to compensate for future conversions of wetlands for development activities. Permittees, upon approval of regulatory agencies, can purchase credits from a mitigation bank to meet their requirements for compensatory mitigation. The value of these “credits” is determined by quantifying the wetland functions or acres restored or created. The bank sponsor is ultimately responsible for the success of the project. Mitigation banking is performed "off-site," meaning it is at a location not on or immediately adjacent to the site of impacts, but within the same watershed. Federal regulations establish a flexible preference for using credits from a mitigation bank over the other compensation mechanisms.

• In-Lieu Fee Mitigation: Mitigation that occurs when a permittee provides funds to an in-lieu-fee sponsor (a public agency or non-profit organization). Usually, the sponsor collects funds from multiple permittees in order to pool the financial resources necessary to build and maintain the mitigation site. The in-lieu fee sponsor is responsible for the success of the mitigation. Like banking, in-lieu fee mitigation is also "off-site," but unlike mitigation banking, it typically occurs after the permitted impacts.

Here’s how mitigation works in real estate development. Let’s say a private developer is building a subdivision on 900 acres of land, of which 300 acres has been declared wetlands by the U.S. Department of Army under the Corps of Engineers. Once federal and state regulatory agencies have agreed that the developer cannot avoid or even minimize the effect on those acres, the developer must compensate – hence, the word mitigation – for the wetlands’ loss by purchasing credits in a mitigation bank.

The mitigation bank is the area that has been restored-not a bank as we know it- and has four distinct components:

1. The bank site: the physical acreage restored, established, enhanced, or preserved;

2. The bank instrument: the formal agreement between the bank owners and regulators establishing liability, performance standards, management and monitoring requirements, and the terms of bank credit approval;

3. The Interagency Review Team (IRT): the interagency team that provides regulatory review, approval, and oversight of the bank; and

4. The service area: the geographic area in which permitted impacts can be compensated for at a given bank.

Before a bank can be permitted, and approved for wetland credit sales, federal and state government regulatory agencies form a Mitigation Banking Review Team (MBRT) that must approve plans for building the bank, from the hydrological and planting design to maintenance and monitoring arrangements. The MBRT also approves the number of mitigation credits that may be earned by the banker.

A developer can buy credits only if they have applied to the federal and/or state agency responsible for wetland permitting, and have provided adequate justification of a need to impact wetlands on their development. Mitigation regulations recommend that the impact and compensation be located in the same watershed and that the impact and mitigation be the same habitat, of similar ecological value or ecologically preferable.

In-Lieu Fee Mitigation

A permit applicant may make a payment to an in-lieu fee program that will conduct wetland, stream or other aquatic resource restoration activities. In-lieu fee programs, as shown in Chart One, are generally administered by government agencies or non-profit organizations that have established an agreement with the regulatory agencies to use in-lieu fee payments collected from permit applicants.

Usually a non-profit organization acts as an intermediary to restore, enhance, create and preserve wetlands and assumes responsibility for their long-term maintenance, earning mitigation credits for their efforts. Non-profits can then sell these mitigation credits to developers who have a permit who must compensate for having impacted wetlands. The sale of wetland credits legally transfers the liability for wetland mitigation from the permittee to the wetland banker.

New Rules

In 2008, the U.S. Army Corps of Engineers adopted new rules that dramatically changed its approach to mitigation under Section 404 of the Clean Water Act, which regulates fill in wetlands and other waters of the United States. The new rules adopt a mitigation hierarchy that moves away from the prior preference for onsite mitigation in favor of mitigation banks and watershed-based mitigation programs. If you wish to obtain a permit to impact wetlands, you must first minimize impacts, and then compensate for unavoidable impacts. The basis for the new rule is that despite progress over the last two decades, there are still gaps in the science of restoration ecology.

The new rule state a permittee must have mitigation plans which include the following:

*objectives

*a mitigation work plan

*site selection criteria

*a maintenance plan

*baseline information (for impact sites)

*credit determination methodology

* performance standards

*a long-term management plan

*site conservation easements

*monitoring requirements

*financial assurances

Source: 1 Federal Register, Guidance for Establishment, Use and Operation of Mitigation Banks, November 28, 1995

Text and images are copyrighted. Contact author for permission.

Louisiana Commercial Realty announced today they were hired to market the 16,000 square foot two-story office building at 739 South Clark Street, near Tulane Avenue and Jefferson Davis Parkway in New Orleans. The building was completely renovated by Ellis Construction and features a unique design including open area for collaborative work flow, cypress flooring, ample controlled parking and large windows allowing light to flow throughout the space.

Tulane Avenue in recent years has experienced a rebirth with more new multi-million dollar developments than any other area of New Orleans, including several large apartment buildings, retail centers, retirement facilities, and the largest hospital development in the United States: the Veterans Administration and the LSU hospitals.

739 south clark

Robert Hand, president of Louisiana Commercial Realty said, ” This is a very special renovation; there is no other building like this in New Orleans. Ellis Construction put real heart into this spectacular renovation, and we think the space is perfect for a growing architectural firm, software design firm, or digital media company. The building is for sale at $2,050,000 and the 2nd floor is also for lease."

Tulane Avenue has witnessed over $1 billion dollars in developments since Hurricane Katrina. Louisiana Commercial Realty has been instrumental in almost all of the Tulane Avenue developments, representing the Domain Company in their development of the 228 unit Crescent Club Apartments, the 72 unit Meridian Apartments, the 183 unit Preserve Apartments, the 18,000 square foot Shops at Crescent Club Retail Center and representing Provident Realty in their development of the 250 unit Marquis Apartments.

More information is available by downloading the 739 South Clark marketing presentation.

Technology has taken a giant leap forward in the last few years by expanding the traditional tool of demographic research into an analysis of lifestyles and consumer spending behavior. The old-school strategy was to look at population count, income, and age to determine a good location for a business. But new-school tools such as leakage factor, retail gap, and Tapestry lifestyle analyses take decision making to a higher level and reduce the risk of failure.

