Valuing commercial property can be a real mystery sometimes because comparable sales are often scarce. This article discusses the 5 things you need to know when working in, buying, selling or leasing commercial property.

Know what to look for in buying, selling or leasing, offices, shopping centers, apartments, hotels and warehouses.

How to use technology, including demographics and zoning, to make better decisions.

How to understand and command the nuances of contracts.

How to utilize basic financial analysis tools for realistic valuations.

How to negotiate with attorneys and agents.

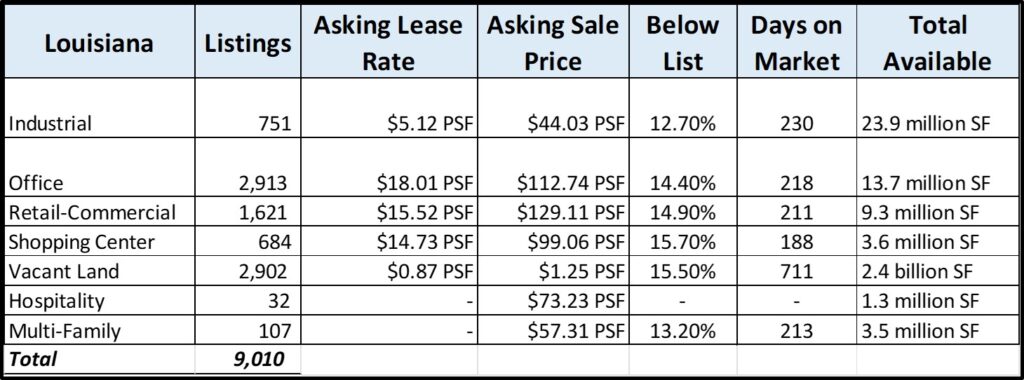

Here Are The Major Sectors of Commercial Property

Office

Industrial

Retail

Shopping Centers

Hospitality

Multifamily

Understanding The Lease Contract

What is CAM? Stands for common area maintenance and is all the operating expenses of the property, including property taxes, insurance, landscaping, water and electricity costs. These costs can be passed along to the tenant or included in the rent price. If they are passed along, the landlord estimates the CAM expenses at the first of the year and charges 1/12 of the yearly cost monthly to the tenant. At the end of the year, if expenses are different from the estimate, the landlord bills the tenant a lump sum reconciliation.

What are rentable and usable square feet? Usable square footage is the actual size of the space a tenant would use, not lease; however, there are other spaces that the tenant uses, such as the hallways and lobby and restrooms. Adding up all the space in the building less the vertical penetrations such as elevators and stairs equals the rentable square footage. This is divided by the total usable square footage which is called the core factor. The usable square footage of an individual tenant space times the core factor is called the rentable square footage. The result is that the tenant pays the cleaning, air conditioning and heat for the hallways and lobby and other common area in the building.

What are gross and net leases? A gross lease is when all the operating expenses are included in the price of the lease. The tenant gets one price per square foot and never has to pay more, unless the lease spells it out. A net lease is a base rent per square foot plus the operating expenses, including everything else. Sometimes in a net lease, the property tax roll is in the tenant's name because the tenant is responsible for property taxes, even if they increase dramatically. Landlords love net leases.

Types of Office Space

The bible of real estate is declared by the Building Owners and Managers Association, or BOMA, and here is how they classify the 3 types of office buildings:

Class A Most prestigious buildings with rents above average for the area. Buildings have high quality standard finishes, state of the art systems and an impressive market presence.

Class B Buildings with rents in the average range for the area. Building finishes are fair to good for the area and systems are adequate, but the building does not compete with Class A at the same price.

Class C Buildings for tenants only wanting functional space at rents below the average for the area.

Class A office buildings tend to have on site parking which is usually covered and have the highest rents. These buildings are the most luxurious and always well kept. Not a drop of trash anywhere. They usually have a cleaning crew operating continuously and a concierge or security guard at a desk in the lobby.

Class B space is nice but not the best. It is priced usually $2-$3/SF less than Class A and not as luxurious but just average in upkeep.

Class C is adequate and usually $5-$6/SF less in price. These are the older building without parking and not well maintained.

Industrial

Industrial space can be anything from breweries to warehouses and 5,000 square feet to millions. Industrial property tenants and owners are interested mostly in:

3 phase electrical-this allows heavy machinery to operate and 99% of all warehouses would already have 3 phase electrical.