This article examines how these new technologies can help commercial real estate professionals make better real estate decisions. We examine an actual 10 acre tract in New Orleans, utilizing the latest technology of the Certified Commercial Investment Member database to generate sophisticated site analysis information on the best use by examining the lifestyle of the residents in the area — and how they spend their money — to determine what retail businesses were needed.

Drive Times

Typically the target-area population analysis looks at demographics within a radius of 3 miles, 5 miles, and 10 miles. However, a better approach is drive-time analysis, which provides more-useful information when there are natural boundaries to an area: For example, north of New Orleans is Lake Pontchartrain and east of New Orleans is a wetlands area and wildlife preserve.

Within the drive times, knowing the population density, per capita and household income, home ownership, and age brackets helps to determine which retailers might thrive: Brooks Brothers or Dollar General? For multifamily, we can examine how many people rent and are in their 20s, the prime apartment renting age. For example, in the 5- and 10-minute drive times from the target 10-acre site, future growth trends show increases in household formation and income. (See Table 1: Demographic Summary.)

Traffic counts also provide useful data, particularly for retail site analysis. The 2008 traffic study by the Louisiana Department of Transportation showed Interstate 10 traffic in New Orleans East at 34,000 cars per day, and the 2010 estimate from Datametrix (www.stdb.com) is 30,000 cars per day.

Demographics – New School

Market Potential. The Market Potential Index measures the relative likelihood of households in the specified trade area exhibiting certain purchasing patterns compared to the United States as a whole. An MPI of 100 represents the U.S. average; a higher number indicates a higher propensity to spend in that category, compared to the national average. (See Table 2: Market Potential Index.)

Two conclusions can be drawn from consumer spending data. First, the MPI exceeds 100 on seafood and chicken/turkey in both the 5- and 10-minute drive time areas, revealing a higher than average propensity to spend on these items. Second, the population is high enough to support at least four supermarkets, using the market assumption that a 50,000-square-foot supermarket needs approximately 8,000 residents.

We can zero in on how much money residents spend annually in specific categories. For example, within a 5-minute drive time of the site, the total amount of money spent on food at home exceeds $39 million and within a 10-minute drive time exceeds $111 million. We also can drill down to determine what types of items a supermarket could sell to have a competitive advantage. For example, within a 10-minute drive time, $38 million was spent on “snacks and other food at home.” (See Table 3: Specific Spending.)

Retail Opportunity. Using industries categorized by North American Industry Classification System, or NAICS, codes, we can pinpoint where demand exceeds supply and shows a need for a business to fill a void. We determine supply by estimating sales to consumers by establishments, while excluding sales to businesses. We forecast demand, or retail potential, by estimating the expected amount spent by consumers at retail establishments.

The gap between demand and supply is called the leakage factor, which presents a snapshot of retail opportunity. This is a measure of the relationship between supply and demand that ranges from +100 (total leakage) to -100 (total surplus). A positive value represents “leakage” of retail opportunity outside the trade area. A negative value represents a surplus of retail sales, a market where customers are drawn in from outside the trade area.

NAICS represents one of the most profound changes for statistical programs focusing on emerging economic activities. The system groups establishments into industries based on their primary activity. NAICS moves down in detail from sector to subsector to group then to industry. This is an improvement over the previous method, the 1987 Standard Industrial Classification, or SIC, system.

The highest leakage factor shows a need for miscellaneous retailers such as florists, office supply, and pet shops; furniture; sporting goods; clothing; and food stores. (See Table 4: Leakage/Surplus by Subsector.)

The leakage factor shows what businesses are needed, by the percent that demand exceeds supply and the dollar amount of the unfulfilled demand, which can forecast sales for a business coming into the area. Retail Gap Analysis represents the difference between retail potential and retail sales: Industry groups with the largest retail gap in the target area are grocery and food and beverage. (See Table 5.)

Zip Code. Retail Marketplace Reports are available by theme, such as grocery store sales, and can drill down to county, city, zip, census tract, and block group, the smallest unit of measurement of census data. Themes can get very specific, even down to a map of the population that used aluminum foil in the past six months. We searched for grocery store sales by zip codes south and west of the target area that are above $28 million; since there is only one Winn-Dixie store in that area, we know the market will bear additional stores. We can use information on expected sales to right-size building square footage and land area.

Tapestry Reports. Tapestry identifies neighborhood segments and describes the socioeconomic quality of the immediate neighborhood. The index is a comparison of the percent of households or population in the area, by Tapestry segment, to the percent of U.S. households or population by segment. An index of 100 is the U.S. average.

The top two Tapestry segments in the target area are Family Foundations and Metro City Edge. These segments include lifestyle traits such as playing basketball and watching courtroom TV, so we can tailor our advertising around that media rather than newsprint. (See Table 6: Top 10 Tapestry Segments.)

Our use of technology has delivered important information for determining the best businesses for the target 10-acre site while reducing risk of business failure. We have progressed from simply knowing the population count, age, and income to knowing detailed information about who lives in the target area, how they spend their money, and what businesses are missing that could satisfy that demand. We have been able to conclude the target area has the highest unfulfilled demand for furniture, sporting goods, clothing, and food stores, and we have been able to forecast the total sales of a future grocery store and can plan our capital expenses such as store size accordingly. We know what makes the nearby residents unique and where they spend more of their money compared to the average consumer, so we also can lower our inventory costs by stocking the goods with the highest demand. We also can reduce our advertising costs by targeting the media that our customers will use.

These new-school tools are available to everyone facing a real estate decision, not just the Walmarts of the world.

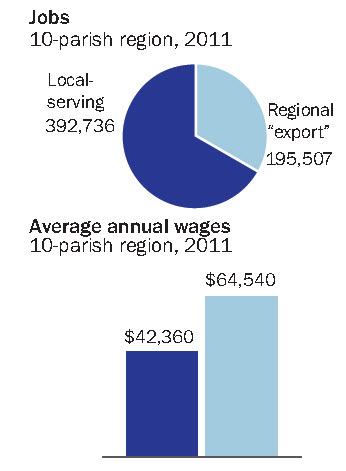

Two out of three ain't bad. The percent of new business start-ups since Katrina has exploded, far outpacing the national average, but the population has continued its shift out of Orleans Parish and government is still the highest job giver. This article examines where the jobs are in the 10 parish region, how we are more productive than the US as a whole, how jobs are leaving Orleans Parish and where they are going.

10 Parish Region

The New Orleans MSA ( Metropolitan Statistical Area) refers to the 7 parish area surrounding New Orleans. A MSA is an area exceeding 50,000 population with a high degree of similarity in social and economic traits. The 10 parish region includes St. James, Tangipahoa & Washington parishes since their economic traits are interwoven.

Jobs By Sector

job chart

Since 2010, four sectors have lost jobs: manufacturing, oil, government and administration services, but government is still the major employer in the 10 parish region around New Orleans with 17% of the nonfarm jobs, followed by wholesale and retail trade at 15% and hospitality at 13%.

Job Distribution

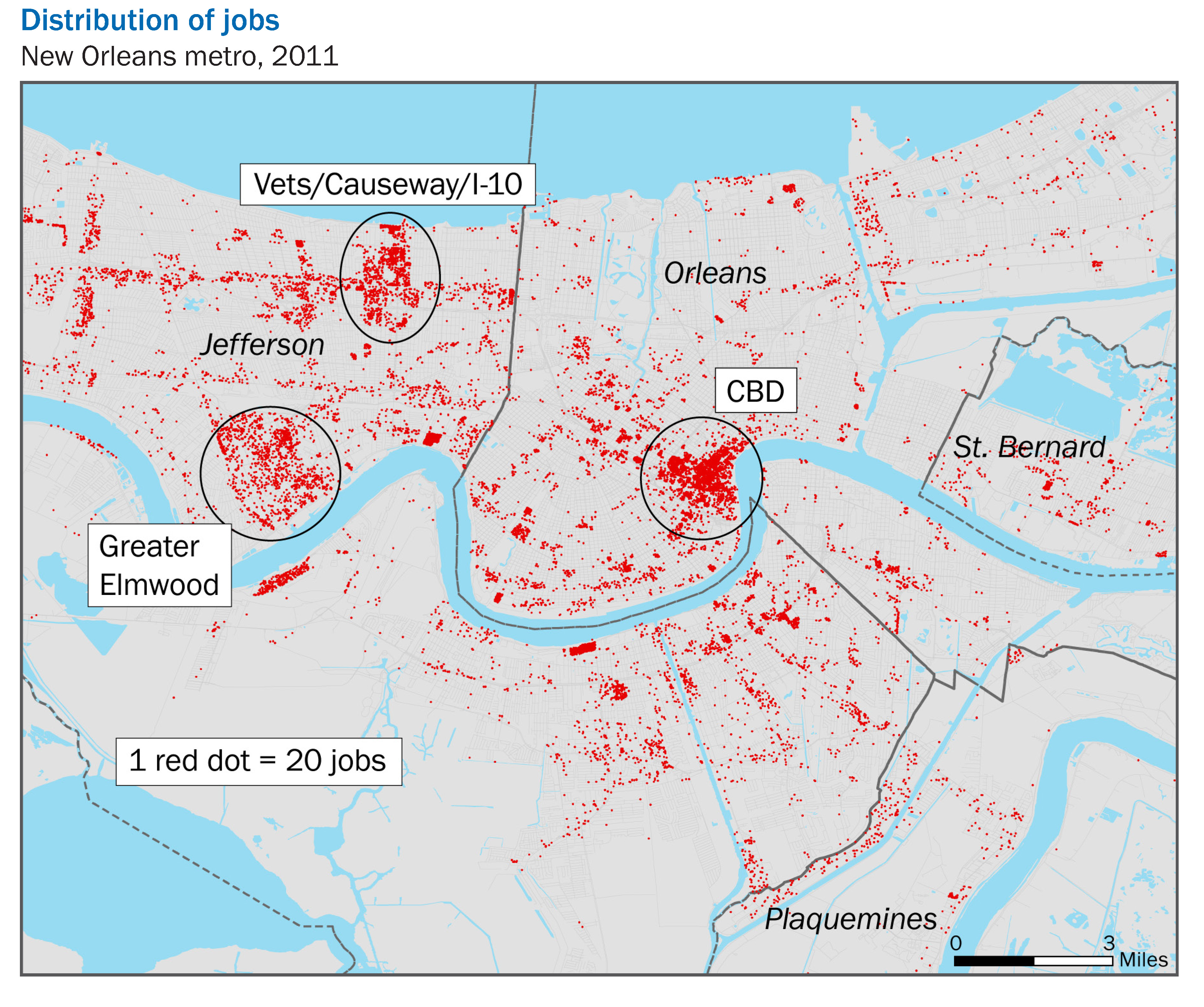

job distribution

Most of the jobs in Orleans and Jefferson Parish fall into three areas: Downtown, Elmwood Shopping Center and Lakeside Shopping Center. Notice the blank area in New Orleans East.

New Orleans Metro Jobs By Parish

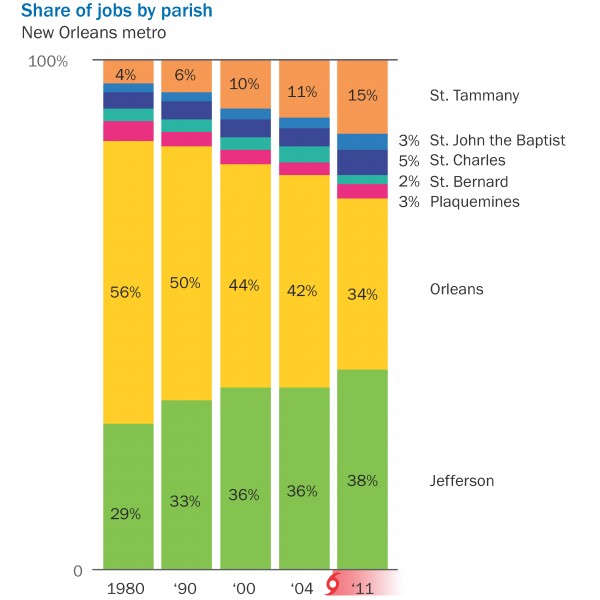

jobs by parish

Jobs have been leaving Orleans Parish since 1980. Neither Dutch, Sidney, Marc, C. Ray or Mitch could make any difference. The jobs went to Jefferson Parish and St. Tammany. Looking at the rate of change, Orleans Parish lost 39% of its market share, Jefferson Parish gained 31% of the market share, and St. Tammany gained 275% market share. Job growth is a strategic driver because it leads to housing booms, new demand for office space, new warehouses to store the goods that industry produces and new retailers to sell to the new consumers.