High floor density-since warehouses are used to store inventory close to where it is being used, pallets of materials are stacked high, creating a high load on the floor. Over time, the floor would crack, so knowing the floor strength would allow a tenant to not damage the floor. The strength is determined when the floor is poured, so if you are in 300 year old New Orleans, you will need to get PSI Company to drill small holes in the concrete and test for the strength.

Loading docks-could be drive up ramps for a florist's van or dock high loading docks that an 18-wheeler can back into so a forklift can unload the pallets.

Laydown yard-every warehouse or industrial property needs a fenced in side yard to store lumber or steel or long pipes that do not need to take up space under the roof.

Eave height- since the warehouse is used for storage, the height of pallet stacking is limited by the height of the eave which is how high the roof is at the wall. The center height is simply how high the roof is in the middle, which is highest in a pitched roof. Measurements are taken from the bottom of the metal support rafters.

Apartments/Multifamily

Low Income Tax Credits

Almost all multifamily/apartments are financed with help from the government. The most common assistance is Low Income Tax Credits from the Department of Housing & Urban Development, or Community Block Grants or New Market Tax Credits. Every year HUD issues $13 billion in tax credits to the states, which then takes applications from developers. Once the state awards the credits to developers, they can be sold to investors, usually at 90 cents on the dollar.

The investor then applies the full $1 worth against his state income tax obligation and the developer uses the cash payment from the developer as equity for a loan from a bank who acts as the middleman. The developer only has to agree that 40% of the apartment units are rented to tenants with incomes no more than 60% of the area's median income. Minimum wage income for 2 is $30,000 annually so the benchmark would be $24,000 income. All tenants would have jobs and be law abiding citizens, as dictated by the apartment's property manager.

Retailers

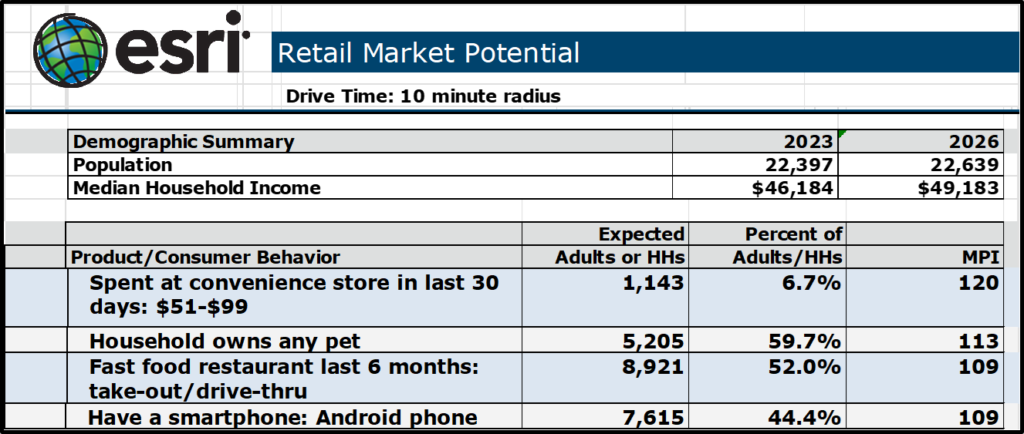

Retailers always want to be in an area where there are enough shoppers to make their store feasible. The standard in demographic research is the population count and household income, but the latest technology drills down into how that income is spent.

Data from ESRI shows that within a 10 minute drive time that 5,205 households own a pet which is 59.7% of households and 13% more than the average household in the United States. The retailer now knows that Petco would be a successful tenant.