Productivity

productivity

Gross metro product (GMP) measures the average value of goods & services produced by each job in the region. Since 1980, productivity in the New Orleans metro area rose 24%, but the US productivity during the same time period rose 57%. More recently though, the data show a change in trend: since the 2008 recession, productivity has increased far more than the national average.

New Business Start-Ups

New businesses fled the New Orleans metropolitan area for the decade prior to Hurricane Katrina, but then things changed: existing residents decided after Katrina to start their own businesses and the influx of new residents to the area to help rebuild it led lots to stay and open their own business. The percent of new businesses due to Katrina more than doubled, which far exceeded the national trend.

Sources: Bureau of Labor, The Data Center, GNO Inc, LED

Louisiana Commercial Realty announced today they were hired to market the 69,000 square foot tract of land at 5550 Crowder Boulevard for GTE Financial. Robert Hand, president of Louisiana Commercial Realty said, " This tract of land is a great opportunity to bring retail businesses to an underserved market. Our research shows within a 5 minute drive time there is a population of 24,000 with an average household income of $48,000, and there is a real need for businesses to come into the area and provides goods and services to these residents. There are three main businesses that are needed: Motor Vehicle, General Merchandise and Restaurants. Our research shows these businesses could have annual sales exceeding $20 million dollars."

site plan

The area is replete with new developments, including:

New Walgreens at Crowder & Lake Forest Boulevard.

New Dorsey Retail Center on Crowder with tenants Pizza Hut & Planet Fitness.

New 500,000 Wal-Mart on Bullard.

Methodist Hospital on Lake Forest & Read Road in operation.

New Dollar General on Crowder.

Hand says, "With a resurgence of new businesses flooding the area, the quality of life for residents goes up which encourages more residents to move into the area. The Crowder area has the most affordable housing for people looking to build their life. Luxurious homes near the country club are priced around $250,000 and two-bedroom apartments are priced around $850 per month. It's a great place to get started."

Within a 5 minute drive time, the population, according to the 2010 Census, was 20,733 and is forecasted to grow to 29,217 by 2019. This growth rate exceeds 3.5% annually, which is 4 times higher than the average US population growth rate.

Hand says more information is available on the available property at LoopNet.com.

If you want to see Louisiana grow, which jobs would you prefer to bring in: oil or tourism? One of these two top industries delivers twice as many jobs but has one-third of the wages. This article examines jobs and wages, defining what is called Export Jobs which in the long run determine our economic future.

Mardi Gras is a perfect example of the strength of our economy to attract people who spend money on hotel rooms, taxis, car rentals, dining out, the latest fashions, site seeing, voodoo dolls and a host of other unique experiences found only in our nearly 300 year old city. But there is a bigger picture; it's called export jobs. These are the jobs that serve customers outside the region, as opposed to jobs that serve local customers. The reason we define export jobs is because if you have none, your economy is confined to growth of the region. Without export jobs, you can grow no more than the average, which today is around 2 to 3% annually. With export jobs, you have specialized industries that attract jobs from other regions that are void of those industries, resulting in faster than average growth.

Half As Much At Three Times The Price

In the 10 parish region surrounding New Orleans, the highest export job industry is the 40,000 job tourism industry with an average wage of $32,162 annually. Second on the export job list is the oil & gas industry which is less than half the number of jobs at around 18,000 but with average wages of $109,362. Multiplying the number of jobs by the average wages results in an economic wage total of $1.2 billion for tourism and $1.9 billion for Oil & Gas, a 58% difference. The problem is that of all the export industries since 1980, only four (motion picture, higher education, insurance agencies, and legal services) have increased job growth and the other seven are in a state of decline or stagnation. Oil & gas jobs have been leaving the region since the 1980's, and the same for the shipping industry. Katrina killed our shipbuilding industry but boosted construction and engineering.

10 Parish Region Export Industries Since 1980

Increasing Jobs:

Motion Picture

Insurance Agencies

Higher Education

Legal Services

Decreasing Jobs:

Heavy Construction & Engineering

Tourism

Oil & Gas

Shipping

Ship Building

Food Manufacturing

Export Industries In 10 Parish Region

Future Growth Depends On 50 Percent of Jobs

There are 195,507 jobs in the top 10 export industries, compared to 392,736 jobs in other industries, so our future growth depends on 50% of the jobs. The average annual wage of export jobs is $64,540, compared to $42,360 for local jobs. While the future growth may be in the motion picture, higher education, insurance and legal industries, the number of jobs produced still don't surpass ship building. But that is a snapshot of how the economy looks today, and our economy is always evolving and adapting to trends.

Conclusion

One look at the chart above and you can easily determine the downward trends today but also forecast where the job trends might be ten years from now, and it doesn't look good. Looking forward, thank goodness the Louisiana legislature a decade ago passed the Louisiana Motion Picture Act that made the movie industry think of us and thank you to Tulane for spitting out so many lawyers. We will save for later the research on why the insurance industry is growing; but at least we have four great export industries driving growth of the Louisiana economy. If you want to help Louisiana grow, preserve our oil industry and keep churning out petroleum engineering graduates, but also court our motion picture, higher education, insurance and legal industries that could determine our future growth.

Sources: Department of Labor, GNO Inc., The Data Center

Snowden was right. Big data is collecting information on you, but you will be astounded at how the latest technology can help commercial real estate buyers and sellers, landlords and tenants, to not only select the perfect location for their business but reduce advertising expenses and drive sales.

For example, if your business is selling toothbrushes, we can now tell how much people spend monthly on toothbrushes and toothpaste within a 1, 3 and 5 minute drive time from any location in any town, and compare that to the average across the United States.

The old school strategies include traffic counts and demographics, income and age; the new school strategy is Tapestry Lifestyle Behavior Analysis which drills down into how you think, what your beliefs are, and how you live your life.

Click on the link to the podcast that will explain.

Even though Louisiana has a diverse culture and varying economic drivers among its major cities, the range of prices of office space will surprise you. For the most part, office lease prices vary by roughly 20%, from a low of $15.03 in Lake Charles to a high of $19.19 in Harahan, with Shreveport/Bossier city being an outlier around $12.32. Sale prices range from $95.44 to $132.24, a 30% variation.

Office Lease Rate By City In Louisiana

office lease rates by city

Average Office Sale Prices By City In Louisiana

chart office sale prices by city

Does Population Affect Commercial Office Real Estate Price?

Loyola University's Institute of Politics believes Louisiana is divided into three main cultures:

Southern-New Orleans and Cajun country with French influence and driven by tourism and oil.

Middle-Alexandria and the agricultural economy.

Northern-Shreveport/Bossier City to Monroe with industrial and entertainment, so it is often considered an outlier.

The different cultures and population don't have an affect on average lease rates or sale prices, as shown in the table below, because each city has its own supply and demand factors which influence the market price.

Table of Average Lease and Sale Prices With City Population

table lease and sale rates

What surprises most people is the average time that it takes to fill empty office space. The fastest average time period is still 10 months, and the time it takes for leasing or selling office property ranges from 330 days in New Orleans to 752 days in Shreveport.

Table of Market Size For Lease and Sale By City With Days On The Market

table sf and dom

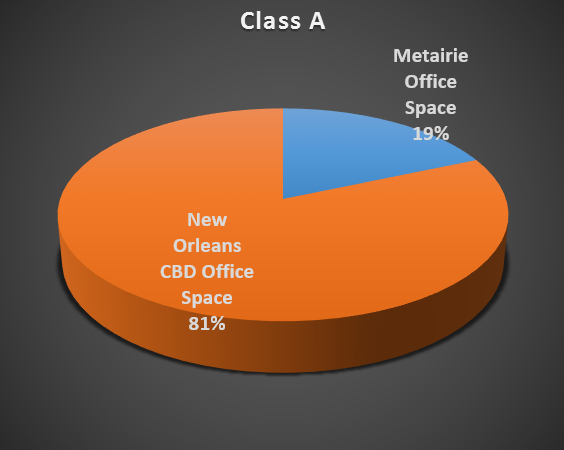

Pie Chart-Size Of The Office Market In Louisiana

chart pie office market for lease

Trends In Office Lease and Sale Prices

The best way to determine where prices are heading in the office market is to chart prices in the past. Below are prices for office space, for lease and for sale, by major city.

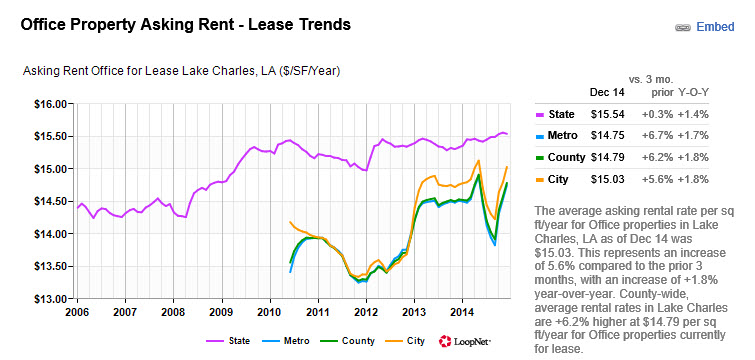

Lake Charles

The yellow line below shows the Lake Charles average office lease price is at its highest level in 4 years, which at $15.03 is up 5.6% over the last 3 months.

chart office lease lake charles

Kenner

The yellow line below shows the Kenner average office space for lease is up 15.8% year over year at $15.82.

chart office kenner

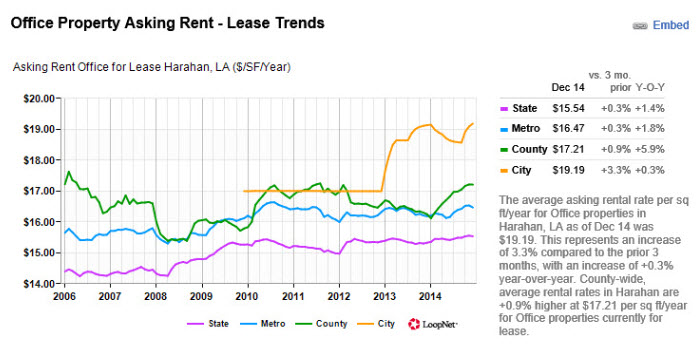

Harahan

The yellow line below shows the Harahan (zip 70123) average office lease price is at its highest level in 4 years, which at $19.19 is up only 0.3% year over year.

chart office Harahan

Covington

The yellow line below shows the Covington average office sale price is at a steady price of $132.24 and lease prices while fluctuating the last seven years without really going anywhere, average $18.20, down 4.3% year over year.

chart office Covington

Baton Rouge

The blue line below shows the Baton Rouge average office sale price is at its lowest level in 7 years, which at $97.44 is down 4.5% year over year. The average lease rate at $15.61 is below its $17 peak 4 years ago.