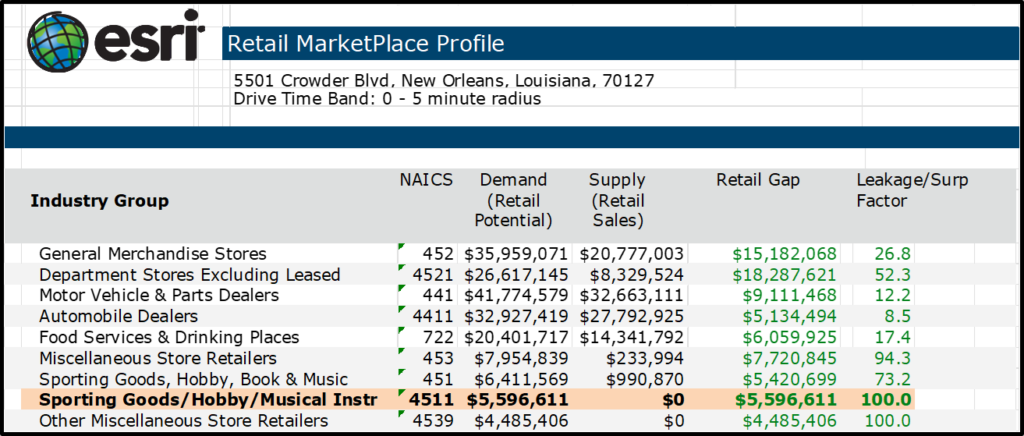

Retailers-Consumer Spending Patterns

Drilling down further into consumer spending, the data show that $5,596,611 is spent on sporting goods within a 5 minute drive time, but no existing retailer sells sporting goods. This is vital information for the retailer tenant and also the landlord, because now both parties know that type of business will be successful and how much they can expect in sales.

Consumer Price Index Adjustments

The most important language in a lease contract is the clause on increasing the rent amount to keep pace with inflation. This language must be very specific but also clear. Most language states the rent is tied to the consumer price index, but there are actually 4 consumer price indices. Here is how your lease should state the inflation adjustment:

“The rental under this lease shall be four ($4.00) dollars per square foot for the first twelve (12) months, with annual adjustments tied to the Consumer Price Index (published by the Bureau of Labor Statistics, All Urban Consumers, Current Series, Index) for the previous calendar year period.”

Notice that language tells exactly what index is used, where to find it and how to apply it.

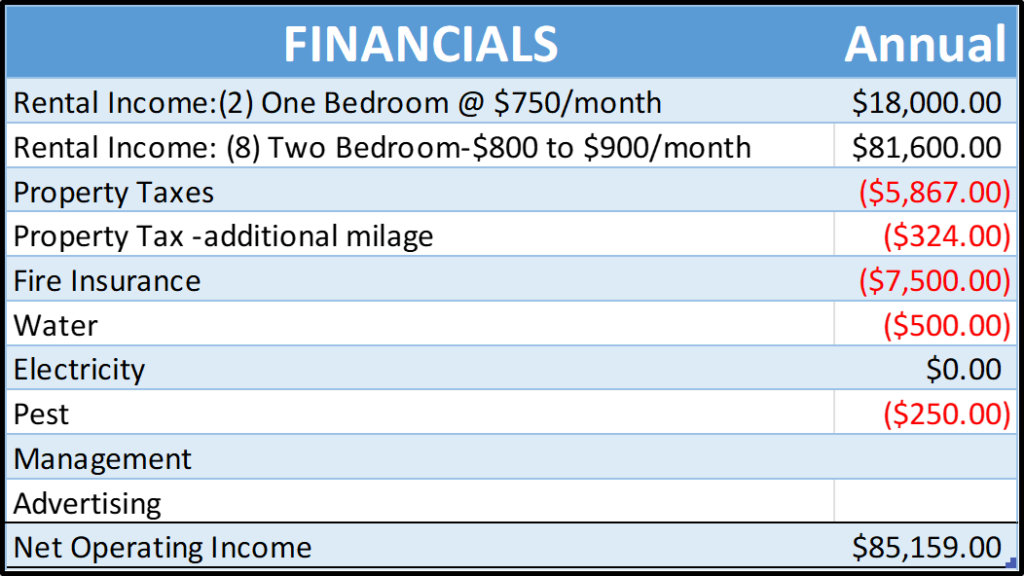

How To Value Commercial Property

The value of commercial property is based on the net operating income, which is the actual, not forecasted, rent income minus expenses (but not depreciation or interest). In the table above for a 10 unit apartment building, the rent income is $96,600 annually and the net operating income is $85,159.

The value is calculated by dividing the net operating income by the capitalization rate, which we assume is 7%. The seller would then value the property at $1,216,557. But wait, there's more. Notice that the seller left off management and advertising expenses. The buyer will add this expense back in because he will not manage the property himself like the seller did, who did not charge for his time. Assuming advertising of $500 monthly and management of $500 monthly, plus repairs/maintenance of $1,000 monthly, the buyer net operating income is $61,159 annually, making the value $873,700. The final sale price on this property was $810,000.

Negotiation

Most buyers and sellers can only negotiate on 3 variables, which usually are: price, deposit amount and length of inspection period. Often there might be 10-15 issues, but both parties need to let some issues go. You want to let go of the items that are not that important and negotiate on the items that are deal-breakers.

Be an active listener. Think about what the other party is saying, then repeat it back to them: "If I hear you correctly, what you are saying is ...". There is always the reason stated but then there is the reason behind the reason. Find that out.