chart office baton rouge

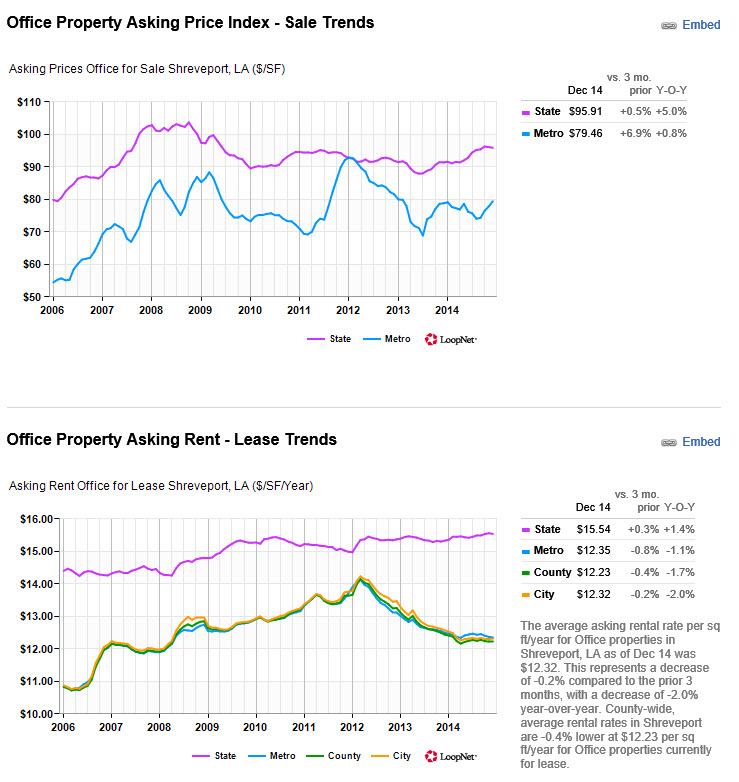

Shreveport

The blue line below shows the Shreveport average office sale price at $79.46 and the yellow line in the lease chart is $12.32, down 2% year over year.

chart office Shreveport

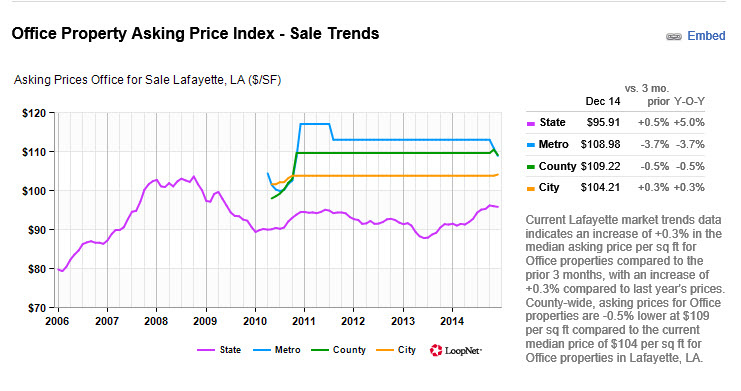

Lafayette

The yellow line below shows the Lafayette average office sale price is steady at $104.21. Average lease rates are not available.

office lafayette

Metairie

Metairie is a small market so for sale price data we use the Metairie/New Orleans Metropolitan average, shown by the blue line below at $113.73, up 8.6% year over year, and the yellow line in the lease chart is $17.48, down from the 2006 peak of $18, but up 4.5% year over year.

chart office Metairie

New Orleans

The yellow line below shows the New Orleans average office sale price at $109.02, up 3.4% year over year, and the yellow line in the lease chart is $16.31, down 0.3% year over year.

chart office new orleans

Summary

Prices vary by city and are based on supply and demand factors unique to economic drivers in the area. Pricing office space is not like pricing stocks and bonds, where there are many buyers and sellers who openly state their bid (buy) price and ask (sell) price, with transactions occurring in the middle when buyers and sellers agree. The best way to determine price levels is examine each property that is available within the same market in the same city, and adjust for differences and quality of the space.

Sources: LACDB, LoopNet, Census 2010, Loyola University

For help determining commercial real estate market prices, see our other articles at www.louisianacommercialrealty.com/blog or contact Robert Hand at 504-289-8172.

Are you a thorough reader? The 1st person to find the spelling, grammar or math error in this article wins $10. Email your error to roberthand@cox.net. Winner is announced in the next article.

jethro bodine ciphering

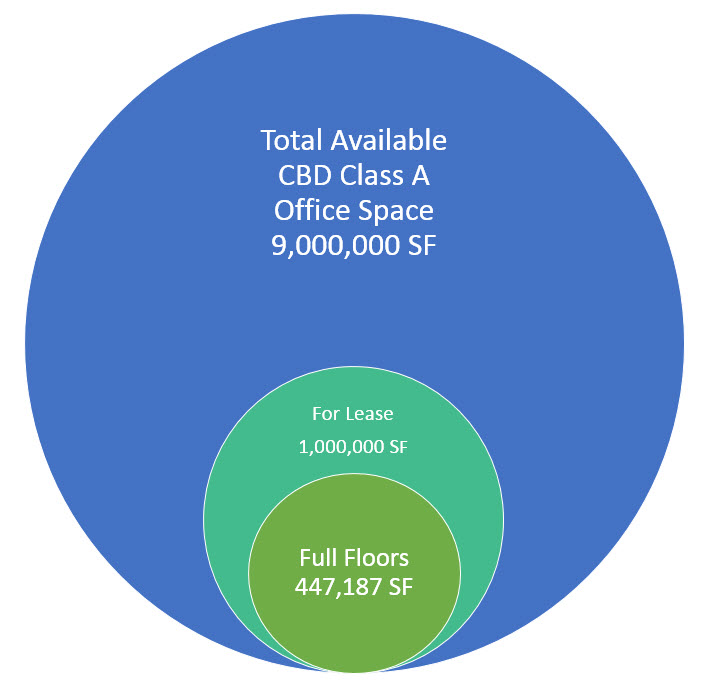

Whenever Beverly Hillbillies star Jethro Bodine needed to do math, he would commence to ciphering by the cement pond, proving that math can be simple if you have enough fingers and toes. Commercial real estate is sometimes that way but sometimes not. Fortunately, when we need to do some math to answer the simple question, "What is the average price of a full floor of Class A Office space in New Orleans?", the data is easily available and the work has already been done. There is just one catch: you can't get the answer the way you were taught.

Weighting The Average Is Not That Heavy

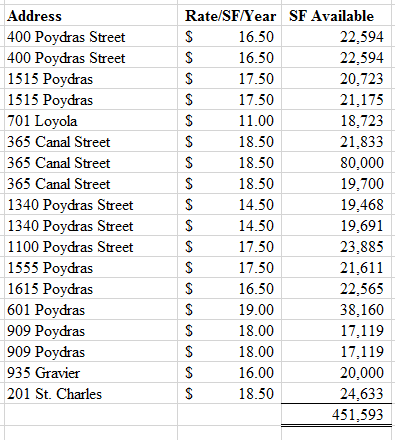

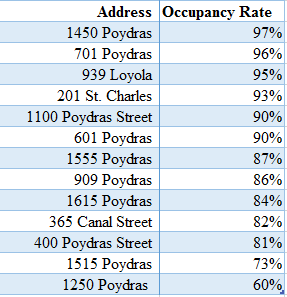

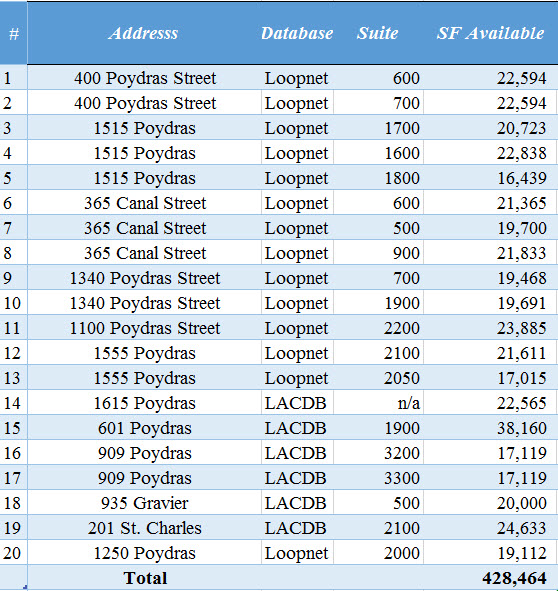

There are 14 Class A office buildings in New Orleans CBD, with a total square footage of approximately 9 million square feet, with one million square feet of that currently for lease, and 428,464 square feet of that comprised of full floor space.

TABLE ONE: New Orleans Class A Full Floor Space

list full floor space

Prices range from $15 per square foot for sublease space to $19 per square foot, and each space varies in how it passes along the cost of taxes, insurance and common area maintenance.

TABLE TWO: List Rates of Class A Office Space

prices full floor Class A

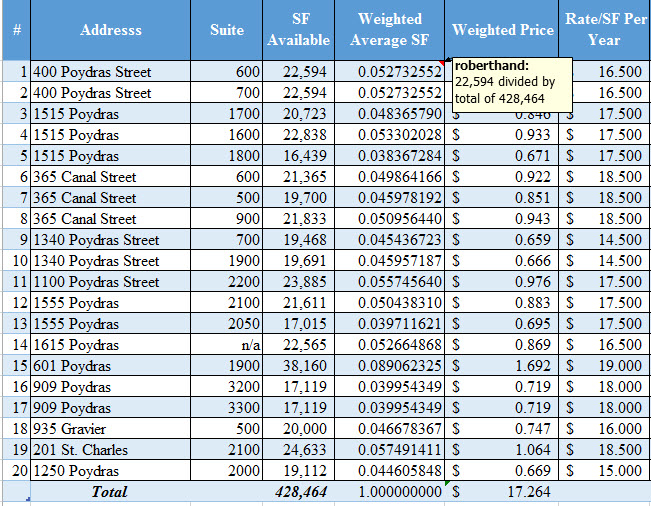

What is the average price? The simple way to determine the average price is to add up all the prices in the table above and divide by 20 ( the number of spaces), but that would not be the most reliable method because it assigns an equal weighting to each of the 20 spaces, as if they all had the same influence on the total square footage of 428,464. The best method for getting the average price is to take into account how much square footage each space has relative to the total. This way the number 15 space at 601 Poydras, which is the largest at 38,160 square feet, has a bigger impact on the final number than does the smallest space, number 5 at 1515 Poydras with only 16,439 square feet.

There Are Only Two Intermediate Steps For The Weighted Average Number

Step 1 is to determine the percent each space is relative to the total. Take the square foot available and divide by the total (in space #1, 22,594 divided by 428,464). Space #1 amounts to about 5.27 percent of the total space. Fill down and you can see that space #15 amounts to 8.9 percent of the total space and, therefore, its price has more weight on the total market than does any other space. Note the total of the weighted square feet equals 1.

TABLE THREE: Weighted Square Feet

weighted price process

Step 2 multiplies the weighted square footage by the listed rate to determine the weighted price for that space. The value for each space is how much that space contributes to the average price, taking into account the amount of square feet contributed to the total square feet. The total of all 20 spaces is $17.264, which is the most reliable answer to "What Is The Average Price?".

TABLE FOUR: Weighted Price

weighted price times SF

Summary

The weighted average method utilized here can provide more reliable results for any sum of data. It works best when there is a large variation in the variables, such as square footage and price. The big surprise is that list prices of Class A office space in the New Orleans CBD are fairly close together, and further adjustments could be made for the variance in terms. While other amenities can affect price and are the judgment of the tenant or landlord, using the weighted average price in negotiations can be a good place to start.

For more information on office space, click on these articles:

The following buildings are deemed Class A but had no full floor space:

1450 Poydras Street

701 Poydras Street

650 Poydras Street

639 Loyola Avenue

Excluded in this analysis but included in previous totals is 701 Loyola, which has a full floor 18,723 square feet in suite 501, but the building is no longer deemed Class A office space.

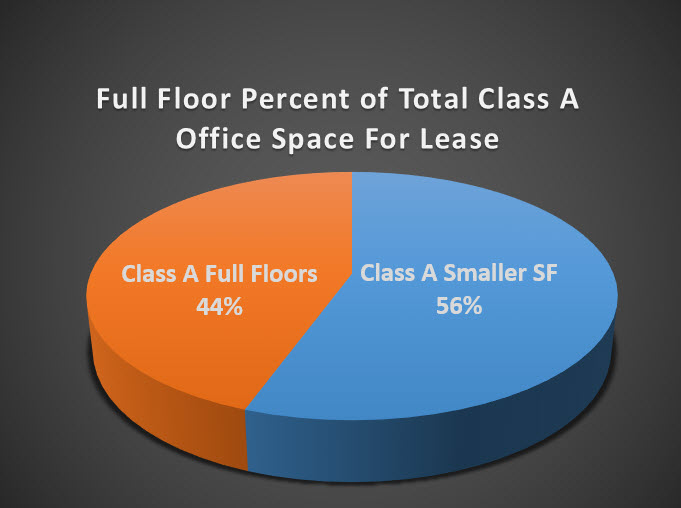

The Class A office market in New Orleans is 90% leased but the 10% that is vacant is almost half comprised of full floors, and full floors take an eternity to lease since they are configured for a single tenant. Full floors range from 18,000 square feet to 24,000 square feet which can accommodate 50 to 75 employees depending on the configuration.

pie chart full floor

Private Offices Are History

Gone are the days of 10' x 10' private offices, which accommodate the fewest employees per full floor. The modern office configuration has plenty of open desk areas that facilitate collaboration and teamwork, and can accommodate the highest number of employees. Full floor space can be difficult to lease to multiple tenants due to the layout of restrooms, hallways, and conference rooms; therefore, the most likely tenant is a large company with at least 50 employees moving into the downtown area. Even with the 35% payroll rebate as an incentive to media and software companies moving into the city, no full floor space has been leased in the past 6 months and the amount of full floor space has increased 19,000 square feet.

Of the one million square feet of Class A office space for lease in New Orleans, full floor space comprises 447,187 square feet.

chart full floor

Full Floor Space Is A Different Market

The result is that vacancy rates will stay higher for those buildings with empty full floors compared to other Class A office buildings, and lease rates will include a larger amount of free rent and buildout allowance. Once the market reaches equilibrium; however, the buildings that can offer the last Class A full floor space will have the highest pricing power and can command a higher than market rent. The tradeoff is that the present value of the higher rent several years down the road may be less than a lower rent price today.

For more information on the Office Market, see our publications:

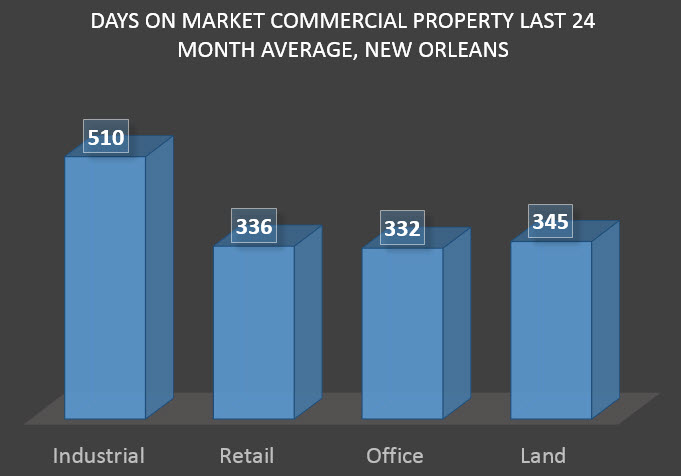

The biggest surprise to most sellers of commercial property is that the average time to find a buyer is well over one year. For example, in New Orleans, the average industrial property for sale or lease in the last 24 months has been on the market 510 days. And still counting.

Industrial Properties In New Orleans-Days On Market & Lease Rates

chart industrial days on market

The industrial sector has the longest waiting period. There are 81 industrial properties for sale or lease totaling 1.4 million square feet, with 632,000 square feet for lease and 770,000 square feet for sale. Of the properties on the market today, the average lease rate is $5 PSF and the average sale price is $40 PSF.

It's All Relative

Contrast this with the residential market where in uptown New Orleans the average time it took to find a buyer was 46 days. But that doesn't tell the whole story. Of the 503 residential properties so far in 2014 that sold, 27% sold within 5 days and 5% sold within one day. So the benchmarks we might have for residential property do not apply to commercial property.

503 sold residential days on market

503 sold residential days on market

Time It Takes To Sell Commercial Property Differs By Type

Each type of commercial property has its own supply and demand curve, with the economics of retail and office property making those sectors in higher demand than industrial property; therefore, the days on the market are less but still average almost one year.

There are 381 office properties for sale and for lease totaling 2.7 million square feet with 2 million square feet for lease and 700,000 square feet for sale. Lease prices average $15.60 PSF and sale prices average $64 PSF. The average office property has been on the market for 332 days.

There are 179 retail properties for sale and for lease totaling 915,000 square feet with 600,000 square feet for lease and 300,000 square feet for sale. Retail prices average $14 PSF and sale prices average $118 PSF. The average retail property has been on the market for 336 days.

There are 102 land sites for sale and for lease totaling 119 million square feet with 1 million square feet for lease and 118 million square feet for sale. Lease prices average $1.40 PSF and sale prices average $2 PSF. The average land site has been on the market for 345 days.

days on market commercial sectors

Three Things To Do Today To Sell Or Lease Your Commercial Property

Commercial real estate can provide excellent returns to investors, especially since 30 year US Treasuries only return 4% today. But there is a trade-off, which is liquidity. Given that it takes a long time to sell or lease commercial property, have a plan and a marketing strategy to shorten the time period. Ideas that work include:

Compiling a Marketing Presentation that includes information to create demand for your property, such as zoning and permitted uses.

Getting your property to come up on the first page in a Google search.

Promoting your property locally and also nationally to a target market that is most likely to buy or lease your property.

There are 13,439 active Louisiana real estate agents, but the city with the most and the company with the most will surprise you. The location of real estate agents does not match up identically with the location of the home buying public. For example, New Orleans has the most licensed agents but does not have the highest population count unless you add in Metairie. Shreveport is the 3rd largest agent count in the state but only has the 5th highest population.

Agents and Population Percentages Are One Surprise

The table below ranks the top 15 areas, comparing the number of agents with the population.

Table of Agents and Population

Agent Ranking

Population Ranking

1

New Orleans

BATON ROUGE

2

Baton Rouge

NEW ORLEANS

3

Shreveport

METAIRIE

4

Metairie

LAFAYETTE

5

Lafayette

SHREVEPORT

6